As global headlines grow heavier and market uncertainty spreads, investors find themselves caught between rising tensions in the Middle East and a cautious U.S. Federal Reserve preparing its next monetary step. This week, the markets have been moving to the rhythm of war speculation, volatile oil prices, and mixed economic signals, all while the Fed gears up for its latest policy decision.

A financial strategist from Tandexo closely examines these developments, breaking down where the pressure is coming from, what the signals mean, and how traders can make sense of the noise.

Energy Markets in the Crosshairs

Crude oil prices surged by 4% earlier this week, responding to fears of a broader war involving Iran, Israel, and potentially the United States. These fears intensified after America’s president urged civilians to leave Tehran and reportedly weighed joining Israel in targeting Iran’s underground nuclear sites, including Fordow.

Still, oil eased back slightly in Asian trading on Wednesday, with U.S. crude dipping below $75 per barrel. Even with spot prices up about 14% since last week, they remain 7% lower than a year ago and are still below January’s $80+ peak.

Much of the market’s current hesitance stems from the fact that while military action is escalating, crude supply hasn’t yet been seriously disrupted. Tanker traffic through the Strait of Hormuz, a route for nearly 20% of the world’s oil, has continued despite reports of GPS jamming and at least one tanker collision near Iran’s port of Bandar Abbas.

What the Fed Might Say (and Why It Matters)

As energy prices fluctuate, traders have shifted their gaze toward the U.S. central bank. The Federal Reserve’s policy meeting concludes Wednesday, just ahead of the Juneteenth market holiday.

No immediate rate change is expected, but the focus will be on the “dot plot”, which outlines where policymakers see interest rates heading. The previous forecast called for two cuts by year-end, but there’s now speculation that only one may remain.

Markets have priced in 45 basis points of easing by December, which reflects uncertainty around inflation, oil shocks, and slowing economic data.

Treasury markets responded accordingly:

- 10-year yields slipped, fueled by soft May data on retail sales, industrial production, and housing starts

- The Fed also announced a June 25 board meeting to review bank capital requirements, possibly allowing banks to hold more Treasuries by easing supplementary leverage ratios

This move, while technical, signals the Fed is trying to support both liquidity and stability in the financial system, even as it navigates complex macroeconomic challenges.

Global Stocks React in Different Directions

Global equity performance has diverged in response to geopolitical and economic triggers:

- Hong Kong equities underperformed, weighed down by local economic concerns

- European defense stocks rose, reflecting demand for military suppliers amid the conflict

- In Sweden, the central bank cut its key rate to 2.0% from 2.25%, weakening the Swedish krona, and signaled that more easing may come before year’s end

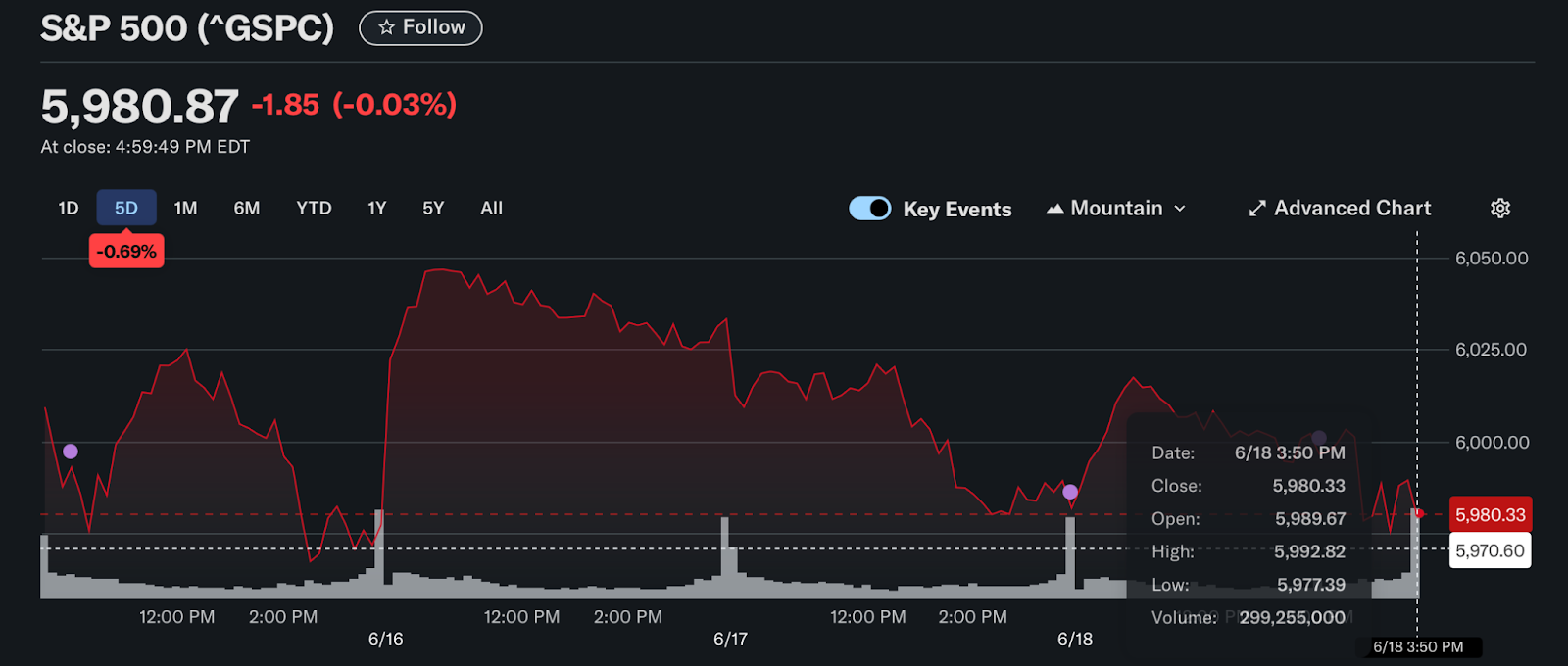

Meanwhile, U.S. futures opened higher on Wednesday, rebounding after the S&P 500 fell nearly 1% on Tuesday.

Currency and Crypto Check

The U.S. dollar continued to decline, even though the “short dollar” trade is getting crowded. Central banks, which have long been buyers of dollar-denominated assets, appear to be stepping back, signaling a potential shift in global portfolio strategies.

The Swiss franc also edged lower, ahead of an expected interest rate cut to 0% from the Swiss National Bank.

In crypto news, Bitcoin remained flat despite a major legislative milestone: The U.S. Senate passed a bill regulating stablecoins, establishing a clearer framework for dollar-pegged digital tokens. Some view this as a pivotal moment for crypto legitimacy, though markets were slow to react.

Energy Stocks and Freight Signals

Investors in energy equities have been repositioning as the outlook for oil remains unpredictable. Much like spot prices, freight rates from the Persian Gulf have jumped since the conflict escalated. But like oil, they still haven’t broken their yearly highs, suggesting that markets are cautious about overcommitting to any single outcome.

This cautious optimism extends to gold as well: While traditionally a haven, gold prices have not hit new records, and slipped on Wednesday.

What Traders Are Watching Next

Key data points and events coming up include:

- U.S. May housing starts

- Weekly unemployment claims

- April Treasury International Capital (TIC) data

- Federal Reserve’s rate decision and economic projections

- Statements from European Central Bank leaders

- Bank of Canada governor’s remarks

- Earnings from Progressive Insurance

In addition to rate commentary, the Fed Chair’s press conference will be watched for signals on how current conflicts, oil shocks, and tariffs are shaping future monetary policy.

Conclusion: Calm Before Another Storm?

With geopolitical pressures climbing and economic uncertainty thickening, markets find themselves in a fragile holding pattern. The oil market isn’t yet pricing in disaster, but it’s definitely nervous. Central banks, meanwhile, are moving cautiously, trying not to fan inflation while avoiding a growth slowdown.

A financial advisor from Tandexo underscores that these are the kinds of moments where signals matter more than sound. From the dot plot to diesel flows, from crypto frameworks to currency shifts, what happens next may depend less on new headlines and more on how traders interpret the broader narrative forming beneath them.