After months of relative calm, investors face a gauntlet of political deadlines and data releases that could jolt everything from Treasuries and the U.S. dollar to gold, corporate credit, and European bonds. From a looming U.S.–EU tariff decision to a contentious French budget vote, and another potential showdown in U.S.–China trade talks, risk premiums look thin compared with the hazards ahead.

Anna Tutova, chief market strategist at Maverix-Global, will unpack the hidden fault lines, outline where surprises may hit first, and explain which assets could swing most dramatically.

Tariff Tremors on July 9

Risk desks are laser-focused on next week’s U.S.–EU tariff deadline. Current pricing implies a mildly positive outcome, either a 10 % universal tariff or a last-minute postponement, similar to what occurred with Beijing earlier this year. Yet:

- Corporate-bond yields appear too low for that uncertainty, warns the global head of solutions strategy at a leading asset manager, who recently turned bearish on credit.

- An EU push for exemptions could still stall, raising fears of retaliatory taxes on key exports.

- Equities have already rebounded 24 % from their April lows, suggesting limited upside if the news is merely “not terrible.”

Should talks falter, expect credit spreads to blow wider and short-dated equity volatility to spike.

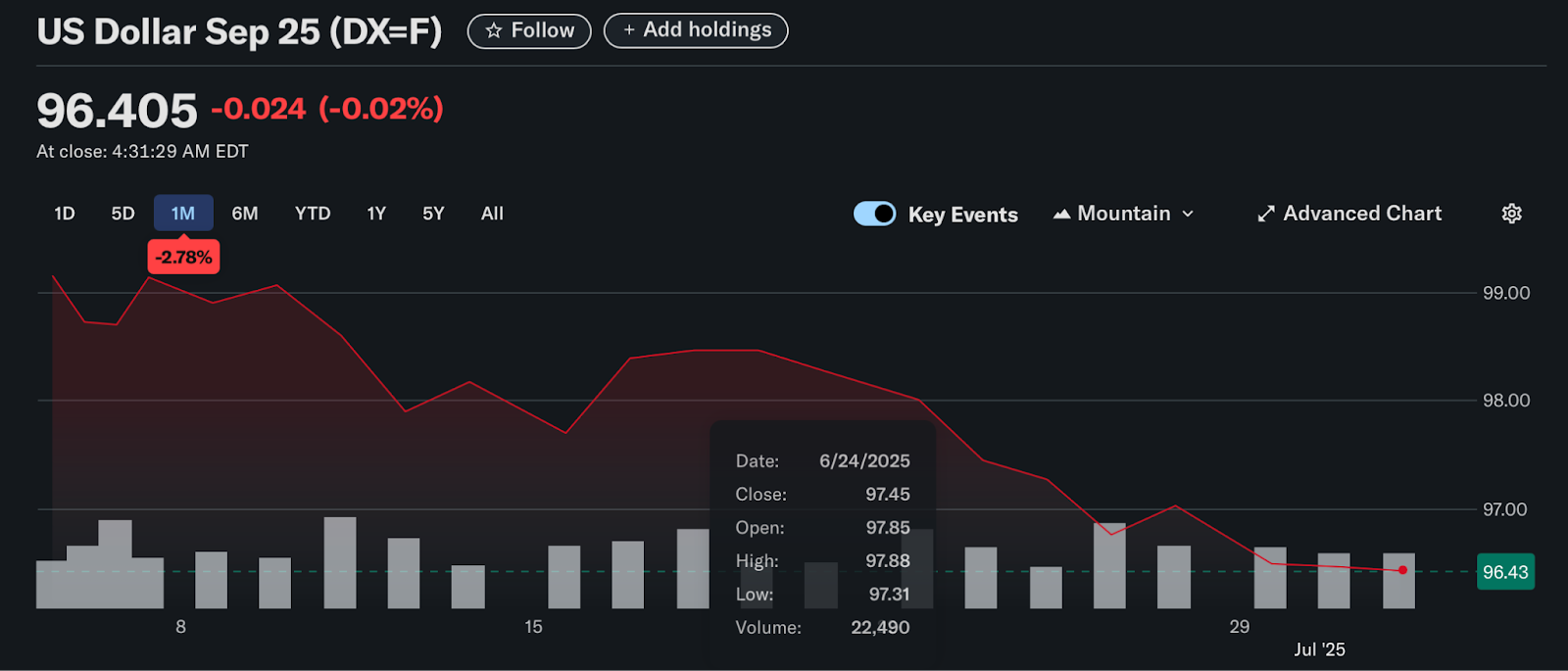

Safe-Haven Assets: Dollar, Treasuries, Gold

Any tariff shock will spill straight into currency and bond markets:

- The U.S. dollar is already down about 10 % versus major peers this year. A breakdown in negotiations could halt that slide; a deal could sink it further and fuel cross-currency volatility.

- Treasuries may suffer if global trade anxiety deepens, argues a fixed-income chief at a prominent U.K. fund house. Foreign central banks have accumulated U.S. debt partly because the greenback dominates global trade. If those flows wobble, yields could shoot higher.

- Gold is up more than 25 % year-to-date to roughly $3,344, serving as a hedge against recession and inflation. A surprisingly benign tariff outcome would likely trigger profit-taking by real-money accounts and hedge funds, warns the multi-asset head at a Swiss investment firm.

Data Jolts: July 4 Jobs Print and the August 1 Payrolls

While Thursday’s U.S. payroll snapshot draws immediate attention, several managers argue the August 1 jobs report, when trading volumes thin out, poses the bigger risk.

- The strategist at Russell Investments highlights that labor data have flown under the radar, even though softening numbers could spark fresh bets on rate cuts and yank the yen sharply higher against both the dollar and the euro.

- Options markets imply muted volatility in several major currency pairs, a complacency that could unwind fast if payrolls disappoint.

Europe’s Debt Stress Watch

Investors can’t ignore the continent either:

- The French prime minister faces a July 14 showdown to pass deficit-trimming measures. The extra yield, or spread, that France pays over Germany is about 70 basis points, which some managers say underprices the political risk.

- Germany’s upper house votes on a stimulus tax break package on July 11. Expectations of larger bond issuance have already nudged 10-year Bund yields up 25 basis points this year, to around 2.62 %.

- In the U.K., fresh welfare-policy reversals threaten the fiscal math, reviving concerns about gilt supply and pushing sterling-rate volatility higher.

RBC Wealth’s head of strategy says they are underweight French debt until the budget fog clears.

The August 12 U.S.–China Deadline

Just when investors catch their breath, an August 12 ultimatum for U.S.–China trade talks looms. A favorable outcome could rally risk assets late in the summer; a miss would reopen the tariff war playbook and intensify pressure on global manufacturing names that already face margin squeeze.

Positioning Playbook

| Asset | Base-Case View | Surprise Upside | Shock Risk |

| U.S. Dollar | Drifts lower on mild tariff deal | Safe-haven bid if talks collapse | Deep slide if global growth perks up |

| Treasuries | Range-bound | Rally on weak jobs data | Sharp selloff on reflation narrative |

| Gold | Edges lower on profit-taking | Breaks new highs on policy panic | – |

| Credit Spreads | Hold tight | Narrow further on clear deals | Widen sharply if tariffs escalate |

| French OATs | Stable if the budget passes | Spread tightens vs. Bunds | Blowout if the vote fails |

Tactical Ideas from the Pros

- Curve Steepeners in Treasuries: Bet that long yields climb faster if safe-haven flows reverse.

- Long Yen Volatility: Cheap insurance against U.S. data miss triggering rate-cut speculation.

- Underweight French Bonds: Reduce exposure until July 14 budget clarity.

- Fade Gold Rallies Above $3,400: Lock profits if tariff headlines turn benign, then reload on dips.

- Credit Hedges: Use CDS indexes to offset tight cash-bond spreads ahead of tariff and payroll risk.

Conclusion

The next five weeks pack a rare density of binary events, each capable of jolting currencies, rates, and commodities. Tariff showdowns, pivotal job numbers, and Europe’s fiscal battles all converge against a backdrop of historically low volatility pricing.

Whether markets re-price risk modestly or lurch violently will depend on an unpredictable mix of policy decisions and data surprises. As Anna Tutova of Maverix-Global emphasizes, investors who underestimate this cocktail of catalysts may find their portfolios shaken rather than stirred when summer’s calm abruptly breaks.