Introduction

In a market filled with uncertainty, investors often overlook opportunities in sectors weighed down by volatility or recent setbacks. Mid-cap biotech firms, in particular, may look risky at first glance, but for those willing to dig deeper, some names present a strong recovery case.

Today, we examine two companies, one leading the way in gene-editing therapies, the other shaking up obesity drug development, that could offer outsized gains. Jane Davis, an analyst at Maverix-Global, will explore why patience and perspective matter when evaluating these beaten-down prospects.

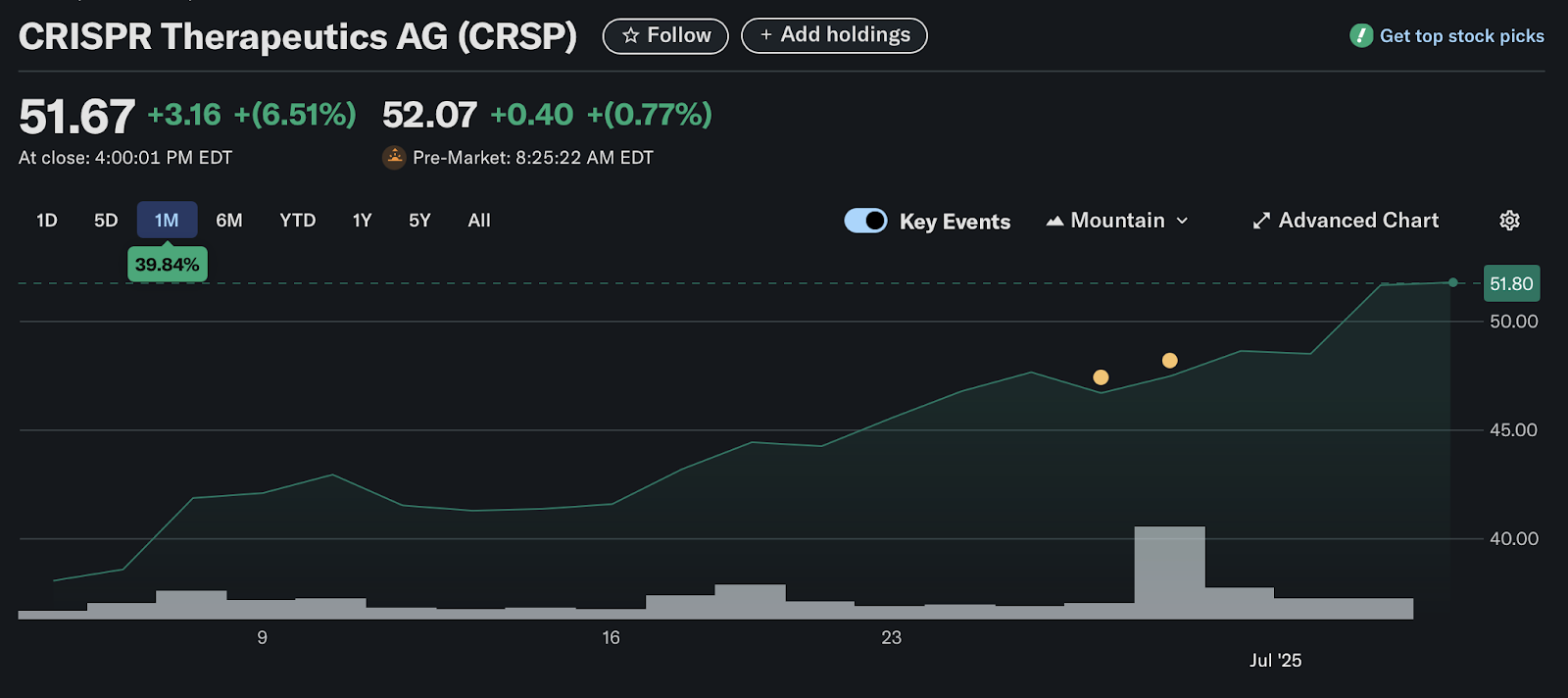

CRISPR Therapeutics: A Gene-Editing Pioneer Awaits Its Next Act

CRISPR Therapeutics made history by developing Casgevy, the first approved gene-editing medicine to leverage Nobel Prize-winning CRISPR technology. The company’s initial public offering (IPO) in 2016 sparked impressive gains, but the momentum faded after 2021 for several reasons:

- Clinical progress is often met by profit-taking among investors, making early milestones a double-edged sword.

- Casgevy remains complex to administer and, despite approval in late 2023, has not yet delivered a significant financial impact.

- CRISPR Therapeutics is still unprofitable, a major concern in today’s cautious investing climate.

Yet the future may not be as bleak as recent price action suggests. CRISPR Therapeutics is advancing new clinical trials for type 1 diabetes, hard-to-treat cancers, and other conditions, with potential data releases as soon as this year. These areas, if successful, could turn investor sentiment around rapidly.

Moreover, Casgevy’s commercial success is only beginning. The medicine, priced at $2.2 million per treatment course in the U.S., targets a population of roughly 60,000 patients across key markets. Profits are shared with a larger drugmaker partner, which has sped up regulatory approvals and expanded reach, especially in markets like the Middle East, where opportunities are substantial.

On the financial side, CRISPR Therapeutics boasts $1.86 billion in cash and equivalents, providing critical runway to fund its pipeline and weather uncertainty. The company’s innovation and potential for blockbuster revenues from Casgevy and beyond mean that patient investors could see the stock bounce back in a meaningful way.

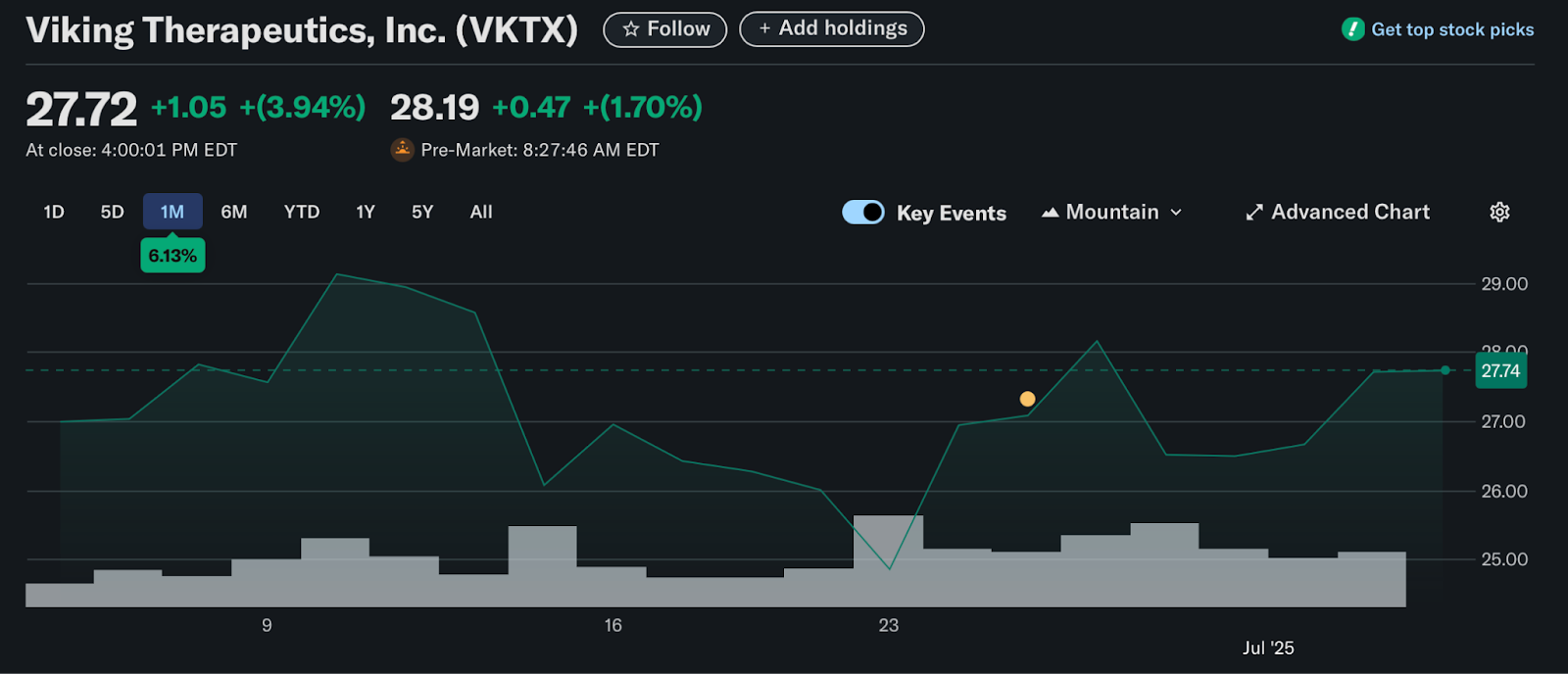

Viking Therapeutics: A New Challenger in the Obesity Drug Race

Viking Therapeutics wasn’t a household name until recently, when strong phase 2 results for VK2735, a weight management therapy, put it on the map. Although shares jumped initially, the momentum cooled, largely due to profit-taking rather than bad news.

The anti-obesity drug market is one of the fastest-growing areas in biotech. VK2735 has delivered mid-stage data that outperforms most peers, and Viking is now testing an oral version of the same molecule, potentially broadening patient access.

But Viking’s ambitions go further. Its VK2809 candidate is entering phase 3 for metabolic dysfunction-associated steatohepatitis (MASH), a serious liver disease, after promising mid-stage data.

Meanwhile, VK0214 is being trialed for X-linked adrenoleukodystrophy, a rare genetic nerve disorder. This candidate has even earned the FDA’s orphan drug designation, which provides incentives for drugs treating rare diseases.

With a current market capitalization of around $3 billion, Viking’s robust clinical pipeline is impressive. If the company navigates the regulatory process and demonstrates continued clinical success, especially with VK2735, the stock could see significant appreciation.

Of course, the risk profile is high: clinical setbacks or regulatory delays could pressure shares, especially with the heavy focus on VK2735. Still, for investors willing to accept some uncertainty, even a modest stake could pay off handsomely if the science holds up.

Key Data and Upside Factors

- CRISPR Therapeutics:

- $2.2 million per Casgevy treatment

- $1.86 billion in cash at Q1

- 60,000 eligible patients across target regions

- Viking Therapeutics:

- Phase 2 success in weight management therapy

- Advancing both injectable and oral formulations

- Orphan drug designation for a rare-disease drug

Investment Perspective: Risks and Opportunities

Both CRISPR Therapeutics and Viking Therapeutics illustrate why the biotech sector is both thrilling and nerve-wracking for investors:

- Potential rewards are substantial, especially when a new therapy addresses a large unmet need or a rare disease.

- The risks are real, particularly for companies that have not yet turned profitable or depend heavily on just one or two drugs in the pipeline.

It’s essential to balance optimism with caution. Cash reserves, partnership deals, regulatory tailwinds, and innovation pipelines should all be weighed before making a move.

Conclusion

Beaten-down biotechs aren’t always value traps. CRISPR Therapeutics and Viking Therapeutics each have catalysts ahead, innovative products in the pipeline, and access to large, unmet markets. For investors willing to navigate the volatility, the upside could be substantial if breakthroughs materialize.

As Jane Davis from Maverix-Global would point out, the true potential in biotech often comes to light when others have moved on, making now an interesting time to look again at these under-the-radar contenders.