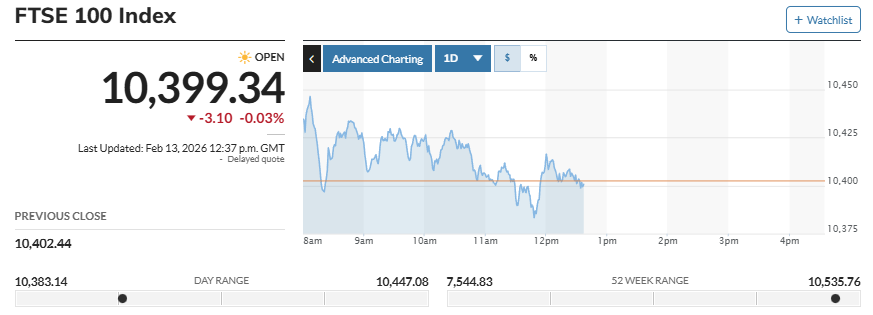

London equity markets traded with limited movement as investors evaluated shifting global sentiment tied to rapid developments in artificial intelligence technologies. Both major benchmarks, the FTSE 100 and the FTSE 250, slipped about 0.1%, reflecting cautious positioning rather than broad selling pressure. Despite the subdued session, the indexes remained on track for modest weekly gains, indicating underlying stability.

According to finance experts at Unirock Gestion, restrained index movement during periods of technological uncertainty often signals a recalibration phase rather than a directional trend. Investors frequently pause after major innovation cycles to reassess valuation models and sector exposure.

AI Developments Trigger Sector Volatility

Recent releases of advanced AI tools since late January have introduced intermittent volatility across global markets. Investors are attempting to determine how newer technologies may affect traditional industries, particularly sectors where automation could alter cost structures or competitive dynamics.

In the United Kingdom, the impact was most visible in technology firms, life insurers, and banking shares. Each of these sectors was on course for weekly declines exceeding 4%, suggesting that portfolio adjustments were underway as investors reassessed risk exposure.

However, technology shares staged a partial rebound during Friday trading. The sector rose roughly 3.8%, with information-services company RELX advancing about 5.4% and credit analytics firm Experian gaining approximately 4.3%. Such rebounds often occur when investors view earlier selloffs as excessive relative to fundamentals.

Defence Stocks Gain Momentum

While several sectors faced pressure, defence-related companies moved higher. The sector advanced roughly 2%, supported by expectations that increased multinational cooperation across Europe could lead to higher spending in the industry.

Sector rotations of this kind are common during uncertain market phases. Investors tend to shift capital toward industries perceived as more resilient or supported by long-term demand drivers. Defence companies are often viewed as structurally supported sectors because spending levels tend to remain stable across economic cycles.

Commodity Movements Weigh on Mining Shares

Mining companies were among the largest drags on the primary index. Major producers such as Rio Tinto and Antofagasta declined more than 2%, tracking weaker copper prices. Commodity-linked equities frequently move in tandem with underlying resource prices because their revenue streams depend directly on market valuations for raw materials.

Price declines in metals can therefore translate quickly into equity market adjustments, especially when investors anticipate softer demand conditions or shifting industrial activity. Mining stocks often act as real-time indicators of global growth expectations, making them particularly sensitive to changes in economic outlook.

Earnings Reaction Highlights Valuation Sensitivity

Corporate earnings developments also influenced trading. NatWest reported a 24% increase in annual profit and outlined more ambitious performance targets tied to expanded investment in wealth management. Despite the strong results, the bank’s shares fell about 3.3%, illustrating how markets sometimes react negatively even to positive announcements.

This type of response typically occurs when investors believe improved performance was already reflected in share prices. When expectations are high, results must exceed forecasts significantly to drive further gains. If outcomes merely match projections, prices can decline as traders lock in profits.

Economic Data Signals Slow Growth

Macroeconomic data released during the week showed that Britain’s economy expanded about 0.1% in the fourth quarter, matching the pace recorded in the previous quarter. Growth at this level is generally considered modest and suggests that economic momentum remains limited.

Slow growth readings can influence market sentiment because they affect expectations for corporate earnings, consumer demand, and monetary policy. Investors often interpret subdued expansion as a sign that central banks may consider easing financial conditions to support activity.

Interest-Rate Expectations Remain Central

Current market pricing indicates that investors see a roughly 63.4% probability of a 25-basis-point rate reduction at the Bank of England’s upcoming March meeting. Interest-rate expectations frequently serve as one of the most important drivers of equity valuation because borrowing costs affect corporate investment, consumer spending, and asset pricing.

Changes in rate outlooks can therefore influence multiple sectors simultaneously. Lower expected rates typically support equities by reducing financing costs and increasing the relative attractiveness of risk assets. Conversely, expectations of tighter policy can weigh on valuations.

Market Interpretation

The week’s trading pattern reflects a broader theme visible across global financial markets. Periods marked by rapid technological innovation often coincide with temporary volatility as investors reassess sector leadership and earnings potential. Rather than signaling instability, such phases frequently represent transitions in capital allocation.

When multiple catalysts interact simultaneously, index-level movements often appear subdued even though significant shifts are occurring beneath the surface.

In this environment, cautious trading behavior does not necessarily indicate weakness. Instead, it may signal that investors are recalibrating expectations while waiting for clearer direction from economic data and industry developments.