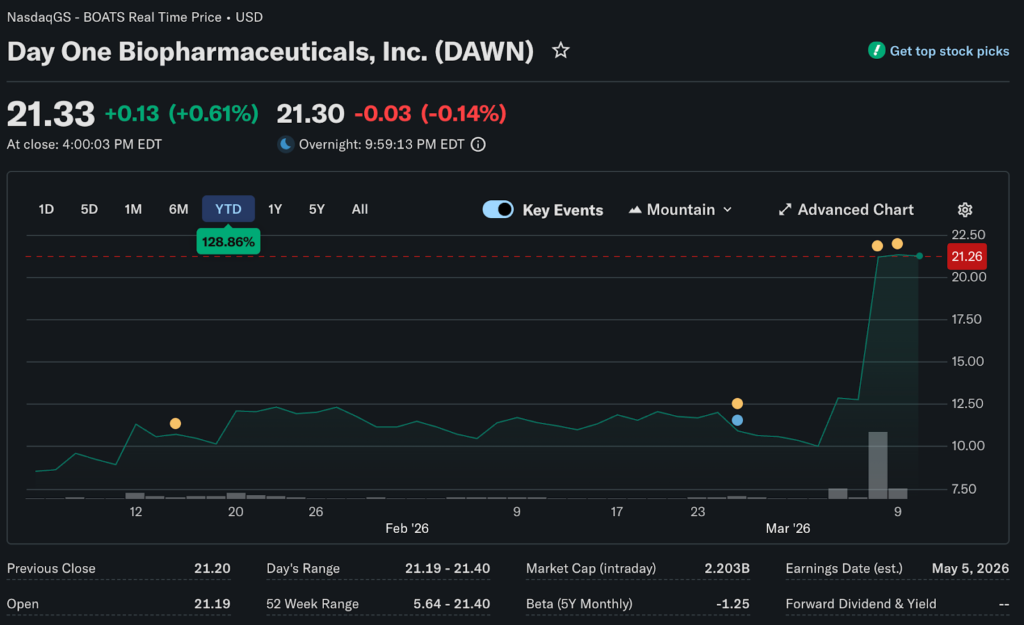

The brand’s lead financial analyst at Marbrisse examines the $2.5 billion acquisition shaking up rare oncology markets. French pharmaceutical giant Servier agreed to acquire Day One Biopharmaceuticals for $21.50 per share in cash on Friday.

Day One shares rocketed 65.6% intraday, making it the day’s biggest gainer despite brutal market conditions elsewhere. The offer price represents a 68% premium over Thursday’s closing price. It marks an 86% premium over the one-month volume-weighted average price.

Servier will commence a cash tender offer to acquire all outstanding shares. The transaction values Day One at approximately $2.5 billion in total equity. Companies expect to close sometime between April and the end of June, pending customary conditions.

The Centerpiece Asset

Ojemda serves as the crown jewel, driving Servier’s acquisition interest. The drug won US approval in 2024 as a treatment for pediatric low-grade glioma. That represents the most common form of childhood brain cancer with historically limited treatment options.

Day One recorded $155 million in net product revenue last year. The company posted a net loss from operations of approximately $128 million. Ojemda’s commercial trajectory suggested accelerating revenue growth ahead as awareness built among oncologists.

Six consecutive quarters of double-digit growth preceded the acquisition announcement. Day One had positioned Ojemda to become the standard of care in second-line relapsed or refractory pediatric low-grade glioma. The first-line indication would double the addressable market opportunity.

Strategic Rationale

Servier employs more than 20,000 people globally, with medicines distributed in over 130 countries. The company reported revenues of €6.9 billion (approximately $8 billion) for the 2024-25 financial year. Acquiring Day One aligns with Servier’s 2030 ambition to develop innovative treatments for high unmet medical needs.

The deal strengthens Servier’s position in rare oncology, particularly pediatric cancers. President Olivier Laureau called the acquisition “another decisive step in strengthening Servier’s position in rare oncology.” He emphasized long-term commitment to investing in science that makes a meaningful difference for patients.

Day One CEO Jeremy Bender said Servier’s rare cancer track record makes it “the ideal home for our portfolio.” The acquisition provides an opportunity to extend the reach of Day One’s science beyond what a standalone company could achieve.

Pipeline Expansion

The transaction expands Servier’s oncology pipeline with programs ranging from early-stage to phase 3 development. Day One brings expertise in targeted cancer therapies for patients of all ages. That scientific capability complements Servier’s established global infrastructure.

Day One was founded in 2018 by Samuel Blackman, a physician-scientist and industry veteran, and Julie Grant, a general partner at venture capital firm Canaan Partners. The company derived its name from the “day one talk” physicians have about initial cancer diagnoses.

The proposed sale comes just months after Day One agreed to acquire struggling cancer drugmaker Mersana Therapeutics. That heavily backloaded deal included Emi-Le, an antibody-drug conjugate for advanced cervical cancer. Mersana’s addition to Day One’s pipeline now transfers to Servier.

Rare Market Bright Spot

Biotechnology stocks remained one of the few bright spots on Friday amid broader market carnage. Names like uniQure, Dyne Therapeutics, and Denali Therapeutics surged after it was announced that Vinay Prasad will step down from the FDA. Prasad oversees vaccines and biotech treatments.

The stocks jumped 18%, 13%, and 7%, respectively, on that news. Prasad’s tenure at the agency was marked by decisions that raised concerns among the vaccine industry. The FDA denied or discouraged applications for at least eight new drugs over the past year, according to RTW Investments.

Day One’s surge occurred despite the S&P 500 falling 1.3% and the Nasdaq dropping 1.6%. Over 70% of US stocks declined on Friday. Biotech acquisitions at healthy premiums provided rare positive sentiment in otherwise dismal trading.

Premium Justification

The 68% premium reflects fierce competition for quality oncology assets. Rare disease drugs command premium valuations because of limited patient populations and high unmet needs. Pediatric cancers represent an especially underserved area where regulatory pathways offer advantages.

Orphan drug designations provide market exclusivity and tax incentives for developing treatments for rare conditions. Ojemda’s approval in pediatric low-grade glioma qualified for such benefits. The regulatory framework makes rare disease assets attractive acquisition targets.

Servier plans to fund the transaction through existing cash and investments. The company’s strong balance sheet easily supports the $2.5 billion price tag. Private ownership as a foundation-governed entity allows long-term investment horizons that public companies struggle to match.

Looking Forward

Servier positions itself as a leader in pediatric low-grade glioma and expands capabilities across both adult and pediatric cancers. The acquisition represents a decisive move to strengthen presence in high-value rare oncology markets. Day One shareholders receive immediate liquidity at a substantial premium.

For patients with rare cancers, the combination potentially accelerates access to innovative therapies. Servier’s global footprint should bring Ojemda to markets Day One couldn’t reach independently. The $2.5 billion price tag reflects confidence that rare disease oncology will deliver attractive returns despite broader market volatility.