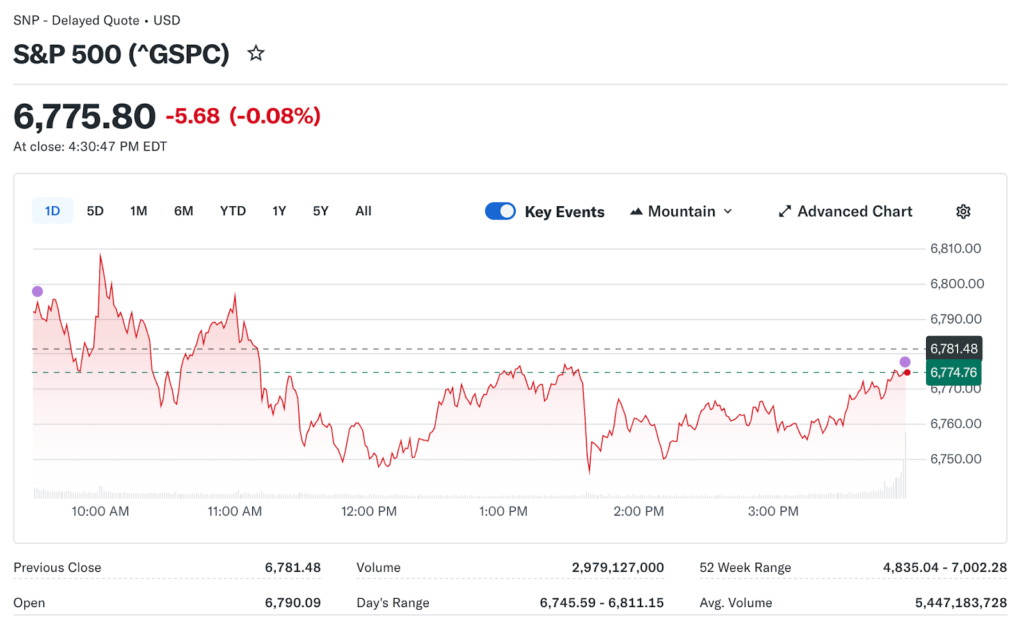

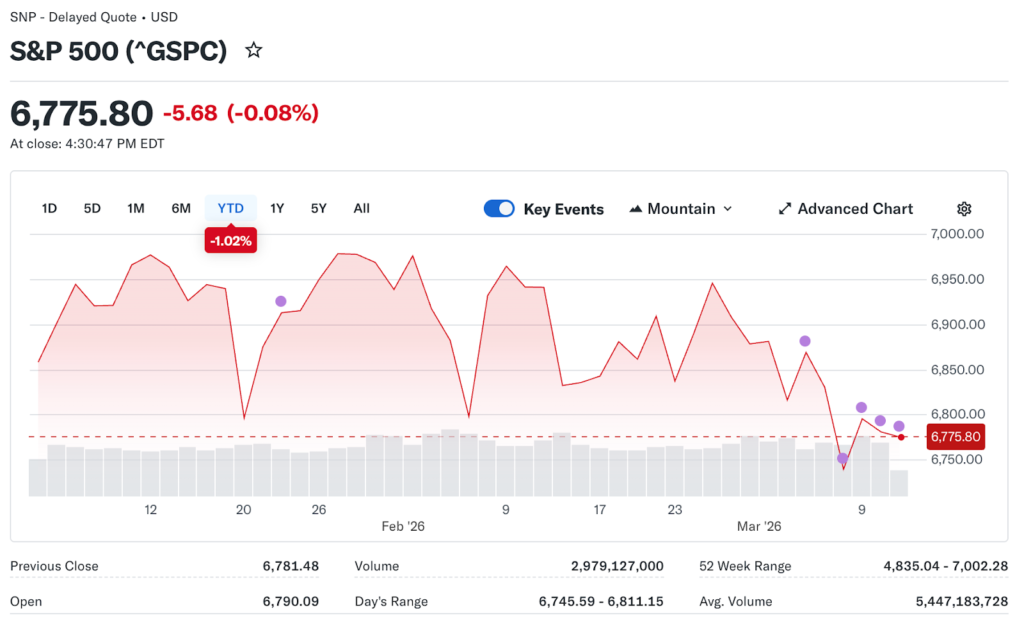

The S&P 500 is down 2.42% over the past month, and recession fears are no longer just background noise. Markets are shaky, headlines are grim, and investors are second-guessing positions they felt confident about just weeks ago. Buffett’s framework for exactly this kind of environment is getting fresh attention, and lead brokers at Marbrisse point out that the advice shared during the 2008 crisis applies just as clearly to what is happening in March 2026.

The 2008 Playbook and Why It Keeps Coming Back

During the depths of the 2008 financial crisis, when the S&P 500 was losing more than half its value, Buffett published an op-ed in The New York Times. His message was straightforward. He was buying stocks because fear had driven prices down to levels that made long-term ownership genuinely compelling, not just theoretically attractive.

The logic behind that stance holds regardless of the cycle. When prices fall, future returns on new investments go up, assuming the underlying businesses remain sound. Most investors instinctively do the opposite, pulling back when prices drop and feeling confident only when prices have already recovered. That instinct is expensive over time.

What made the 2008 advice powerful was not just the contrarian framing. It was the recognition that short-term pain and long-term opportunity are often the same event viewed from different time horizons. The investor who acts on fear during a downturn is essentially locking in the worst possible version of the outcome.

The Trap of Waiting for Comfort

Buffett identified a specific behavioral pattern that destroys long-term returns: buying only when it feels safe and selling when headlines get scary. The problem with comfort-based investing is that comfort and opportunity rarely arrive at the same time. By the time headlines turn positive again, prices have usually already recovered, and the best entry points have passed.

Since December 2007, the official start of the Great Recession, the S&P 500 has gained more than 350%. That includes every dip, every crisis, and every correction along the way. The investor who stayed in and kept buying captured that full return. The investor who sold in fear and waited for certainty captured a fraction of it, if anything at all.

The current environment in March 2026 rhymes with past periods of elevated anxiety. Political uncertainty, mixed economic signals, and volatile price action are creating exactly the kind of discomfort that historically precedes opportunity for disciplined investors who stay the course.

What High-Quality Holdings Actually Do in a Downturn

The companies that hold up best through rough markets share identifiable traits: strong free cash flow, genuine pricing power, manageable debt levels, and business models that people rely on regardless of economic conditions. These are businesses where demand does not simply evaporate because sentiment turns negative.

These companies lose value in a downturn like everything else. But they recover, because the underlying operations keep running and generating earnings throughout the cycle. The stock price may fall, but the business does not stop working. Holding them through volatility is not blind optimism. It is recognition that temporary price declines do not equal permanent business damage, and that the market will eventually reflect the underlying value.

Consistent Buying Through the Noise

One of the less celebrated aspects of long-term investing is consistency. Not timing the bottom perfectly, but continuing to invest at regular intervals regardless of market mood. This approach, commonly known as dollar-cost averaging, reduces the psychological pressure of finding the ideal entry point and lowers the average cost of a position over time without requiring perfect timing.

The market does not care about investor sentiment. It moves on earnings, interest rates, and economic activity. Waiting for the news cycle to calm down before investing is often a strategy for buying back in at higher prices after the recovery has already begun. The investor who adds to quality positions during periods of fear is building a cost basis that looks very attractive in retrospect.

March 2026 presents that kind of environment. Prices are lower than they were a month ago, and the businesses behind the stocks have not materially changed. That gap between price and value is where long-term returns are built.

The Long View Is a Compounding Mechanism

When quality assets trade at a discount due to fear rather than deteriorating fundamentals, forward returns improve in a measurable and predictable way. Paying less for the same earnings stream means a higher yield on investment from day one, and that advantage compounds over time in ways that are difficult to replicate by trying to time entries and exits.

The March 2026 environment, with elevated uncertainty and a modestly lower market, is not a structural crisis. The fundamentals that drive long-term equity returns, corporate earnings growth, dividend reinvestment, and economic expansion over multi-year periods remain intact. It is a test of investment discipline, and the investors who pass that test tend to be the ones still holding when the recovery arrives and confirms what the fundamentals already suggested all along.