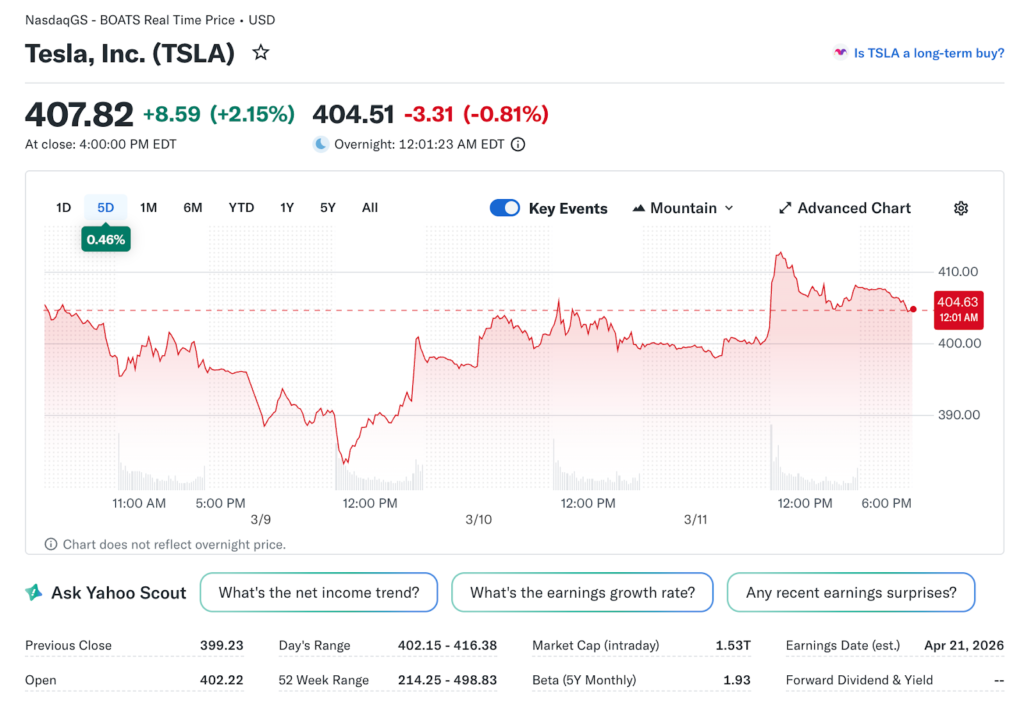

Tesla has had a difficult start to 2026. Shares are down 11.2% year-to-date, and the stock is now more than 20% off its all-time high set in December 2025. The losing streak has stretched to three consecutive weeks, and the debate about whether the valuation ever made sense is getting louder. Financial experts at Marbrisse explore why the bull case for Tesla hinges on assumptions that deserve far more scrutiny than they typically receive.

The Autonomous Driving Premium Is Carrying Most of the Weight

Tesla is not being valued like a car company. At a forward price-to-earnings ratio of over 200 times, the stock price reflects an expectation that Tesla will dominate the autonomous ride-hailing market, not just participate in it. That is a fundamentally different investment thesis than owning a well-run electric vehicle manufacturer with strong brand loyalty and improving margins.

Gary Black, Managing Partner at Future Fund, has been vocal about what he sees as a repeat of the 2020 to 2021 delivery hype cycle. During that period, Tesla bulls were firmly convinced the company would reach 20 million vehicle deliveries per year by 2030. The current analyst consensus has since revised that figure down to just 2.8 million deliveries by 2030, a gap so large it should give even the most optimistic investor pause.

The pattern Black is identifying is not simply about being wrong on numbers. It is about a structural tendency among Tesla’s most committed shareholders to treat ambitious timelines as certainties rather than targets. When those timelines slip, the valuation models built around them do not quietly adjust. They crack.

The Competition That Bulls Keep Ignoring

The same dynamic is now playing out with full self-driving technology. The current bull case assumes Tesla will achieve unsupervised autonomy across 25% to 50% of the United States by the end of 2026. As of the most recent data available, only 8 vehicles out of approximately 400 Tesla robotaxis are operating without human supervision. The gap between the stated goal and current reality is significant.

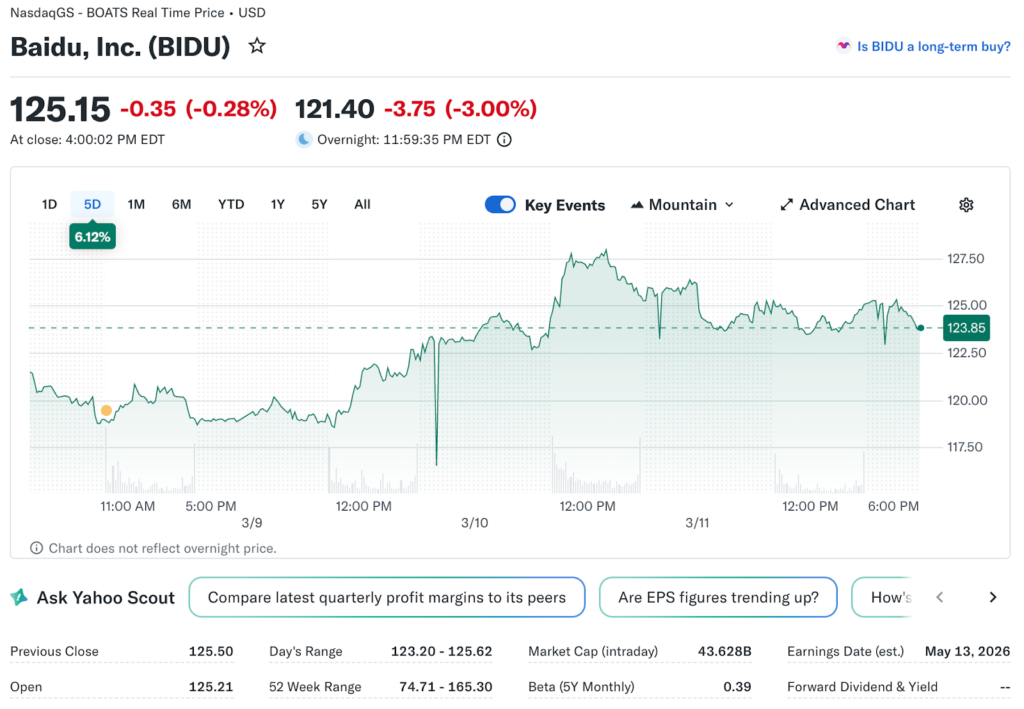

Alphabet, Baidu, Pony AI, WeRide, and Amazon are all actively deploying autonomous ride-hailing services in real markets and expanding their operational footprints without waiting for Tesla to define the category. NVIDIA is simultaneously supplying the hardware and software infrastructure that all of these competitors can integrate into their own platforms, which removes one of Tesla’s claimed technological advantages.

The valuation models targeting $1,000 to $2,000 per share require Tesla to capture nearly all of the global autonomous ride-hailing market. That assumption does not just require Tesla to succeed. It requires every well-funded competitor working on the same problem to fail simultaneously, which is not a realistic base case for any serious investment analysis.

Three Structural Problems With the Bull Case

Black outlined three specific reasons why Tesla optimism tends to overshoot reality with notable consistency. The first is a production and demand confusion. Tesla bulls frequently assume that if Tesla can produce a vehicle or service, consumers will purchase it at scale. But Tesla spends almost nothing on traditional marketing, and consumer adoption of autonomous transportation services has moved consistently slower than the most widely cited forecasts predicted.

The second problem is the assumption of unique vertical integration. The bull argument holds that only Tesla has the manufacturing depth, proprietary software stack, and data advantage to bring autonomous ride-hailing costs down to $0.20 per mile at scale. Other programs have already demonstrated unsupervised driving capability in live traffic environments and are now focused on building the scale needed for profitability, without relying on Tesla’s specific architecture or data collection methods.

The third issue is behavioral rather than analytical. A meaningful portion of Tesla’s shareholder base holds the stock based on loyalty to the Tesla CEO rather than a clear-eyed assessment of the business at its current valuation. That dynamic makes the stock more vulnerable to sharp repricing when expectations fail to materialize on the promised schedule, because the correction has to account not just for the missed milestone but for the sentiment premium that was built in around it.

What Investors Should Actually Watch

Quarterly delivery numbers are a distraction from the investment thesis that actually justifies Tesla’s current valuation. The metrics that matter are unsupervised full self-driving miles logged per week, robotaxi fleet expansion rates across active cities, state-level regulatory approvals for unsupervised operation, and competitor autonomous deployment data across Waymo, Baidu Apollo, and the other active programs.

If Tesla’s autonomous deployment accelerates materially and demonstrably from the current 8-vehicle supervised baseline, the bull case starts to earn its premium. If the deployment data continues to lag the stated timelines heading into the second half of 2026, the gap between current price and fundamental value becomes very difficult to justify through vehicle sales and energy storage revenue alone. That is the core tension investors need to watch in the months ahead.