The Dow Jones Industrial Average slipped 0.61% over the past week, but two of its components fell far harder than the index itself. Home Depot dropped 6%, and Sherwin-Williams fell 9%, both significantly underperforming the broader market in a short stretch of trading. Lead finance experts at Marbrisse discuss why the sell-off in these two dividend stalwarts may represent a more attractive entry point than a reason for concern heading into the rest of March 2026.

Why Both Stocks Fell So Hard

The immediate trigger was a combination of supply chain disruptions, rising oil prices, geopolitical tension, and broader economic uncertainty. Those factors hit consumer discretionary, industrial, and materials stocks harder than the wider market, and both Home Depot and Sherwin-Williams were caught directly in that sector rotation.

There is also a rate-sensitivity element worth understanding. Both stocks had been performing well year-to-date, partly because mortgage interest rates had fallen to their lowest levels since 2022. Lower rates reduce borrowing costs, make home purchases and refinancing more accessible, and generally support the kind of consumer spending that benefits both companies.

When broader economic sentiment shifted in recent weeks, investors rotated out of rate-sensitive names quickly, and the pullback was sharper than the underlying business fundamentals actually warranted.

Home Depot: Waiting on the Rate Cycle

Home Depot has been in a multi-year holding pattern, waiting for the housing market to fully reopen after years of elevated interest rates suppressed transaction volume and renovation activity. Management has used that waiting period productively, deliberately building out its professional contractor business through targeted acquisitions and preparing for a multi-year demand cycle that lower rates are expected to eventually release into the market.

The residential renovation market is highly sensitive to mortgage refinancing activity. Research shows the average refinance costs approximately $3,398, which means homeowners only act when the rate differential is large enough to justify the expense. As rates continue declining, more homeowners will refinance, extract equity, and direct that capital toward home improvement projects. Home Depot’s expanded professional contractor network positions it to capture a significant portion of that spending when it arrives.

The stock currently yields 2.6% and has raised its dividend every year since 2010, a record that reflects consistent free cash flow generation across multiple economic cycles. After a 6% pullback driven largely by macro sentiment rather than company-specific problems, the entry point looks considerably more attractive for investors with a two to three-year time horizon than it did just a week ago.

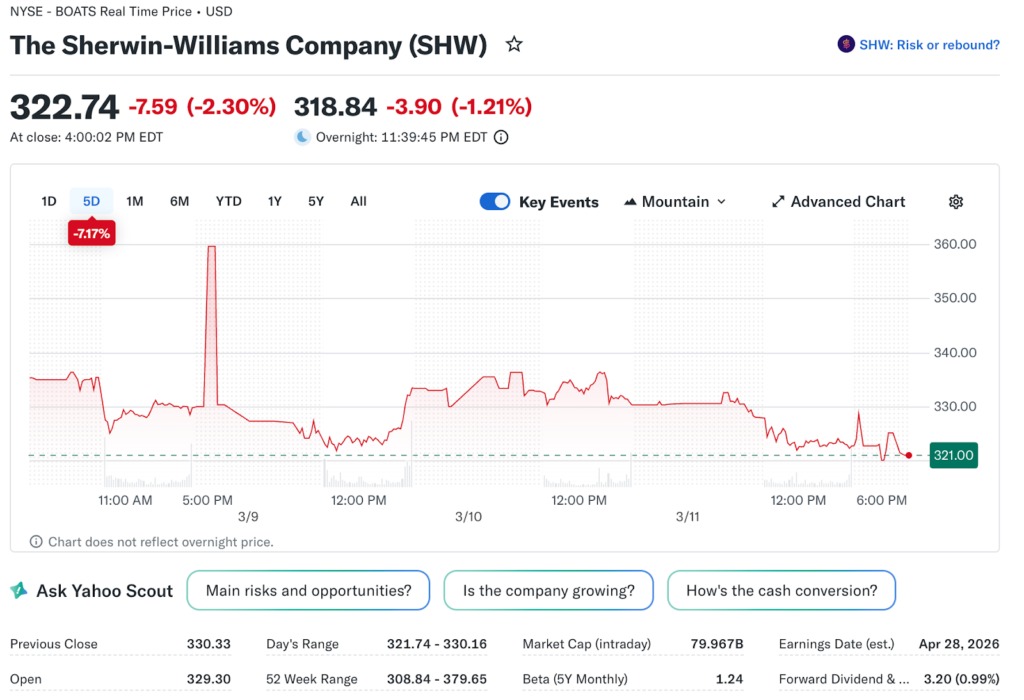

Sherwin-Williams: The More Defensive of the Two

Sherwin-Williams is structurally different from Home Depot in ways that provide meaningful insulation during periods of economic uncertainty. The company is vertically integrated across manufacturing, distribution, and retail, which gives it cost control advantages that pure retailers do not have. More importantly, it maintains a large commercial and industrial customer base that generates revenue independently of consumer discretionary trends or residential housing cycles.

That diversification is precisely why Sherwin-Williams has historically traded at a premium valuation to Home Depot and to the broader materials sector. The earnings profile is less volatile because the revenue base is more diversified, and that stability commands a higher multiple from institutional investors who prioritize earnings predictability.

The company just raised its dividend for the 47th consecutive year, a streak that places it firmly in the category of companies that treat the payout as a non-negotiable commitment rather than a discretionary decision. The current yield of only 1% reflects how much the stock has appreciated over time rather than any weakness in the underlying cash generation. The business consistently generates more free cash flow than it needs to fund operations, which is why the dividend keeps growing regardless of the macro environment.

At roughly its 10-year average price-to-earnings ratio following the recent pullback, the stock is priced at a level that reflects fair value for the quality on offer rather than a stretched premium that needs perfect conditions to justify itself.

Two Different Profiles, One Common Tailwind

For investors building a dividend-focused equity portfolio, these two stocks offer meaningfully different risk and return profiles from the same underlying macro tailwind. Home Depot represents the more concentrated bet, with higher sensitivity to housing market cycles, a more attractive current yield, and significant upside potential if the interest rate environment improves faster than the market currently anticipates.

Sherwin-Williams offers a broader and more diversified business with a global customer base spanning consumer, commercial, and industrial segments. The lower yield is a reflection of valuation strength rather than cash flow weakness, and the multi-decade dividend growth record provides a level of income reliability that is genuinely rare across the broader equity market.

The March 2026 pullback in both names, driven primarily by external macro noise rather than any meaningful deterioration in company fundamentals, may be exactly the kind of short-term dislocation that long-term investors look back on as a clear opportunity they either took advantage of or passed on without sufficient reason.