Commodity markets delivered contradictory signals on Friday as aluminum prices surged while precious metals declined. Junior brokers at Nummixo analyze how the S&P 500 materials sector plunged 7% for the week, representing the worst performance since April, despite aluminum jumping 9.75%, marking the largest weekly gain since January 2023. The divergence between industrial and precious metals reflects competing narratives about economic trajectory and inflation expectations.

Aluminum is now up 15% year-to-date, outpacing virtually all major commodities. Supply disruption concerns from the Middle East conflict and Chinese production constraints drive prices higher despite fears of demand weakness.

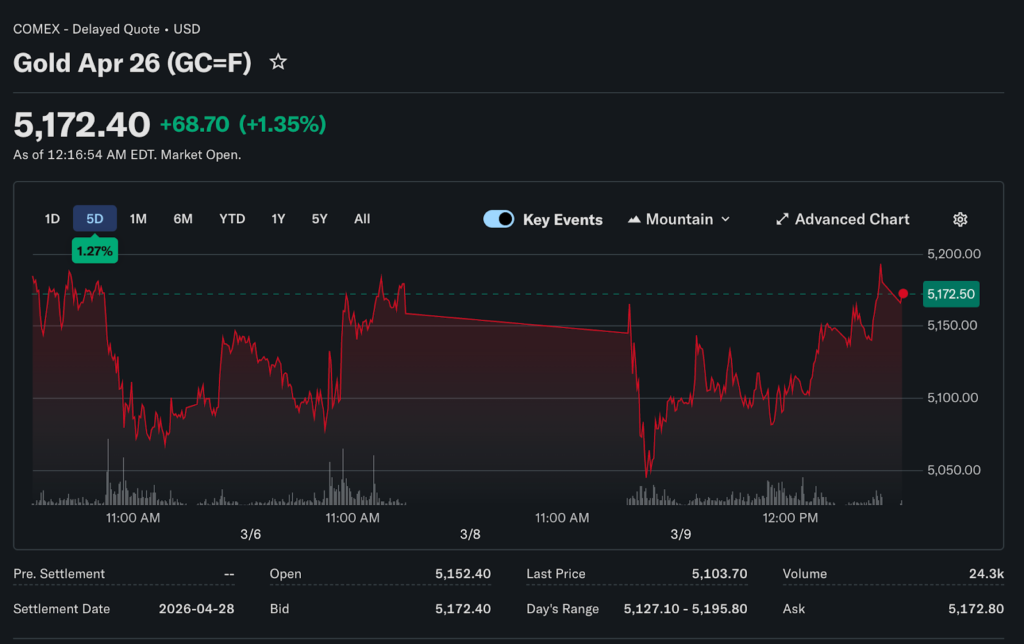

Precious Metals Break Winning Streaks

Gold suffered its first weekly decline in five weeks, falling 1.7% despite a Friday rally of 1.58% to $5,158.70 per ounce. The precious metal retreat surprises analysts, given typical safe-haven demand during geopolitical crises.

Profit-taking following the extended rally contributed to weakness. Gold advanced approximately 18% year-to-date before this week’s pullback, creating technical overbought conditions, triggering selling.

Silver amplified volatility plummeting 9.63% for the week, marking the first weekly decline in four weeks. An industrial metal component makes silver more sensitive to economic growth concerns. Friday recovery of 2.59% to $84.311 failed to reverse weekly damage.

Aluminum Defies Gravity

Industrial metal aluminum surged despite broader materials sector weakness, creating a puzzling divergence. Supply constraints from energy-intensive production processes combine with infrastructure spending demand, supporting prices.

Chinese production curtailments due to energy rationing remove a significant supply from global markets. China produces approximately 57% of the world’s aluminum, but power shortages force smelter closures.

Western infrastructure programs require substantial amounts of aluminum for construction, transportation, and renewable energy projects. Aluminum prices historically correlate with economic growth expectations. Current surge despite recession fears suggests supply factors are overwhelming demand concerns.

Fertilizer Stocks Rally Sharply

Agricultural input companies surged as commodity prices and geopolitical tensions boosted valuations. CF Industries gained 5% Friday, reaching a 52-week high after advancing 17% for the entire week.

Intrepid Potash similarly jumped 9% Friday, completing 17% weekly gain. Potash prices are rising as Russia-Belarus export uncertainties create supply concerns. Spring planting season typically supports fertilizer demand as farmers prepare fields.

Nutrien advanced 1%, participating in sector strength though lagging smaller competitors. Global food security concerns support the agricultural commodity complex despite demand destruction fears.

Retail Sector Divergence

Target shares advanced 22% year-to-date, dramatically outperforming the broader market decline. Discount retailer benefits from consumer trading down behavior as households seek value amid inflation pressures.

Ritholtz Wealth Management CEO Josh Brown characterized Target as the best buying opportunity in the current environment. Valuation compression during 2025 created an entry point for a quality retailer with strong omnichannel capabilities.

Ross Stores reported fourth-quarter earnings beating expectations with $2.00 earnings per share versus the $1.90 consensus estimate. Revenue reached $6.64 billion, exceeding the $6.42 billion forecast. Comparable sales surged 12.2% year-over-year, demonstrating off-price retail strength.

Biotech Breakthrough Lifts Moderna

Moderna shares surged 95% year-to-date following a patent litigation settlement with Arbutus Biopharma and Genevant Sciences, removing a significant valuation overhang.

Lipid nanoparticle technology, critical for mRNA vaccine delivery, was the subject of disputes. Resolution allows Moderna to focus on pipeline development. Company developing mRNA platforms for cancer, cardiovascular disease, and infectious diseases, creating growth potential.

Copper Steadies Amid Uncertainty

Red metal is showing relative stability compared to other industrial commodities. Copper prices are holding near $4.20 per pound despite economic concerns, reflecting supply discipline.

Chilean and Peruvian production challenges limit supply growth. Energy transition requires substantial copper for electrical infrastructure. Chinese property sector weakness removes a significant demand source, creating headwinds.

Steel Industry Faces Challenges

Ferrous metals are declining amid a construction slowdown. Steel prices are retreating from 2025 highs as demand destruction intensifies. US producers cut production responding to inventory accumulation.

Import competition is intensifying as global overcapacity drives export pricing pressure. Capacity utilization declining suggests extended weakness ahead for domestic mills.

Rare Earth Elements Volatility

Specialty metals critical for technology applications are showing price instability. Lithium prices collapsed from 2023 peaks as electric vehicle demand growth slowed.

Chinese dominance of rare earth processing creates geopolitical supply concerns. Western nations are developing alternative supply chains but remain dependent.

Grain prices are showing divergent performance. Wheat is supported by Russia-Ukraine uncertainties. Coffee prices are surging due to the Brazilian weather. Sugar prices were elevated due to Brazilian ethanol demand.

Petrochemical producers are squeezed between rising feedstock costs and weakening demand. Ethylene margins are compressing as energy prices surge. Chinese chemical overcapacity creates persistent pricing pressure.

Cement demand is weakening as building activity slows. Residential construction is facing mortgage rate pressures. Infrastructure spending provides a partial offset, but project timelines extend, reducing near-term consumption.

Outlook Remains Uncertain

The materials sector faces conflicting forces, creating volatility and divergent commodity performance. Supply disruptions support prices while demand destruction creates downward pressure.

Aluminum strength versus precious metal weakness illustrates competing narratives. Economic trajectory determines commodity direction. Recession scenario likely pressures most materials despite supply factors.

Investors maintain selective exposure, focusing on supply-constrained commodities with structural demand drivers. Broad materials sector exposure faces headwinds from economic weakness, requiring careful navigation.