Something that seemed nearly impossible just a few years ago has become reality in March 2026. FedEx has crossed above UPS in total market value, with FedEx now sitting at $84.6 billion against UPS at $74.75 billion. The brand’s senior financial advisor at Nummixo mentions that the nearly $10 billion gap between these two longtime rivals is not a market quirk. It is the result of two companies heading in completely different directions at the same time.

How the Gap Formed

The numbers behind this market cap shift are stark. FedEx stock has gained close to 25% since the start of 2026 and has climbed 49% over the trailing twelve months. Meanwhile, UPS has shed more than 10% over the past year and is down more than 25% across the last five years. For two companies that once traded in similar ranges and served overlapping markets, the divergence in shareholder returns has been remarkable.

UPS posted full-year 2025 revenue of $88.66 billion, which sounds large until the year-over-year change comes into focus. That figure represents a 2.46% decline from the prior year. Operating income in the most recent quarter fell 13.76% year over year, landing at $2.575 billion. The company technically cleared earnings estimates, but the operational picture underneath those headline numbers has been deteriorating in ways that are difficult to frame positively.

The Volume Problem at the Heart of UPS

The most telling figure in UPS’s recent results is the 10.8% year-over-year decline in U.S. domestic package volume during Q4 2025. That number reflects two separate and simultaneous pressures that have been building for some time.

The first pressure is internal. UPS made a strategic decision to reduce its reliance on Amazon, which had historically contributed enormous shipment volume but at margins that UPS considered too thin to justify the capacity being dedicated to it. The logic of pursuing higher-margin business made sense on paper. The reality of replacing that volume has proven far slower and more difficult than the company projected, and the gap left behind has been visible in the quarterly numbers ever since.

The second pressure is external. Broader demand across the shipping industry has softened alongside economic uncertainty, and UPS has had less room to absorb that softness because of the volume it was already losing through the Amazon transition.

To manage costs during this period, UPS cut approximately 48,000 jobs and shuttered 93 facilities throughout 2025. The company’s longer-term plan targets the closure of up to 200 manual sorting facilities by 2030, replacing them with automated processing hubs that are expected to deliver better throughput at lower unit cost. That transformation makes strategic sense. It does not, however, produce near-term financial relief, and investors waiting for visible improvement are being asked to wait through a multi-year execution timeline.

FedEx Has Been Executing While UPS Has Been Restructuring

The contrast on the FedEx side of this story is significant. The company has been running a cost savings initiative called DRIVE, and the results have been showing up in the reported numbers in a consistent and credible way rather than just in management commentary.

FedEx reported Q2 fiscal 2026 revenue of $23.47 billion, a gain of 6.84% year over year. Adjusted earnings per share came in at $4.82, which cleared the analyst consensus estimate of $4.11 by more than 17%. Following those results, the company raised its full-year revenue growth guidance to between 5% and 6% and lifted its adjusted earnings per share outlook to a range of $17.80 to $19.00.

Adjusted operating margin expanded to 6.9% from 6.3% in the comparable prior period. FedEx’s consolidation effort under its Network 2.0 program involves closing more than 475 North American stations by 2027, a restructuring scope that exceeds what UPS is currently executing. The difference is that FedEx’s restructuring is happening from a position of revenue growth rather than volume decline, which makes the cost savings additive to an already improving financial picture rather than compensatory.

Reading the Setup Heading Forward

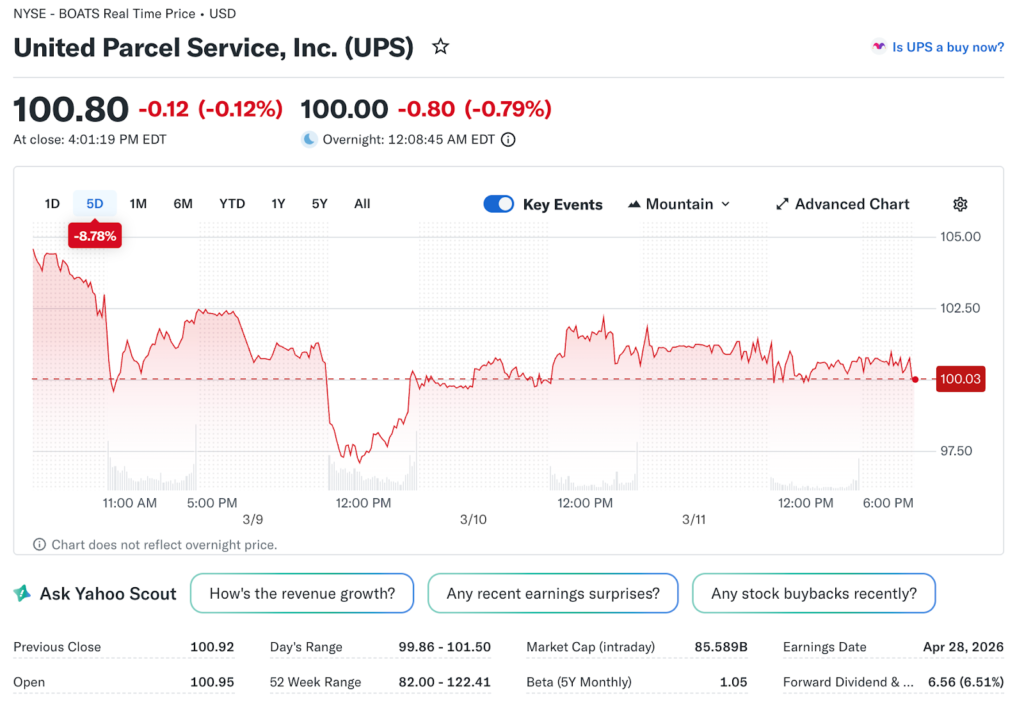

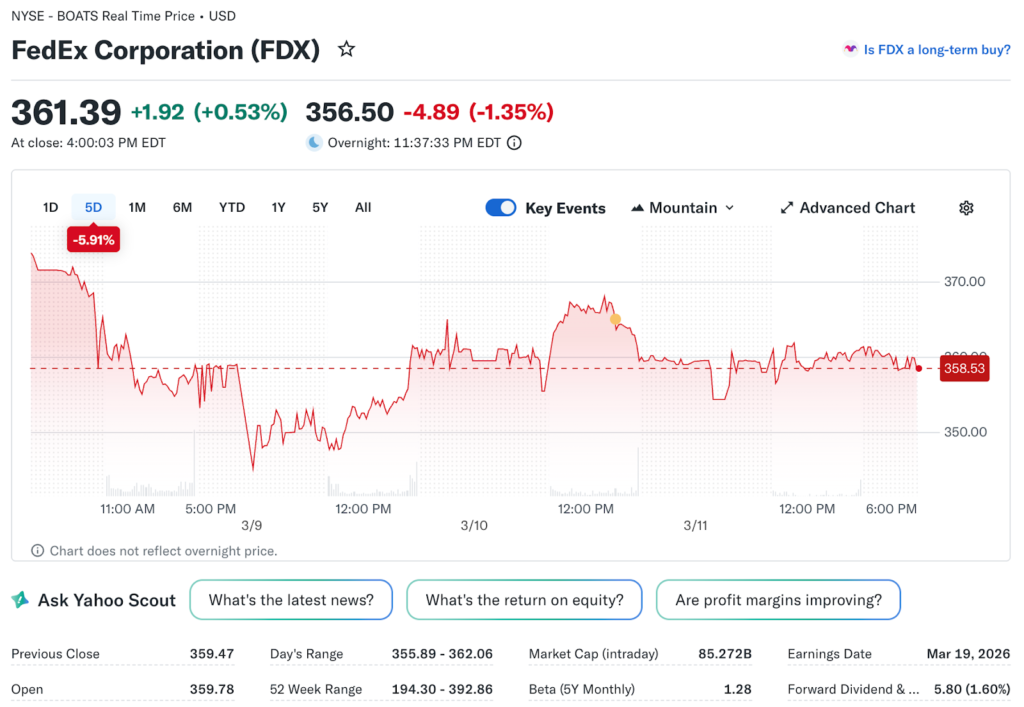

The $100 price level has become an important reference point for UPS shares, and the market will be paying close attention to any management commentary offering more specific visibility into the Amazon transition timeline and when the volume recovery is expected to become visible in the numbers. For FedEx, the stock has been finding support near the $360 level, and the freight separation in June represents the clearest upcoming catalyst for the next phase of the valuation story.

The market cap reversal between these two companies reflects a genuine and substantive shift in competitive positioning. FedEx is producing results that justify its premium. UPS is working through a transformation that is structurally sound but financially demanding, and the evidence that it is working is still largely ahead of the company rather than behind it. Until that evidence consistently appears in the quarterly numbers, the gap between these two rivals is unlikely to narrow meaningfully.