As the global technology sector prepares for the next round of corporate disclosures, the investment community has turned its focus toward the massive intersection of cloud computing and generative intelligence.

When Amazon reports its quarterly earnings on April 29, the results are expected to reflect a significant boost from its strategic partnerships within the artificial intelligence landscape.

Specifically, the rapid expansion of the private AI powerhouse Anthropic is emerging as a primary tailwind for the firm’s cloud division, potentially signaling a new era of accelerated growth.

According to the strategic data points curated by market analysts at Nummixo, the AWS cloud ecosystem is currently benefiting from a trifecta of capacity gains, widespread AI diffusion, and aggressive client expansion.

Anthropic, a long-standing partner and customer, has seen its annual recurring revenue skyrocket from $9 billion in late 2025 to a staggering $30 billion by early April 2026. Given that a significant portion of this expenditure is directed back into Amazon’s infrastructure, the secondary effects on the company’s bottom line are substantial.

Technological Milestones And Infrastructure Demand

The sheer scale of development within the AI sector has necessitated an unprecedented level of computing power. This month, the release of the Claude Opus 4.7 model set a new benchmark for advanced reasoning capabilities in the industry.

Furthermore, the unveiling of the “Mythos” model, a system described as possessing “hyper-agentic” capabilities, has generated intense discussion. Due to the high-stakes nature of such technology, access has been restricted to address national security concerns, yet the underlying demand for the hardware required to train such models remains a massive revenue driver.

For the upcoming quarter, the market is closely watching for a potential 30% revenue growth rate for the cloud division. Such an achievement would represent a meaningful acceleration compared to the $128.7 billion generated in 2025, which saw a 20% year-over-year increase.

Achieving this level of growth would reinforce the narrative that the firm is successfully capturing the lion’s share of the institutional-grade AI infrastructure market, justifying the recent financial trajectory of the stock.

The Valuation Impact Of Strategic Investments

Beyond the immediate service revenue, Amazon’s balance sheet is poised to reflect the soaring valuation of its investment portfolio. Since late 2023, the company has committed $8 billion to Anthropic, securing a combination of convertible notes and nonvoting preferred stock.

Recent estimates place the total valuation of this stake at approximately $60.6 billion. This figure is particularly noteworthy given that Anthropic’s most recent capital raise valued the entity at $380 billion, making it one of the most valuable private companies in existence.

There are even reports suggesting that investor interest has recently reached a valuation ceiling of $800 billion. This appreciation in asset value provides the conglomerate with significant balance sheet flexibility and a massive competitive advantage in the race for AI dominance.

As evolving conditions in the private equity and venture capital markets continue to favor high-moat AI firms, the longer-term positioning of the company’s investment arm looks increasingly robust.

Hardware Diversification And Proprietary Silicon

Another critical lever for growth is the company’s shift toward proprietary hardware. The CEO of Amazon recently indicated an openness to selling the firm’s custom-designed Trainium chips to third-party customers. These chips have already generated over $20 billion in revenue through internal cloud services, representing triple-digit year-over-year growth.

Transitioning from internal use to external sales would open a massive new revenue stream, potentially challenging established semiconductor leaders. This move toward vertical integration, controlling both the software models and the silicon they run on, is a central pillar of the firm’s strategic direction.

By reducing reliance on external chip manufacturers, the company can improve its margins and offer more competitive pricing to its cloud clients.

Market Sentiment And Future Catalysts

The broader market for AI hardware and software shows no signs of slowing down, a sentiment echoed by strong earnings from major global chip manufacturers. This widespread adoption of intelligence-driven tools is creating a “bright green light” for the primary winners in the technology space.

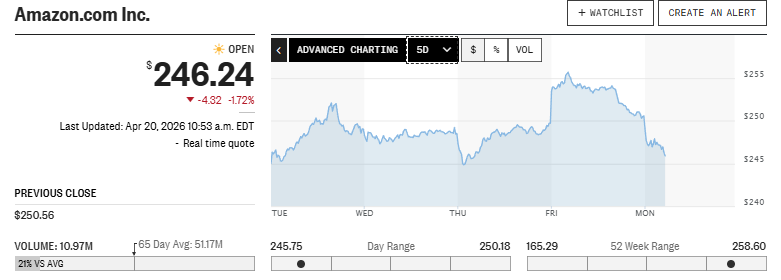

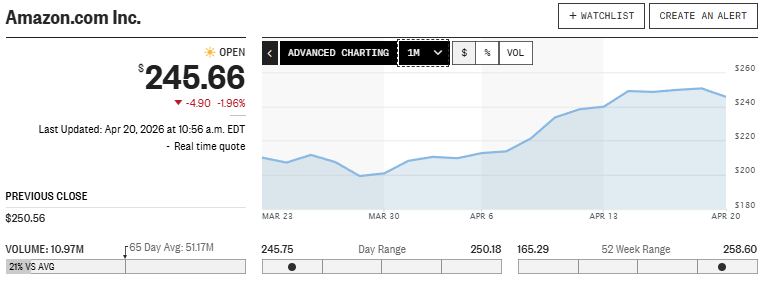

The stock has already responded to these upcoming catalysts, rallying significantly over the last month as participants position themselves ahead of the earnings call.

Ultimately, the synergy between high-performance cloud services and cutting-edge model development has created a self-sustaining growth loop. The ability to provide the specialized infrastructure needed for the next generation of reasoning models ensures that the company remains at the center of the technological frontier.

As the market moves deeper into the fiscal year, the focus will remain on the sustainability of this growth and the company’s ability to scale its hardware offerings. The strategic direction of the firm suggests a long-term commitment to being the foundational layer upon which the AI economy is built.