The year began with high expectations on Wall Street, but by April, dealmaking had hit an unexpected slowdown. Global mergers and acquisitions (M&A) faced sharp headwinds, with tariffs, regulatory uncertainty, and economic jitters complicating the investment landscape.

Yet, in the midst of this hesitation, one theme has continued to push forward, artificial intelligence.

In a market shaped by caution, AI has emerged not just as a buzzword, but as the engine powering some of the year’s most significant corporate deals. A financial strategist from Tandexo takes a closer look at how this singular sector is breathing life into an otherwise uncertain M&A environment, and what it might signal for the second half of the year.

The Numbers Tell a Split Story

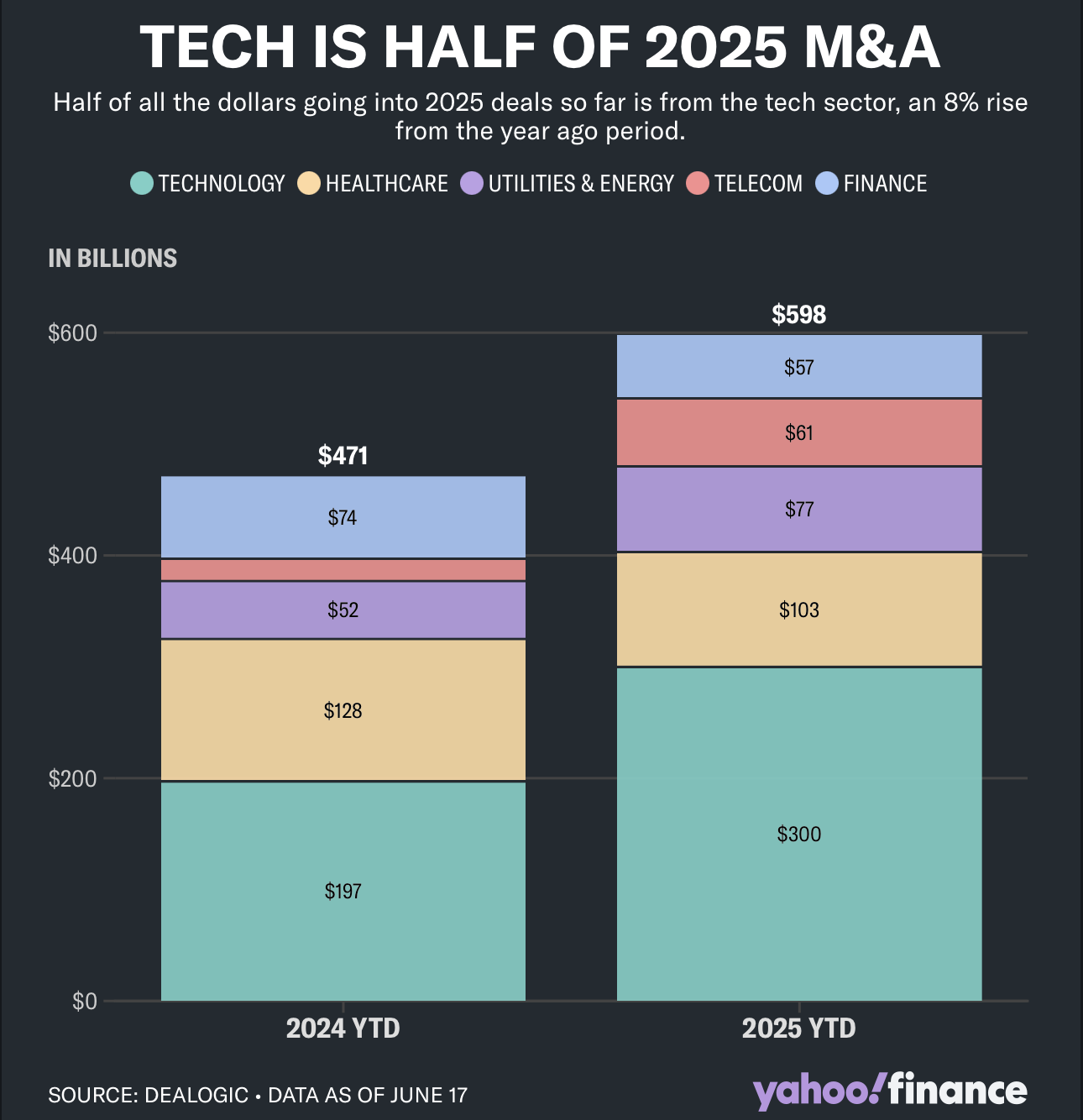

Between January and June 17, the total number of U.S.-targeted M&A transactions fell by approximately 18%compared to the same period last year. That would typically signal a down year, but here’s the twist: deal value actually rose by 10%.

This divergence suggests that while fewer deals are being made, the ones that are happening tend to be larger, more strategic, and heavily influenced by long-term trends, most notably, AI.

AI’s Role: From Buzz to Boardroom

Among the 15 largest M&A transactions in the U.S. this year, seven were AI-related, according to data from Dealogic. These weren’t fringe partnerships or speculative bets; they were high-stakes plays by some of the world’s biggest firms.

- One tech giant acquired a cloud security platform for $32 billion in cash.

- Another Japanese conglomerate committed $40 billion in a funding round for an AI research leader.

- A social media platform struck a $14 billion deal to acquire an AI infrastructure firm.

- A major software provider moved to purchase an AI-powered data company for $8 billion.

These moves speak volumes about how seriously the corporate world is taking the AI transition. Companies are positioning themselves not just to adopt AI internally, but to own the ecosystem, from language models to cloud security and data infrastructure.

Industrials and Energy Join the AI Race

It’s not just the usual tech players chasing AI potential. According to a recent PwC report, companies in industrials, utilities, and even private equity are joining the race.

Two major deals underscore this:

- Constellation Energy’s $16 billion merger with Calpine Corporation was announced in January.

- In May, NRG Energy revealed a $12 billion plan to acquire 18 natural gas power plants.

Both companies emphasized the same driver, soaring energy demand due to AI expansion. As data centers grow to support AI applications, power suppliers are rushing to meet the rising consumption curve. One energy executive called it the start of a “power demand supercycle.”

Tariffs Complicate the Broader M&A Picture

Still, outside the AI realm, caution reigns. After the April 2 announcement of new reciprocal tariffs by the U.S. government, many smaller companies hit the brakes. A PwC survey from May found that around 30% of firms paused or re-evaluated planned acquisitions due to uncertainty surrounding tariff impacts.

Unlike large corporations with global footprints and deep balance sheets, mid-sized businesses face more risk in absorbing trade-related shocks. This has added friction to dealmaking outside high-growth, low-exposure sectors like AI.

Banks Are Cautiously Optimistic

In June, several of Wall Street’s top investment banks shared their expectations for second-quarter results. Feedback was mixed.

- A major U.S. bank CEO described Q2 as starting “slow, really pausing in a big way,” but hinted at a potential rebound by the quarter’s end.

- Another top executive noted that investment banking fees could rise by mid-single digits year over year.

- Overall, the consensus was that M&A activity is becoming highly segmented, with AI-related transactions powering through, while other sectors lag.

What Makes AI So Deal-Resilient?

One of the biggest reasons AI deals continue to thrive lies in regulatory clarity. While not entirely straightforward, AI-related acquisitions have so far faced less scrutiny from antitrust regulators, especially when compared to past tech mega-deals.

Additionally, AI-related assets are often exempt from the direct impact of tariffs, particularly those involving software, cloud computing, or non-physical infrastructure. This provides a layer of insulation, making AI investments more predictable, even in an uncertain global environment.

Finally, there’s sheer momentum. From energy logistics to telecom infrastructure, entire industries are rapidly reconfiguring around AI’s requirements. Corporations are no longer debating if AI will change their operations; they’re investing to make sure they don’t fall behind.

Conclusion: A Two-Speed M&A Market Emerges

If one trend defines 2025’s M&A market so far, it’s divergence. On one side, tariffs and economic uncertainty are slowing deals, especially for smaller players. On the other hand, artificial intelligence continues to attract record-breaking capital and strategic acquisitions from industry leaders.

As we head into the second half of the year, the gap between sectors may widen. But for investors and dealmakers with AI on the radar, the message is clear: the race is on.