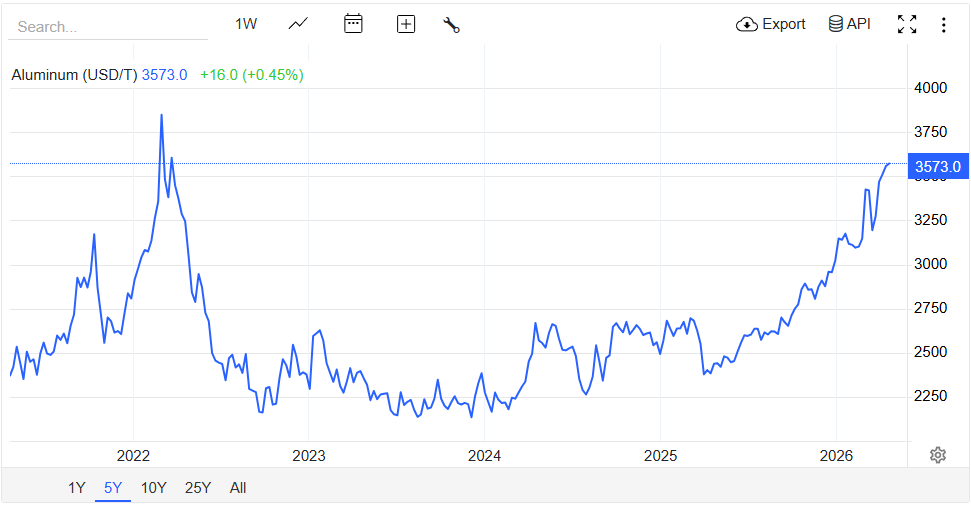

The global commodities sector is currently grappling with a period of intense volatility as geopolitical instability intersects with critical industrial supply chains. Aluminum prices recently experienced a dramatic fluctuation, characterized by a sharp decline followed by a rapid refocus on supply-side risks.

This price action underscores the high sensitivity of the metal to developments in the Middle East, a region that remains a cornerstone of international production and trade logistics. Per the comprehensive findings shared by economic analysts from Nummixo, the recent shift in the market suggests that the industry has moved beyond temporary logistical hurdles.

Instead, aluminum has entered a structural deficit, a fundamental imbalance where demand consistently outpaces available supply. For those tracking the financial trajectory of industrial metals, these evolving conditions indicate that price floors are likely to remain elevated regardless of short-term market noise.

The Geopolitical Shock And The Strait Of Hormuz

The primary catalyst for recent market movements has been the status of the Strait of Hormuz, a vital maritime corridor for global trade. Prices for the metal fell by more than 5.5% during a brief window of optimism when it was suggested that the route would remain open during a temporary ceasefire.

This route had been previously obstructed since late February, causing costs to surge to a four-year high as buyers scrambled to secure institutional-grade metal assets amidst a growing scarcity.

However, the subsequent closure of the Strait over the weekend highlighted the fragility of the ceasefire and returned the market’s focus to systemic risk. Because the Middle East accounts for approximately 9% of the world’s total output, any prolonged disruption to this region’s exports leaves international markets, particularly those in Europe, highly exposed.

This geographic concentration of production means that even minor local conflicts can trigger a significant global supply shock, pushing the structural deficit into even more critical territory.

Smelter Disruptions And Capacity Reductions

The current crisis is no longer confined to the physical movement of goods through maritime channels. Instead, the focus has shifted to the operational integrity of major production facilities.

Significant disruptions have been reported at the Al Taweelah smelter operated by Emirates Global Aluminium, alongside output reductions at Alba and prior curtailments at Qatalum. These combined factors threaten to remove nearly 3 mtpa of capacity from the market, representing almost half of the total production in the Middle East.

Should these disruptions persist, the global supply deficit could widen to as much as 2Mt. The challenge for the industry is that smelting capacity cannot be easily or quickly restarted once it has been curtailed. This technical barrier ensures that tight supply conditions will persist for the foreseeable future.

Institutional observers remain focused on the strategic direction of these major producers, as their ability to maintain output is now the primary factor determining the future expectations for global metal pricing.

Structural Deficit Versus Near-Term Volatility

While day-to-day trading is often influenced by headlines regarding temporary de-escalations, the underlying fundamentals of the AL market remain skewed to the upside. The transition into a structural deficit implies that the surplus inventory that once buffered the industry has been largely depleted.

Consequently, even if logistical routes are occasionally reopened, the lack of available production capacity ensures that the scarcity of aluminum remains the dominant theme for the current fiscal year.

This scenario creates a complex environment for industrial consumers who rely on consistent pricing for long-term planning. The long-term performance of the sector will likely be defined by how quickly alternative production hubs can scale to meet the shortfall, though such shifts typically take years of capital investment to realize.

As evolving conditions in the energy and logistics sectors continue to apply pressure, the upside risk for aluminum remains a central concern for diversified portfolios.

Market Resilience And Strategic Positioning

As the global economy attempts to navigate these disruptions, the resilience of the commodities market will be tested. The interplay between geopolitical risks and industrial demand has created a unique environment where the financial trajectory of the metal is detached from broader economic cooling.

With several upcoming catalysts on the horizon, including further updates on smelter status and maritime security protocols, the market is bracing for continued tension.

Ultimately, the longer-term positioning of aluminum suggests that current price levels are not merely a result of speculation but a reflection of a genuine and deep-seated shortage. For those prioritizing capital preservation, the focus must remain on the strategic direction of regional leaders in the Middle East.

While volatility is expected to continue in the short term, the fundamental structural deficit provides a strong foundation for sustained value. The ability of the global supply chain to adapt to these future expectations will determine the stability of the industrial sector as a whole throughout the next decade.