The global commodities landscape is navigating a period of intense price fluctuation as industrial metals retreat from recent multi-month highs. Copper, often viewed as a primary barometer for global economic health, has eased slightly from its most significant peak since early February.

This cooling period follows a weekend of heightened geopolitical instability in the Middle East, which has effectively stalled previous momentum toward a diplomatic resolution between major powers.

According to market analysts at Marbrisse, the current sensitivity in the metals market is a direct reflection of broader fears regarding a sustained energy shock.

As maritime security in the Strait of Hormuz remains compromised, the potential for a prolonged disruption to global trade routes is forcing institutional players to re-evaluate their longer-term positioning in base metals.

While demand signals remain mixed, the risk of a hawkish pivot by central bankers to combat energy-driven inflation remains a persistent concern for the manufacturing sector.

Geopolitical Deadlock And The Impact On Commodity Benchmarks

The primary catalyst for the recent shift in sentiment was the seizure of an Iranian-flagged vessel by naval forces, an event that has cast significant doubt on the future of scheduled peace talks.

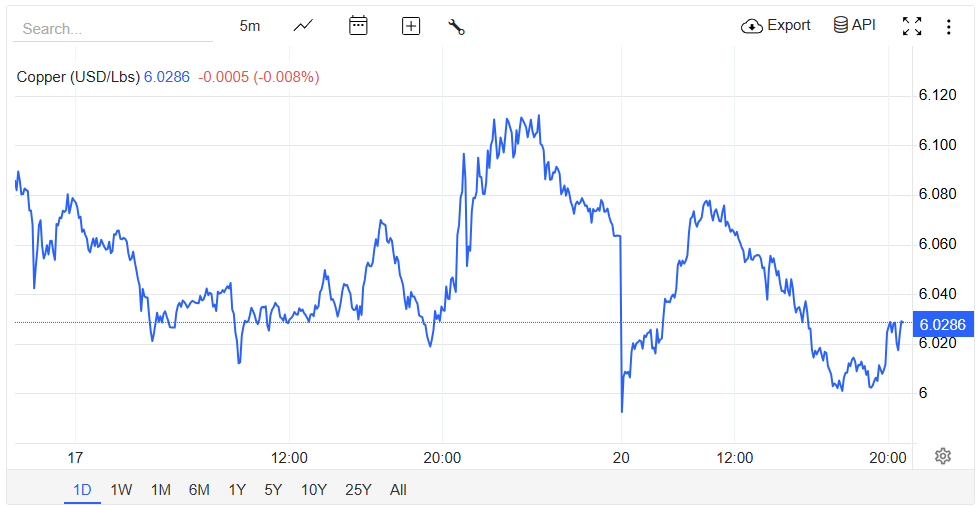

The conflict, now entering its eighth week, saw a dramatic escalation over the weekend, leading to a spike in crude oil prices that reversed much of the previous week’s downward trend. In London, copper was trading 1% lower at $13,217.50 a ton on the London Metal Exchange (LME) by late morning, following its third-highest close on record.

This volatility underscores the “whipsaw” nature of the current market, where signs of de-escalation are frequently met with renewed friction. The Foreign Ministry in Tehran has indicated that there are currently no plans to send diplomats to Pakistan for a second round of negotiations, citing the ongoing maritime blockade as a primary grievance.

For the metals market, the risk is that a closed strait will not only spike energy costs but also cripple the movement of raw materials and finished industrial products, leading to a stagnation in global manufacturing activity.

Chinese Demand Resilience Amidst Global Uncertainty

Despite the turbulence in the Middle East, copper prices are finding a level of support from robust industrial activity in East Asia. In China, inventories have been declining at a rapid pace, providing a necessary counterweight to the geopolitical risk premium.

Stockpiles monitored by the Shanghai Futures Exchange have seen a massive reduction of nearly 200,000 tons since the yearly peak recorded on March 13. This suggests that the peak consumption season is currently in full effect, with demand maintaining a high growth rate despite external shocks.

Aluminum Supply Chain Fragility And Smelter Disruptions

The aluminum market has followed a distinct trajectory compared to other base metals due to its heavy reliance on regional energy and infrastructure. Aluminum prices slipped further on Monday, following a 5% decline at the end of last week.

The conflict has directly forced smelter closures and significant production cuts across the Gulf region, which traditionally serves as a major global hub for the metal. Data from the International Aluminium Institute reveals that aluminum production in Gulf countries dropped by 6% to 15,963 tons a day during the month of March.

The ongoing closure of the Strait of Hormuz is viewed as a critical bottleneck, as it prevents producers from restocking essential raw materials like alumina and exporting finished products. This disruption is having a significant knock-on impact on global supply chains, extending as far as Australia, which serves as a primary supplier to the region.

The inability to move material has left large quantities of metal essentially stranded, leading to localized shortages and increased premiums for immediate delivery.

Industrial Resilience In An Evolving Economic Landscape

As the Tuesday ceasefire deadline approaches, the industrial sector is preparing for a range of possible outcomes. The strategic direction of the commodities market will depend heavily on whether a sustainable framework for maritime security can be established.

In the interim, metals like aluminum and copper will continue to be sensitive to upcoming catalysts involving both diplomatic announcements and domestic economic data from major consuming nations.

Under these evolving conditions, the focus for market participants remains on liquidity and capital preservation. While the Chinese market offers a localized narrative of growth, the broader global economy is still contending with the specter of a major energy-driven recession.

For institutional players, the financial trajectory of the metals sector will likely be defined by the balance between physical scarcity and the dampening effects of high interest rates.

In the absence of a clear breakthrough in Islamabad, the commodities market is set to remain in a state of high alert, navigating the thin line between a two-month high and a potential correction driven by global industrial cooling.