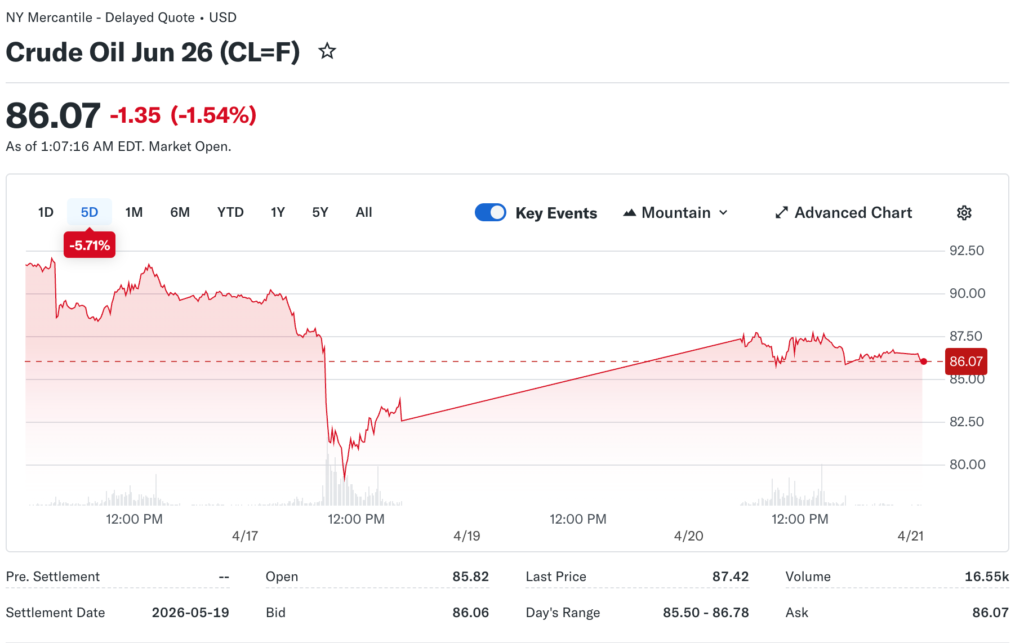

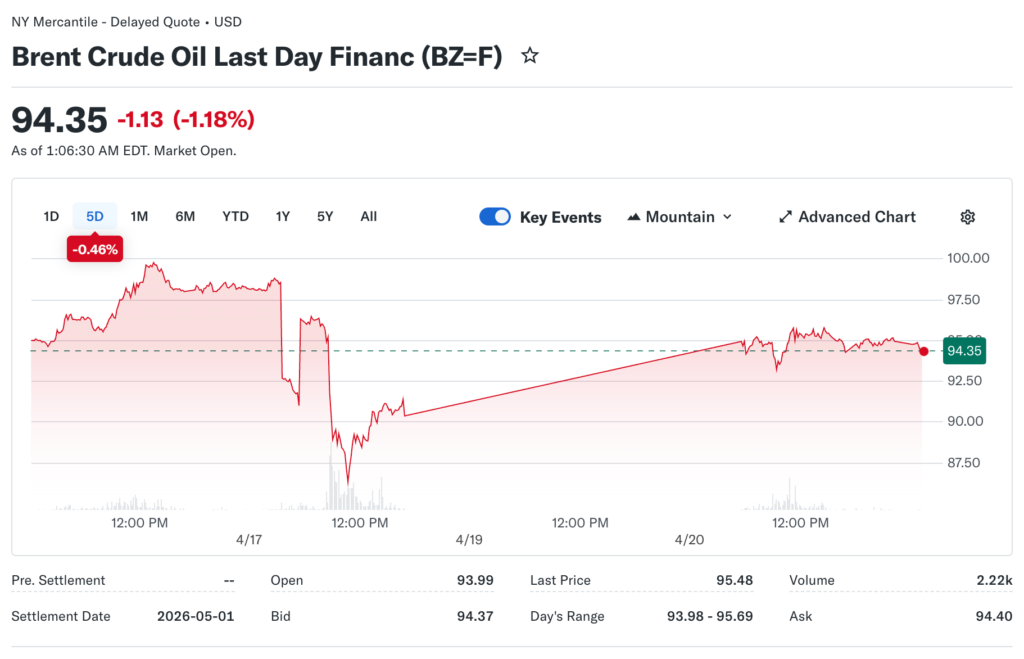

Crude oil prices whipsawed on Tuesday, trading in a narrow range near $88 per barrel. West Texas Intermediate futures fluctuated as geopolitical developments unfolded rapidly. Brent benchmark traded around $95, reflecting global supply concerns.

Senior broker from Nummvix analyzes how energy markets remained hostage to Middle East developments. Strait of Hormuz tensions are dominating price action despite ceasefire talks continuing. Supply disruptions are reaching historic proportions, with 9 million barrels daily shut-in.

The Price Action

WTI crude oscillated between $86 and $90 intraday, with volatility elevated. The benchmark rose 5% Monday before giving back gains. Traders whipsawed by conflicting headlines from the negotiation front.

Brent premium over WTI widened to $12 per barrel, historically wide. The shipping disruptions are disproportionately affecting the international benchmark. Asian buyers are particularly impacted by the Strait closure.

The futures curve indicates backwardation, indicating tight near-term supply. The prompt month trading substantial premium over deferred contracts. Market structure reflecting physical shortage despite demand destruction.

The Strait Situation

The Strait of Hormuz remained effectively closed to most commercial traffic. Iran is controlling the passage, requiring coordination with forces. Tanker movements have been reduced to a trickle from normal flows.

Crude exports from the Persian Gulf were effectively halted temporarily. Saudi Arabia, Kuwait, and the UAE are unable to ship production. Oil storage is filling rapidly at producing fields.

Production shut-ins reached 9.1 million barrels daily in April. The historic disruption exceeds previous supply shocks. OPEC is unable to offset the given geography constraints.

The Geopolitical Risk

Ceasefire talks scheduled in Pakistan are creating hope temporarily. Negotiators are meeting to discuss terms for ending the conflict. Market pricing is low on the probability of a breakthrough currently.

Duration uncertainty keeps the risk premium elevated significantly. The timeline for resolution completely unclear to participants. Energy security concerns are spreading among importing nations.

Strategic reserves being tapped to moderate price impact. The United States is releasing from the Strategic Petroleum Reserve. International Energy Agency coordinating member country actions.

The Demand Response

Global oil demand is contracting sharply due to the supply shock impact. Consumption declined 2.3 million barrels daily in April. Price rationing is destroying demand as budgets are strained.

Asian economies are particularly affected given their reliance on the Middle East. China and India are implementing conservation measures. Manufacturing activity is slowing due to energy costs.

Gasoline prices are averaging $4.50 per gallon nationally, punishing consumers. The retail prices are reaching levels triggering behavioral changes. Driving activity is declining as costs have become prohibitive.

The Refining Margins

Crack spreads surged to record levels, benefiting refiners. The gasoline and diesel margins extremely profitable. Product shortages are developing as crude supplies are disrupted.

Refinery utilization is declining with feedstock supply challenges. The runs are falling by 6 million barrels daily globally. Capacity is idled awaiting crude availability restoration.

Middle distillate prices are hitting all-time highs due to a shortage. The diesel and jet fuel are particularly tight. Industrial activity and aviation are bearing the brunt.

The Energy Stocks

Integrated oils outperform the broader market significantly. Chevron and ExxonMobil are benefiting from the price surge. Upstream earnings are exploding from the commodity tailwind.

Exploration and production companies are posting windfall profits. The shale producers are ramping up output where possible. Shareholder returns are increasing through dividends and buybacks.

Pipeline companies’ mixed performance given volume declines. Energy Transfer and Williams are exposed to throughput. Fee-based models are partially insulated from prices.

The Service Sector

Oilfield services stocks are rallying on activity expectations. Halliburton and Schlumberger are positioned for growth. International markets particularly attractive for expansion.

Offshore drillers are benefiting from renewed interest. The deepwater assets commanding premium day rates. Contract renewals at substantially higher terms.

The offshore construction backlog is building from projects sanctioned. The subsea equipment is in strong demand for development. Energy security driving investment decisions.

The Alternative Energy

Renewable stocks are underperforming despite the oil surge, surprisingly. The solar and wind companies are not benefiting. Valuations are already elevated, limiting upside perhaps.

Electric vehicle adoption pace unchanged by gasoline prices. Tesla and its competitors are maintaining delivery schedules. Long-term transition narrative unchanged fundamentally.

Nuclear renaissance gaining momentum from crisis. The uranium prices are rising on renewed interest. Small modular reactors receiving regulatory attention.

The Natural Gas

Natural gas prices are rising in sympathy with crude oil. The Henry Hub benchmark is around $3.50 per mmBtu. LNG exports are running near capacity, substituting for supply.

European prices are spiking from the Middle East LNG disruption. The gas flows through the Strait were also curtailed. Energy crisis concerns resurfacing in Europe.

Storage levels adequate for now, moderating concerns. However, the injection season is approaching, requiring builds. The winter 2026-27 outlook is uncertain given supplies.

The Investment Strategy

Energy sector weighting increased among portfolio managers. The commodity exposure provides an inflation hedge. Valuation multiples compressed despite earnings surge.

Integrated oils preferred over pure exploration companies. The diversification across the value chain is attractive. Dividend yields around 4% supporting valuations.

Caution is warranted given the geopolitical dependency entirely. The downside of a resolution substantial and sudden. Position sizing is accordingly recommended by strategists.