Semiconductor stocks surged on Tuesday, leading technology sector gains. AI chip demand remained insatiable, driving revenue growth. Taiwan Semiconductor reported 32% quarterly revenue increase, stunning investors.

Lead financial analyst from Nummvix examines how artificial intelligence applications are fueling unprecedented chip demand. Data center buildouts are accelerating globally, requiring massive amounts of silicon. Supply constraints persist despite capacity additions, limiting availability.

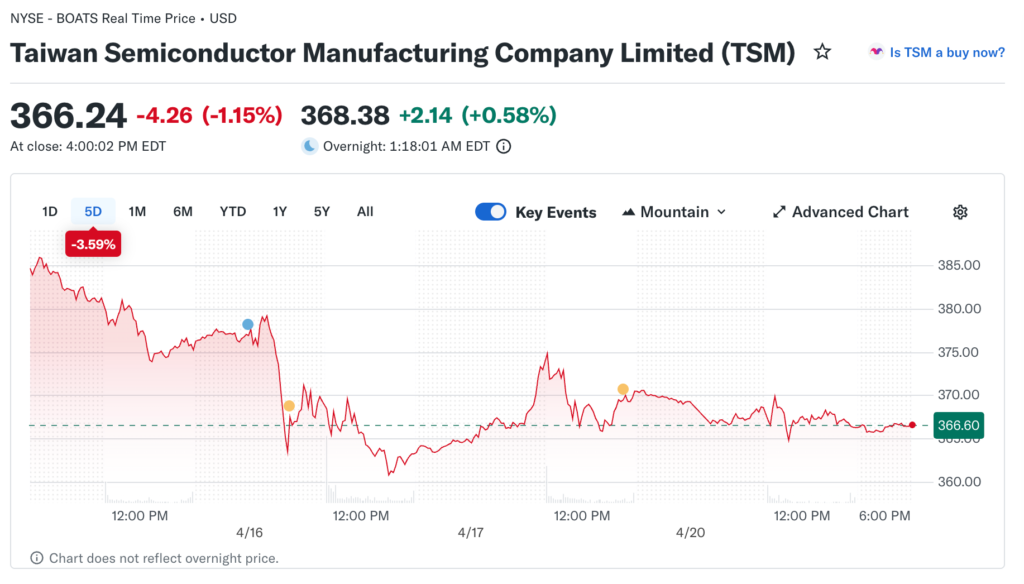

The TSMC Dominance

Taiwan Semiconductor Manufacturing reported first-quarter results exceeding expectations. The world’s largest foundry posted revenue growth 32% year-over-year. Earnings surged 40% from operating leverage materializing.

Advanced nodes driving growth with 3-nanometer production ramping. The cutting-edge process technology commanded premium pricing. Capacity is fully booked throughout the year with waiting lists.

Customers, including NVIDIA, Apple, and AMD, are competing for allocation. The fabless chipmakers are dependent on TSMC manufacturing. Geopolitical concerns about Taiwan’s concentration rising.

The NVIDIA Phenomenon

NVIDIA shares climbed 2%, maintaining its leadership position. The GPU giant is trading at $187 per share. Market capitalization exceeding $4 trillion, making it the world’s largest.

Data center revenue growth is exceeding 100% annually and is sustained. The Blackwell platform launched successfully to strong demand. Enterprise adoption of AI is accelerating across industries.

Gross margins are around 75%, demonstrating pricing power. The vertically integrated approach commands premiums. The software ecosystem is creating a competitive moat, deepening.

The Broadcom Surge

Broadcom custom AI chips are gaining market share rapidly. The ASIC approach appeals to hyperscalers seeking optimization. Google and Meta are designing proprietary solutions.

VMware acquisition integration progressing ahead of schedule. The virtualization software leader complements hardware. Data center software revenue is diversifying the business mix.

Networking chips are benefiting from the AI infrastructure buildout. The switches and routers connect GPU clusters. Vertical integration across the stack creates value.

The Memory Boom

Micron Technology’s high-bandwidth memory sales are exploding. The HBM products essential for AI applications. Capacity constraints are limiting supply despite expansions.

DRAM prices are rising 40% from cycle lows. The memory market is recovering from oversupply. Pricing power is finally returning to manufacturers.

NAND flash is also strengthening due to data center demand. The storage requirements for AI training enormous. Capital expenditures are increasing to meet needs.

The Equipment Makers

ASML’s photolithography monopoly is strengthening further. The extreme ultraviolet lithography machines irreplaceable. Delivery times are extending to 18 months out.

Lam Research and KLA are benefiting from capacity additions. The demand for manufacturing equipment is surging globally. China’s buildout, despite restrictions, is contributing.

Applied Materials is posting record backlog levels. The diverse product portfolio is capturing growth. Service revenues provide recurring income streams.

The Design Tools

Cadence and Synopsys electronic design automation are thriving. The chip complexity requires sophisticated software. AI-powered design tools improving productivity significantly.

Licensing revenues recurring nature valued by investors. The mission-critical nature ensures retention. Pricing increases are passing through successfully.

Cloud-based tools are gaining adoption among customers. The scalability and collaboration features are appealing. Subscription models are improving cash flow visibility.

The Foundry Economics

Manufacturing capacity additions cost billions per facility. The Arizona and Germany fabs are under construction. Government subsidies partially offset investments.

Leading-edge nodes require extreme precision and cost. The 3-nanometer and below is technically challenging. Yield improvements are taking time to optimize.

Mature nodes also tight with automotive demand. The 28-nanometer capacity is constrained globally. Diversification across technologies prudent strategy.

The China Factor

Semiconductor restrictions limiting U.S. exports to China. The advanced chips and equipment were embargoed. National security concerns driving policy decisions.

Chinese chipmakers are investing heavily in self-sufficiency. SMIC is advancing despite technology constraints. Government funding supports the domestic industry.

Geopolitical tensions are creating supply chain bifurcation. The U.S. and China are developing parallel ecosystems. Redundancy costs are increasing for everyone.

The Automotive Chips

Car semiconductors are recovering from a shortage period. The electric vehicles require more content. Advanced driver assistance systems silicon-intensive.

NXP and Infineon are benefiting from electrification. The power management chips essential for EVs. Automotive design wins multi-year revenue.

Inventory corrections are behind the industry, finally. The restocking cycle begins for components. Pricing stabilizing after the volatility period.

The AMD Challenge

Advanced Micro Devices is gaining data center share. The MI300 AI accelerators are competitive with NVIDIA. Price-performance advantage appeals to customers.

The CPU business is recovering from Intel’s weakness. The server processors market share gains continue. Epyc platform adoption is accelerating among hyperscalers.

Gaming graphics cards are facing competition from NVIDIA. The Radeon products are struggling against the GeForce. Console chips provide a stable revenue base.

The Sector Outlook

The semiconductor industry is expected to finally surpass $1 trillion in sales in 2026. The milestone reflects decades of growth. AI applications are pushing over the threshold.

Consolidation is likely to continue given scale requirements. The M&A activity is picking up selectively. Regulatory scrutiny limits some combinations.

Long-term growth trajectory intact despite cyclicality. The digital transformation requires more silicon. AI and edge computing are driving the next wave.