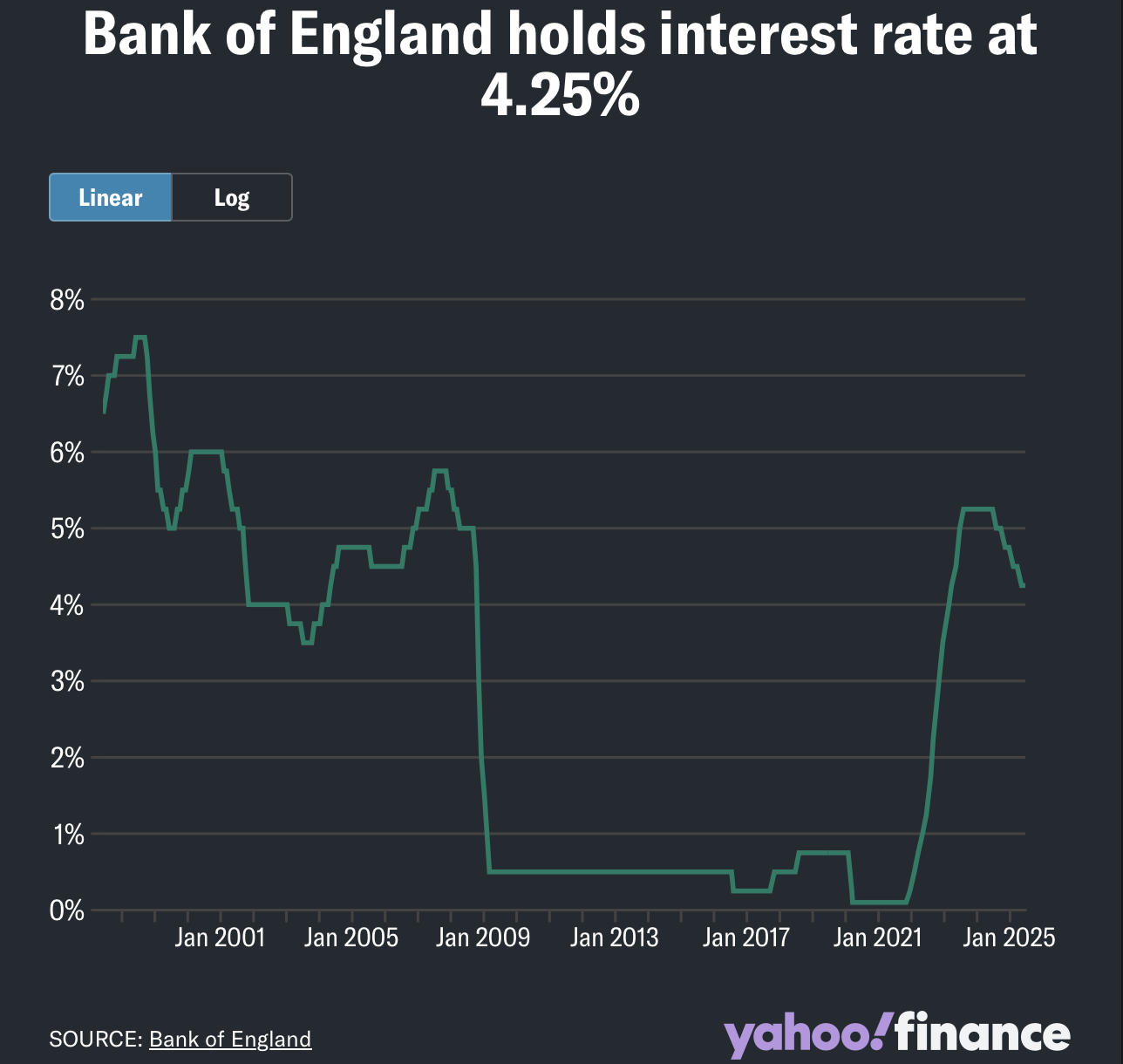

In a time of geopolitical strain, global tariff shifts, and an unpredictable energy market, the Bank of England (BoE) is walking a tightrope between stimulating the economy and keeping inflation under control. This week, the central bank decided to hold interest rates steady at 4.25%, resisting further cuts for now, even as expectations of relief grow louder across the financial landscape.

This decision reflects more than just economic forecasting; it’s a reflection of how unpredictable global dynamics, from Middle East conflicts to US trade tariffs, continue to shape domestic financial policy. To unpack what this means for everyday borrowers, savers, and investors, a financial strategist at Tandexo unpacks the delicate balancing act the BoE is navigating.

Why the BoE Froze the Rate at 4.25%

The BoE’s latest Monetary Policy Committee (MPC) vote landed at 6–3 in favor of holding rates at 4.25%, with three members calling for a 0.25 percentage point cut. This came after a prior rate reduction in May, continuing a pattern of easing seen every other meeting since last August, when rates peaked at 5.25%.

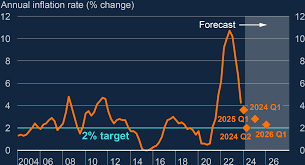

Despite this trend, the MPC ultimately decided to hold off this round, driven by one key concern: inflation remains above the BoE’s 2% target, registering 3.4% in May. Persistent services inflation and wage growth are viewed as barriers to cutting rates more aggressively.

The Middle East and Global Energy Pressures

The situation has been further complicated by rising oil prices, sparked by escalating tensions in the Middle East. Within days, energy prices rose 8.5%, adding to inflationary pressure and shaking confidence in a stable rate-cutting path.

This has prompted the BoE to tread carefully, stating that “energy prices have risen owing to an escalation of the conflict in the Middle East” and warning of heightened geopolitical unpredictability.

Investors Still Expect a Cut: Just Not Yet

Market sentiment still leans toward further easing. Traders have priced in an 84% probability of a rate cut to 4% at the BoE’s next meeting, up from 77% earlier in the week. But that expectation hinges on inflation continuing to cool and economic conditions becoming more favorable.

Some analysts suggest a more moderate trajectory. The BoE’s forecast for inflation anticipates it remaining broadly flat for the rest of 2025, before gradually falling toward the target in 2026.

How Tariffs and Global Trade Disruption Are Complicating Things

The inflation narrative doesn’t exist in a vacuum. Economic uncertainty from new US-imposed tariffs is still playing out, with many analysts pointing to trade tensions as a growing concern for the UK.

With the 90-day pause on reciprocal tariffs nearing its end, the fallout is expected to hit European exporters hardest, especially since Europe remains the UK’s largest trading partner. The BoE acknowledged these external threats, noting “two-sided risks to inflation”, one being global cost pressures, the other being weaker domestic demand.

Labour Market Softening, But Not Enough

One silver lining for those hoping for lower rates is the cooling UK labour market. The BoE noted that the job market has “continued to loosen,” which should, in theory, reduce pressure on wages and help bring inflation down.

However, without “clear signs in the hard data,” the MPC remains cautious. The committee made it clear that only strong, consistent evidence of declining service prices and wage growth would justify faster cuts.

Homebuyers Caught in the Middle

The central bank’s decision has ripple effects for millions of UK consumers, especially homebuyers and mortgage holders. Although Zoopla reported healthy housing activity in May, fixed mortgage rates are likely to remain volatile.

According to one strategist, the UK economy’s “neutral interest rate” likely lies around 3%, but markets only expect the base rate to reach 3.5% by April 2026. This indicates that any return to more affordable borrowing conditions will be slow and gradual.

For now, mortgage rates are hovering between the upper 3% and lower 4% ranges, with lenders closely watching inflation and BoE signals. Those looking to borrow or refinance may face limited windows of opportunity.

A Broader Global Contrast

While the BoE remains cautious, some of its peers are taking more decisive action. In the past week alone:

- The Swiss National Bank cut its rate to 0%, citing a strong franc and subdued inflation.

- Norway’s central bank surprised markets with its first rate cut in five years, lowering borrowing costs from 4.5% to 4.25%.

- In contrast, the US Federal Reserve held its rate steady, with no change to its expected two-rate-cut outlook for the year.

This divergence illustrates just how fragmented global monetary policy has become, each central bank grappling with a unique blend of inflation, trade shifts, and political risk.

Conclusion: Holding the Line in Uncertain Times

The Bank of England’s decision to hold interest rates at 4.25% reflects the difficult position policymakers face: navigating between stubborn inflation, a cooling labour market, and unpredictable external shocks from trade and geopolitical conflict.

While a future rate cut remains likely, possibly as early as autumn, it will only come once inflation trends become clearer, and the global economic backdrop stabilizes.

In short, the Bank isn’t done cutting, but it’s not ready to move faster just yet. As inflation simmers and international risks swirl, caution, not urgency, remains the Bank’s guiding principle for now.