After months of heightened tension between the U.S. and China, a 90-day tariff truce has brought some calm to volatile commodity markets, particularly oil and iron ore. While the energy sector grapples with shifting U.S. policy preferences and oversupply, the metals market is cautiously optimistic on the back of trade relief and potential stimulus in China.

This reset has significant implications across industries, from crude production to steel output. To better understand the economic undercurrents driving recent price action, a commodities strategist from Horizon28, Thomas de Waal offers a deeper analysis of the intertwined forces behind this fragile rebound.

Crude Oil Sentiment: A Presidential Price Preference

image from vantagemarkets.com

Over the past several years, U.S. energy policy has been closely linked to domestic production goals and oil affordability. According to recent analysis by Goldman Sachs, the current U.S. administration appears to favor West Texas Intermediate (WTI) oil prices between $40 and $50 per barrel, based on an extensive review of nearly 900 social media posts by America’s president.

- When WTI exceeds $50, the messaging has often included calls for price reductions, usually linked to inflation control or gasoline affordability.

- Conversely, when prices fall below $30, posts have historically shifted toward supporting higher oil prices, mainly to bolster domestic energy producers.

As of the most recent data, WTI was trading slightly above $63 a barrel, despite shedding 12% year-to-date due to tariff fallout and a faster-than-expected supply increase by OPEC+. However, oil prices have rebounded from earlier lows following the U.S.-China tariff reprieve, suggesting a short-term floor may be in place.

Goldman’s broader view points toward lower oil prices in 2025–2026, though recent developments like the trade truce could present upside risks, particularly if global demand stabilizes.

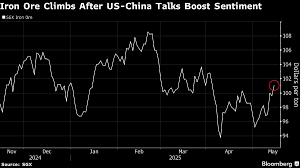

Trade Truce Fuels a Metal Market Rebound

While oil markets contend with geopolitical balancing, iron ore—a vital input for steelmaking—has also shown signs of life. Prices climbed nearly 2% to a six-week high, with Singapore futures reaching $101 per ton and Dalian exchange contracts rising over 2.5%.

This modest rally was sparked by the same U.S.-China trade truce, which prompted renewed hopes for expanded industrial activity and fewer export restrictions. According to a joint statement, “substantial progress” has been made in negotiations, and both sides are working toward longer-term solutions.

But optimism in the metals market remains guarded. The ferrous complex, which includes steel and iron ore, has been under pressure due to:

- Slowing global growth

- Weaker steel demand

- Production cuts planned in China for environmental reasons

Even if trade relations continue to improve, the sector is not immune to structural headwinds.

China’s Role: Stabilizer or Structural Drag?

Much of the metals market’s direction hinges on China’s policy decisions. Analysts at Bloomberg Intelligence note that new stimulus efforts, particularly in infrastructure and housing, could lift steel demand by 0.5% over the next two years—a modest recovery compared to earlier consensus estimates of a 3% decline.

Key factors include:

- A stabilizing property market after four years of stagnation

- Fiscal support for the industrial and construction sectors

- A shift toward more targeted stimulus, rather than broad credit easing

However, China’s industrialization has entered a mature phase, meaning large-scale expansions in steel and iron demand are unlikely. Analysts caution that any recovery may be temporary, more cyclical than structural.

Commodities Caught Between Politics and Demand

The intersection of commodity markets and political rhetoric is becoming more pronounced. Oil, for instance, remains a highly politicized asset, with prices often responding not just to supply and demand fundamentals, but also to:

- Public statements from U.S. leadership

- Sanctions and foreign policy shifts

- OPEC+ coordination and breakdowns

Similarly, the metals market is shaped not just by construction or automotive demand, but also by:

- Tariff regimes

- Subsidy announcements

- Environmental regulations in both China and the West

The trade truce, while providing near-term relief, does little to erase these deeper forces.

Near-Term Outlook: Recovery or Pause?

Looking ahead, several trends are emerging across the energy and metals space:

Oil Market Signals

- WTI remains rangebound, with downward pressure from OPEC+ supply but support from U.S.-China trade de-escalation.

- Price sensitivity from U.S. policymakers could curb upside potential above $60–$65 per barrel.

- Longer-term expectations suggest a drift lower, unless new supply disruptions or demand spikes materialize.

Iron Ore and Steel Sentiment

- Iron ore may continue to find support around $100/ton, barring major downgrades to China’s demand outlook.

- Stimulus measures and trade detente offer a temporary lifeline, though analysts still flag structural risks in China’s steel-intensive sectors.

- The market could remain volatile, reflecting the clash between short-term optimism and longer-term transition.

Conclusion: Temporary Relief, Persistent Questions

The recent uptick in oil and iron ore prices underscores how global commodity markets remain deeply intertwined with policy signals and macroeconomic narratives. The U.S.-China truce has brought momentary clarity, allowing both crude oil and industrial metals to stabilize after a turbulent stretch.

Yet, under the surface, deeper uncertainties persist. From the U.S. administration’s active influence on energy pricing to China’s cautious approach to stimulus, the road ahead remains uneven.

For investors and analysts alike, the key will be separating short-term market responses from long-term structural change—and staying alert in a world where barrels and steel speak louder than words.