Bitmine Immersion Technologies disclosed the largest single-week Ethereum purchase of 2026 this week, bringing its total holdings to 4.535 million ETH, a position equivalent to 3.76% of Ethereum’s entire circulating supply. The brand’s senior financial analyst at Nummixo stresses that while the scale of this accumulation reflects genuine conviction in the Ethereum thesis, the concentration of risk embedded in the strategy deserves careful and honest evaluation from anyone considering exposure to this stock.

The Position Has Reached an Unusual Scale

Holding 3.76% of the total Ethereum supply places Bitmine in a category occupied by very few entities anywhere in the world. This is not a diversified digital asset treasury. It is a concentrated, single-asset accumulation strategy being executed with growing intensity, and the company is continuing to add to it ahead of what management describes as a significant product launch.

The staking operation adds another layer to the picture. Bitmine now has more than 3 million ETH staked within the Ethereum network, generating recurring income through validation rewards tied directly to on-chain activity levels. At this scale, the staking revenue stream is substantial. Total reported assets across crypto holdings, cash, and other investments stand at $10.3 billion, giving the company a balance sheet that is large in absolute terms relative to most crypto-exposed equities.

MAVAN Is the Strategic Bet Behind the Buying

The accelerated pace of Ethereum acquisition is not happening in isolation. Management has been deliberate about connecting the accumulation strategy to the upcoming launch of the MAVAN enterprise staking network, a platform designed to provide institutional-grade staking services to external clients rather than simply generating returns from Bitmine’s own holdings.

If MAVAN attracts meaningful enterprise adoption after launch, the revenue model shifts from a balance-sheet-driven staking operation to a fee-based platform business serving other large ETH holders. That transition would represent a significant maturation of the business model, reducing dependency on Ethereum price appreciation as the primary driver of financial performance. The market’s reaction to MAVAN’s early traction, or lack of it, will likely be one of the most important share price catalysts for BMNR through the rest of 2026.

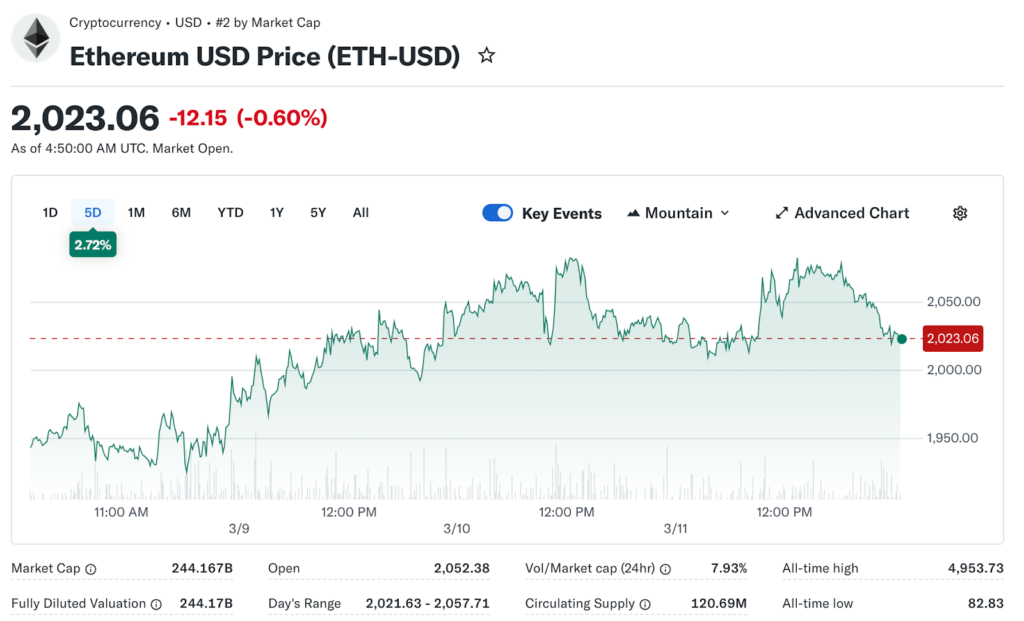

The Stock’s Performance Reflects the Volatility

The price history of BMNR shares captures the inherent tension in this business model. The stock has gained 172.8% over the past year, reflecting the substantial value creation the Ethereum accumulation strategy has delivered during that period. At the same time, shares are down 33.5% year to date in 2026, reflecting how quickly sentiment can shift when a single asset with known volatility characteristics moves against a concentrated holder.

Both of those data points are accurate simultaneously, and together they describe the experience of owning a company whose fortunes are this closely tied to a single digital asset. The upside can be extraordinary. The drawdowns can be severe. And the transition between the two can happen faster than most equity investors are accustomed to managing.

Concentration Risk Has Multiple Dimensions

The risks attached to Bitmine’s strategy extend beyond simple price exposure to Ethereum. Protocol risk is a genuine consideration. Ethereum has undergone significant technical changes in recent years, and future network upgrades could alter the economics of staking in ways that are difficult to model from the current vantage point. Changes to validator reward structures, alterations to the staking mechanism, or shifts in the network’s fee market could each affect the income Bitmine generates from its staked position.

Regulatory risk has grown more relevant as institutional crypto activity has attracted greater attention from financial regulators globally. Frameworks governing staking activities, the tax treatment of staking rewards, and capital requirements for entities holding large positions in digital assets are all areas where regulatory clarity remains incomplete. A material change in any of these areas could affect Bitmine’s operations with limited advance notice.

Dilution risk is a third factor that analysts have specifically flagged. Bitmine has previously issued equity to fund its Ethereum purchases, and the ongoing buildout of the MAVAN platform will likely require additional capital. Shareholders who do not participate in future equity raises face ownership dilution, and the company’s history in this regard is something investors should factor into their total return calculations rather than focusing solely on the asset appreciation story.

Three Things Worth Tracking Closely

For investors already holding BMNR or considering a position, three developments will define the investment narrative through the remainder of 2026. The MAVAN launch timeline and initial enterprise customer numbers will be the clearest signal of whether the platform can generate fee-based revenue at a meaningful scale.

Updates to the total ETH position and the proportion actively staked will reflect both management’s ongoing conviction and the evolution of the income profile. Any new capital raises or additional moonshot investments will reveal how management is balancing growth ambitions against balance sheet discipline and the dilution history that existing shareholders are already carrying.