Government savings fund steps in as banks tighten lending amid weak housing demand

China’s housing market is grappling with weakening sales and a slowing economy. In response, the government is turning to its 10.9 trillion yuan ($1.5 trillion) housing provident fund to offer homebuyers an alternative to bank mortgages.

This move is designed to reduce the mortgage burden and provide much-needed support to homebuyers in these challenging times. An expert from Rineplex highlights the growing role of this fund as local governments adjust policies to unlock its potential.

The Shift Toward Housing Provident Fund Support

China’s housing sector faces persistent issues, including oversupply, reduced buyer demand, and concerns about the financial health of developers. With commercial banks becoming more cautious in their lending practices due to rising bad debts and shrinking profits, the housing provident fund has emerged as a crucial alternative.

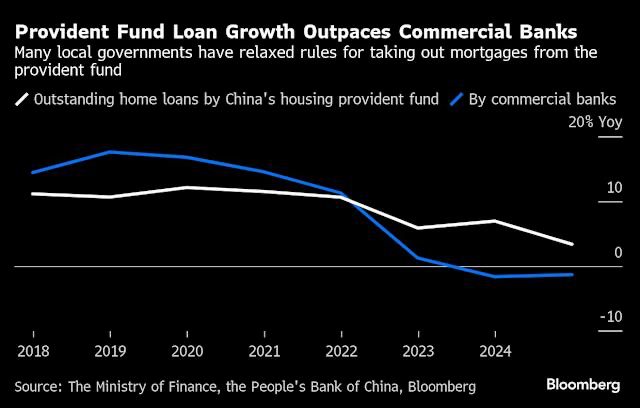

Housing provident fund loans now total 8.1 trillion yuan, surpassing the outstanding mortgages of traditional banks.

Chen Wenjing, a researcher from China Index Holdings, explains that the housing provident fund has become a primary tool in the government’s efforts to support the housing market. This often-overlooked savings program allows employers and employees to contribute monthly, creating a pool of funds that can be used for home purchases, often at lower interest rates than traditional bank loans.

Key Features of the Housing Provident Fund

The provident fund system is not new. It was adopted from Singapore more than three decades ago and requires both employers and employees to contribute to a shared savings pool. The funds accumulated are then offered as mortgages, usually at favorable terms.

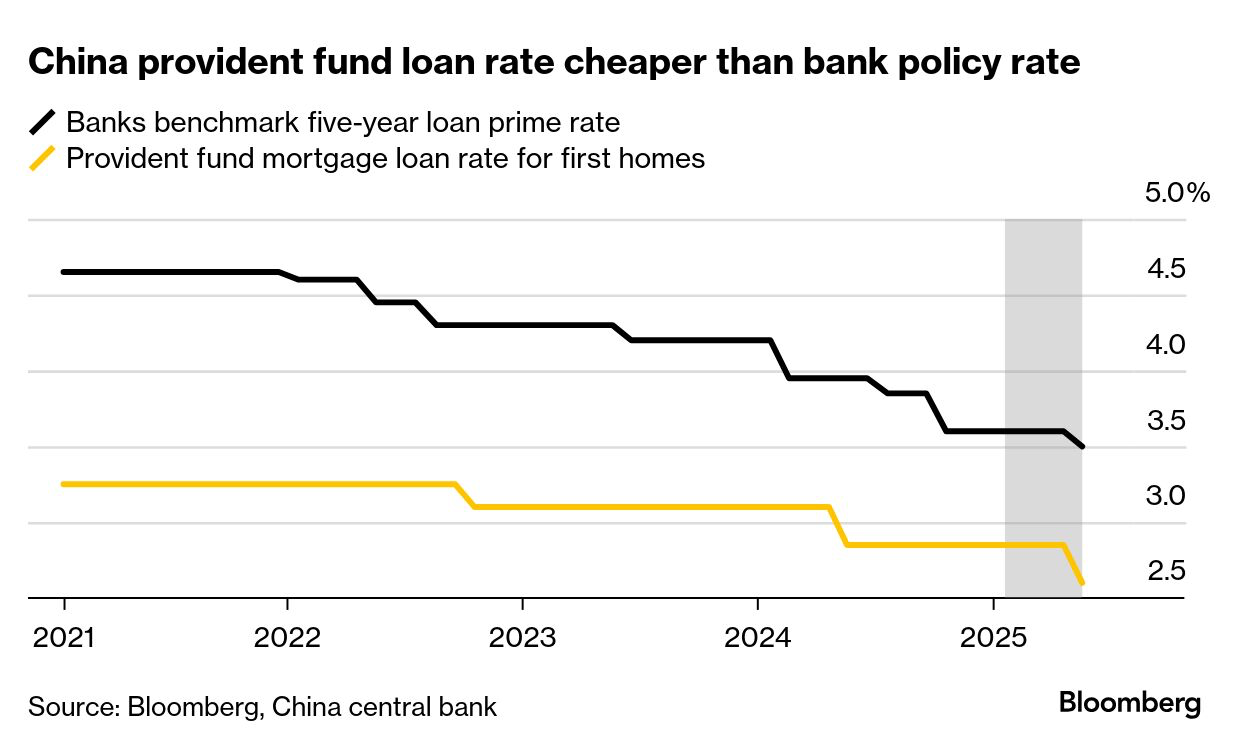

Unlike banks, which have been tightening lending amid broader financial pressures, the provident fund continues to offer accessible mortgage loans even as the banking sector pulls back.

In 2024, the outstanding loans issued through the provident fund increased by 3.4%, while bank loans dipped by 1.3%. This shift highlights the growing importance of the fund as a reliable alternative for financing home purchases.

The system benefits from a large base of contributors, nearly 180 million people, and continues to offer more aggressive lending policies compared to the cautious approach of banks.

A Ray of Hope for Homebuyers in a Tight Market

The central government has started easing the rules surrounding the provident fund, allowing more flexibility in how it can be used for home purchases. At least 50 municipalities have relaxed conditions, increasing loan limits and enabling down payments to be made from the savings pool.

In Shenzhen, one of China’s least affordable cities, new measures allow residents to withdraw provident fund deposits to help with down payments. Similarly, Beijing saw the fund cover 33% of residential mortgages in 2024, up from 29.4% in 2020.

These changes reflect the government’s intent to unlock more funds for homebuyers and alleviate the financial burden created by declining residential sales. However, while these measures offer some relief, they may not be enough to spark a full recovery in the housing market.

Can the Provident Fund Turn the Tide?

Despite the vital support it provides, analysts remain uncertain about the housing provident fund’s ability to resolve the fundamental issues facing China’s housing market, primarily, weak demand.

Residential sales continued to decline in May, with major developers like Country Garden Holdings reporting a 28% drop in transactions. Bloomberg Intelligence analysts Kristy Hung and Monica Si point out that although the provident fund provides relief to homebuyers, it does not address the root cause of the market’s problems, lack of demand.

Interest rates on mortgages issued through the provident fund have been reduced by 0.9 percentage points in recent months, making them more affordable than bank loans. However, Liu Jieqi, a Hong Kong-based property analyst at UOB Kay Hian, believes that while this rate cut might lower borrowing costs by about 3%, it is unlikely to trigger a significant boost in home sales.

The Long-Term Outlook: Can the Fund Sustain Growth?

The housing provident fund remains a vital tool for the Chinese government in its efforts to stabilize the housing market. President Xi Jinping has emphasized the need for continued policy support to bolster the sector amid both external and internal economic challenges. However, the success of these efforts will depend on the effective implementation of measures and the broader economic recovery.

In conclusion, while the housing provident fund offers a valuable alternative to traditional bank mortgages, it does not serve as a one-size-fits-all solution to the deeper challenges plaguing China’s housing market.

As the market continues to face headwinds, it will be crucial to monitor how policymakers adjust their strategies and whether these efforts can shift the broader sentiment in the housing sector.

Closing Thoughts: More Than Just Financial Relief

The decision to leverage China’s $1.5 trillion provident fund underscores the government’s resolve to support the housing market. However, whether these measures will bring about a full recovery or simply offer temporary relief remains uncertain.

Investors and homebuyers should stay vigilant, keeping a close watch on how the fund’s policies evolve and whether broader economic conditions can restore confidence in the sector in the coming months.