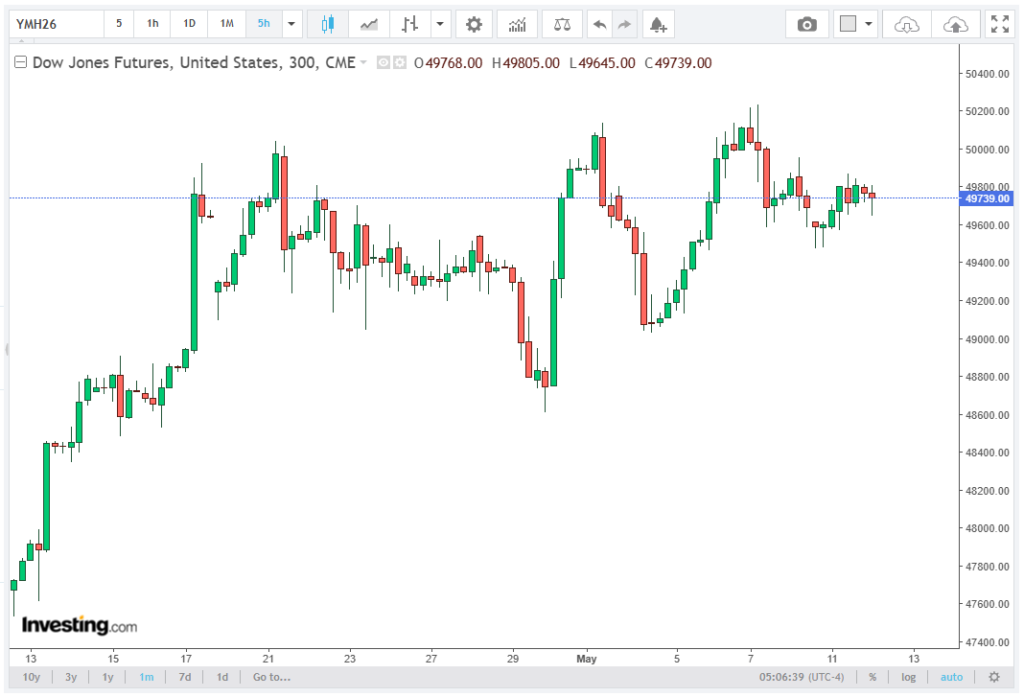

Dow Jones futures are holding steady around 49,800 during European trading hours on Tuesday, signaling a cautious start to the week as investors await the release of the US Consumer Price Index (CPI) for April.

Heightened geopolitical tensions between the United States and Iran have increased risk aversion, offsetting optimism from strong tech sector performance. The team at Nummixo presents a complete analysis of this issue in their recent publication.

Meanwhile, S&P 500 futures slipped 0.35% to 7,410, and Nasdaq 100 futures fell 0.77% to roughly 29,200. Traders are monitoring April’s inflation data, as analysts expect headline CPI to rise 0.4% month-over-month and 3.7% year-over-year, providing crucial insight into inflationary pressures and the potential direction of Federal Reserve (Fed) interest rate policy.

Renewed US-Iran Tensions Weigh on Market Sentiment

US stock futures are under pressure amid escalating US-Iran tensions, with markets reacting to geopolitical uncertainty. CNN reported that the US President expressed increasing frustration with the progress of ongoing negotiations to resolve hostilities in the region.

According to White House aides, the administration is now considering a resumption of military action more seriously than in previous weeks, raising market volatility. The CBOE Volatility Index (VIX) briefly spiked to 21.8, up from 19.5 at the prior close, reflecting heightened investor risk aversion.

Further compounding tensions, Iranian Parliament Speaker Mohammad Bagher Ghalibaf warned via Reuters that Iran’s military is prepared to retaliate against any future strikes, placing the fragile ceasefire under strain. Analysts note that any escalation could disrupt oil supply, potentially pushing Brent crude above $86 per barrel, impacting energy-heavy indices such as the Dow Jones Industrial Average (DJIA).

US Stock Futures and Inflation Watch

Investors are focused on April’s CPI report, which will shed light on the inflationary trajectory of the US economy. Expectations for core CPI, which excludes volatile food and energy prices, are around 0.3% month-over-month, with year-over-year growth near 3.3%. These figures will influence Fed policy guidance on potential interest rate adjustments, particularly amid concerns about geopolitical risk premiums.

Despite Dow Jones futures holding steady, the S&P 500 and Nasdaq 100 futures have dipped slightly, signaling a market teetering between optimism and caution. Analysts emphasize that any surprise inflation data could trigger a repricing of risk assets, especially in growth-sensitive sectors like technology and semiconductors.

Wall Street Gains Fueled by AI Optimism

Wall Street closed higher on Monday, with the Dow Jones up 0.19% to 49,710, the S&P 500 up 0.19% to 7,436, and the Nasdaq 100 adding 0.1% to 29,430, reaching fresh record highs. Gains were primarily led by chipmakers, which rallied on AI-driven demand expectations. NVIDIA (NVDA) surged +4.2%, AMD +3.7%, and Intel +2.1%, reflecting investor confidence in semiconductor growth driven by artificial intelligence applications.

In addition to tech, energy, materials, and industrial sectors contributed to Monday’s rally. ExxonMobil (XOM) gained +1.5%, Caterpillar (CAT) +1.2%, and Freeport-McMoRan (FCX) +2.0%, supporting broader market momentum despite rising geopolitical risk.

Key Market Drivers This Week

Traders are eyeing several critical catalysts in the coming days. April CPI remains central, with expectations for a moderate acceleration in inflation. US-Iran tensions and the risk of potential military escalation could amplify risk-off sentiment, contributing to further equity market volatility and cautious positioning in both stocks and commodities.

Additionally, markets will closely monitor the US President’s meeting with Chinese President Xi Jinping, covering trade policies, AI regulation, and global energy security. Outcomes from this discussion could have meaningful implications for global supply chains, equity indices, and currency markets, particularly USD/CNY, which is currently trading near 7.25, as well as broader emerging market flows.

Outlook and Investor Considerations

In the current environment, investors face a delicate balance between opportunity and caution. AI-driven technology stocks and sector rotation present upside potential, yet heightened geopolitical risk and pending inflation data necessitate robust risk management.

The flat performance of Dow Jones futures indicates a market in wait-and-see mode, with participants weighing the economic consequences of US-Iran tensions alongside inflation expectations. Analysts suggest that sustained market gains will depend on both a resolution of regional conflicts and supportive economic data, particularly core CPI readings and retail sales figures.

As traders anticipate CPI figures and track geopolitical developments, Dow Jones futures remain a barometer of market caution, while optimism in AI-driven technology stocks continues to propel the S&P 500 and Nasdaq 100 to record highs.

Investors should maintain balanced exposure across growth and defensive sectors, while closely monitoring risk indicators such as VIX and bond yields, which currently stand at 10-year Treasury yield: 4.12%.