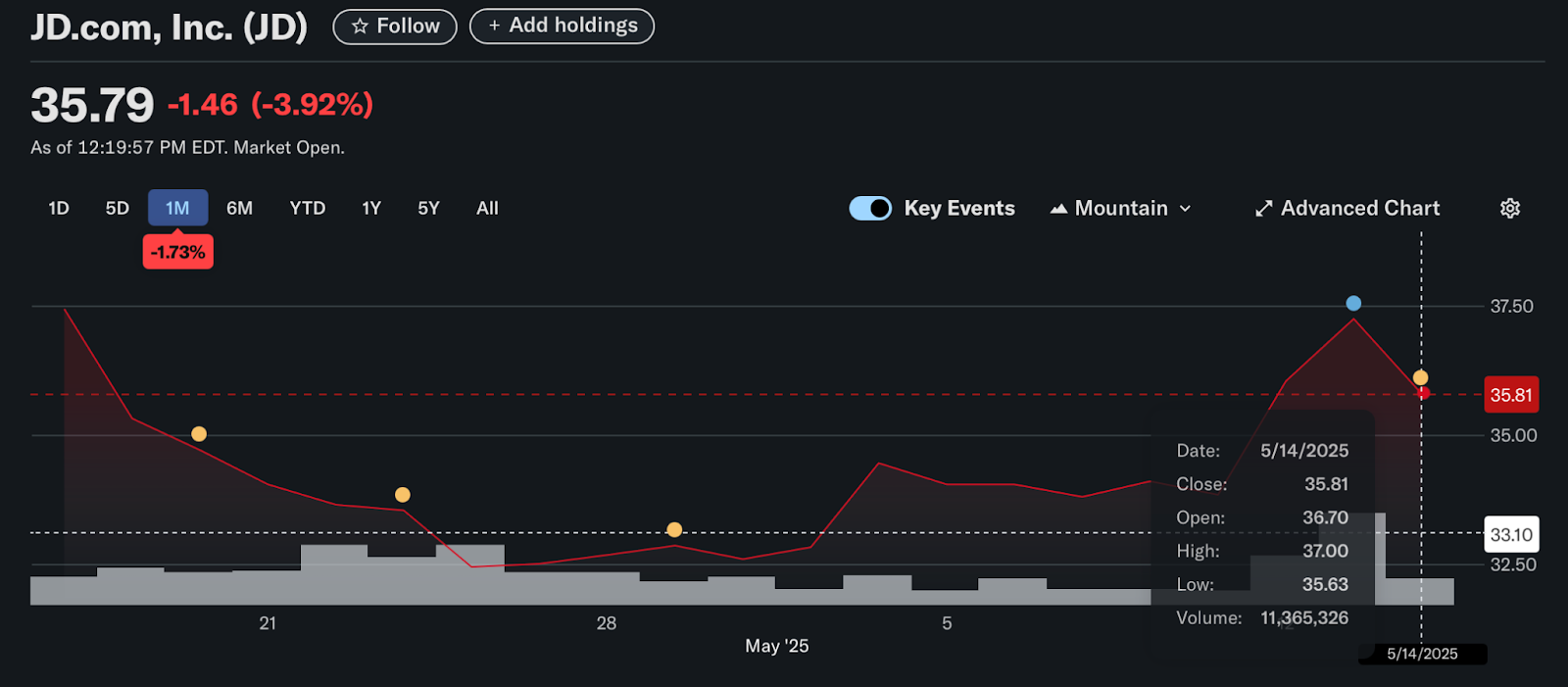

JD.com has posted its fastest revenue growth since 2022, buoyed by renewed consumer stimulus in China and a high-stakes push into food delivery, a sector long dominated by Meituan. The e-commerce heavyweight reported a 16% rise in quarterly sales to 301.1 billion yuan ($42 billion), driven by higher consumer activity and strategic expansion.

However, behind the upbeat numbers lies a growing debate about the long-term cost of JD’s aggressive moves, particularly as losses in new ventures more than doubled. A financial strategist from Horizon28, Sam Edmund Albert, sheds light on the deeper implications of this growth spurt—what it means for JD’s future, its financial sustainability, and the broader Chinese tech landscape.

Revenue Soars, But Risks Multiply

JD.com’s sales expansion in the March quarter reflects a 16% year-over-year increase, marking its strongest pace in three years. This growth comes as China continues to roll out stimulus measures, including consumer subsidies and trade-in incentives, designed to stimulate domestic demand amid lingering economic headwinds and global trade pressures.

Yet, JD’s newfound success is closely tied to its rapid—and costly—entry into the food delivery market. The company now handles nearly 20 million daily orders, a remarkable jump that places it within range of 20% of Meituan’s 2024 peak volume. JD’s CEO framed food delivery as a “natural extension” of its retail ecosystem, positioning it as a long-term growth avenue despite significant startup costs.

Mounting Losses in New Businesses

While top-line growth impressed, JD’s pivot into food delivery has introduced major financial strain. Losses from new businesses surged to 1.3 billion yuan, nearly double the 670 million yuan reported in the same quarter last year. These losses accounted for over 37% more than market estimates, raising red flags among analysts about the sustainability of JD’s aggressive expansion strategy.

JPMorgan analysts estimate that if current trends continue, JD’s food delivery segment could generate 18 billion yuan in annualized losses, potentially wiping out 36% of its parent company’s operating profit by 2025.

Profitability vs. Market Share: A Familiar Dilemma

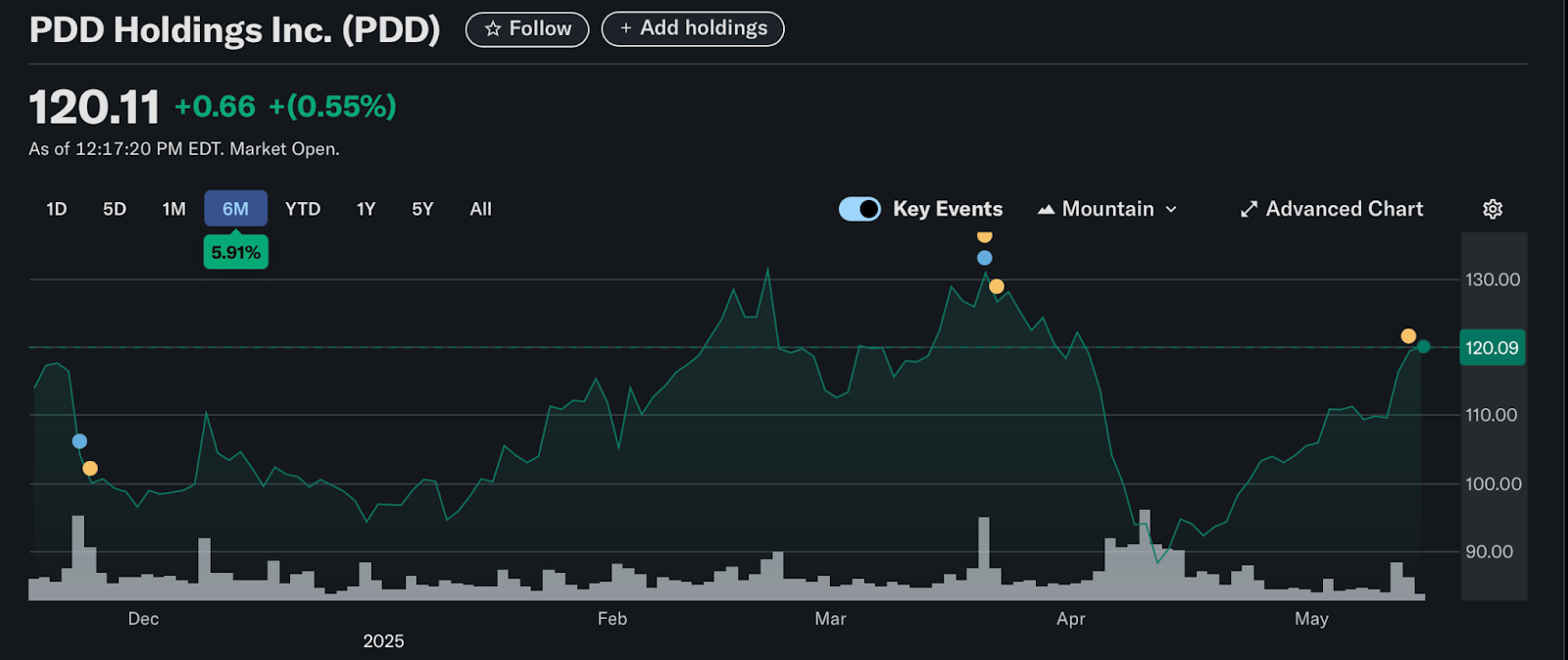

JD has long walked the tightrope between capturing market share and delivering profits, battling entrenched rivals such as Alibaba and PDD Holdings. The current battle with Meituan mirrors earlier fights in e-commerce and logistics—only this time, JD is entering a low-margin, highly competitive sector where even incumbents struggle to maintain profitability.

The company is offering deep discounts and promotional coupons to attract customers. In April, JD pledged to hire 100,000 full-time delivery riders over three months, a costly but necessary step to scale up its network. These tactics have proven effective in gaining market share but have drawn criticism from investors concerned about operating margin erosion.

Stimulus-Fueled Spending: A Temporary Tailwind?

JD’s strong quarterly performance also owes much to Beijing’s ongoing stimulus campaign, which has included monetary easing and trade-in subsidies on everything from smartphones to appliances and cars. These incentives have revived consumer demand for big-ticket items, with JD reporting a 53% increase in net income to 10.9 billion yuan despite mounting losses from new ventures.

However, analysts warn that the boost from the stimulus could be temporary. Without structural improvement in consumer confidence and wage growth, there’s concern that JD’s growth may falter once policy support fades.

Regulatory Spotlight Intensifies

The fiercely competitive nature of the food delivery market has attracted the attention of regulators. This week, China’s market watchdog summoned executives from JD, Meituan, and Alibaba to issue a warning about excessive and “unruly” competitive practices. While no formal penalties have been issued, the intervention signals growing concern over market dynamics that may undercut long-term industry stability.

Mixed Signals from Analysts and Investors

While some analysts commend JD for its ambition and ability to scale new services rapidly, others are urging caution. Bloomberg Intelligence noted that although JD’s adjusted operating profit beat consensus expectations, the declining beat margin, from 18% in prior quarters to 17% this quarter, suggests waning earnings momentum.

Barclays and UBS analysts also raised concerns about earnings dilution and long-term profitability. Investor sentiment remains mixed—JD’s American depositary receipts rose by as much as 3.5% following the report, reflecting optimism about top-line growth but also uncertainty about capital allocation and competitive risk.

Long-Term Outlook: Rewarding or Risky?

JD’s executives insist that the food delivery sector has room for multiple platforms, and the early growth in user volume supports their claim. Yet, the company now faces a delicate balancing act: continue scaling fast enough to compete with Meituan while containing losses and investor backlash.

If JD succeeds in establishing a stable user base and operational efficiency in this vertical, it could carve out a profitable niche in a growing market, especially as AI and logistics integration redefine consumer expectations for instant commerce.

But the cost of missteps is high, and with global trade uncertainties, regulatory pressure, and an economy still recovering, JD’s long-term bet on food delivery could either solidify its future or strain its margins beyond repair.