A sharp and unexpected rally has gripped equity markets, leaving many investors chasing momentum while quietly questioning its foundation. Spurred by temporary relief in U.S.–China trade tensions, coupled with economic resilience and fading volatility, the uptrend in global stocks has caught under-positioned players off guard.

However, with few concrete data points backing the surge and risk appetite returning unevenly, the bullish momentum may be walking a tightrope. Alex van den Berg, senior strategist at Horizon28, explores the precarious mechanics of this rebound, the psychology behind investor hesitation, and what it may signal for the months ahead.

Rising Without Roots: The Discomfort Behind the Rally

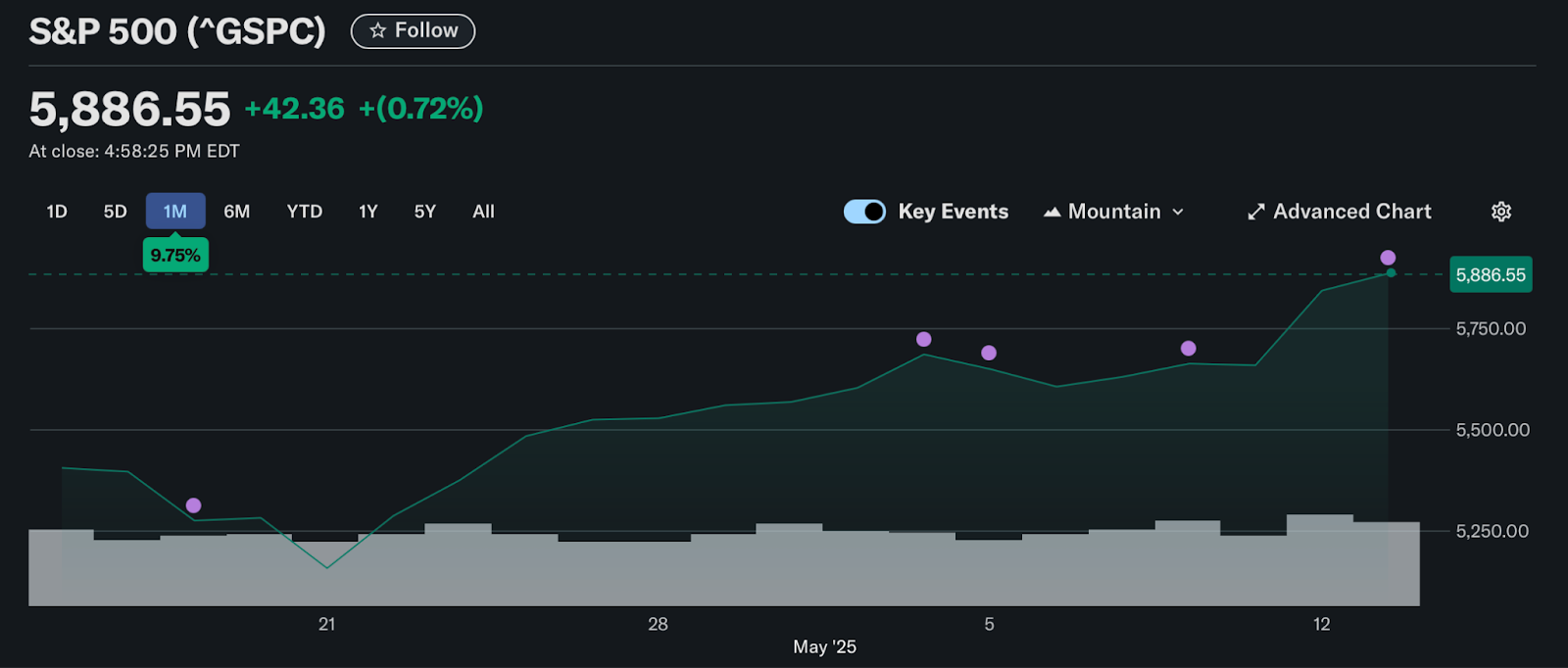

The equity rebound off April’s lows has been swift and broad, but not universally embraced. Market participants describe it as a rally that feels uncomfortable to chase, largely because its underpinnings are more sentiment-driven than data-supported.

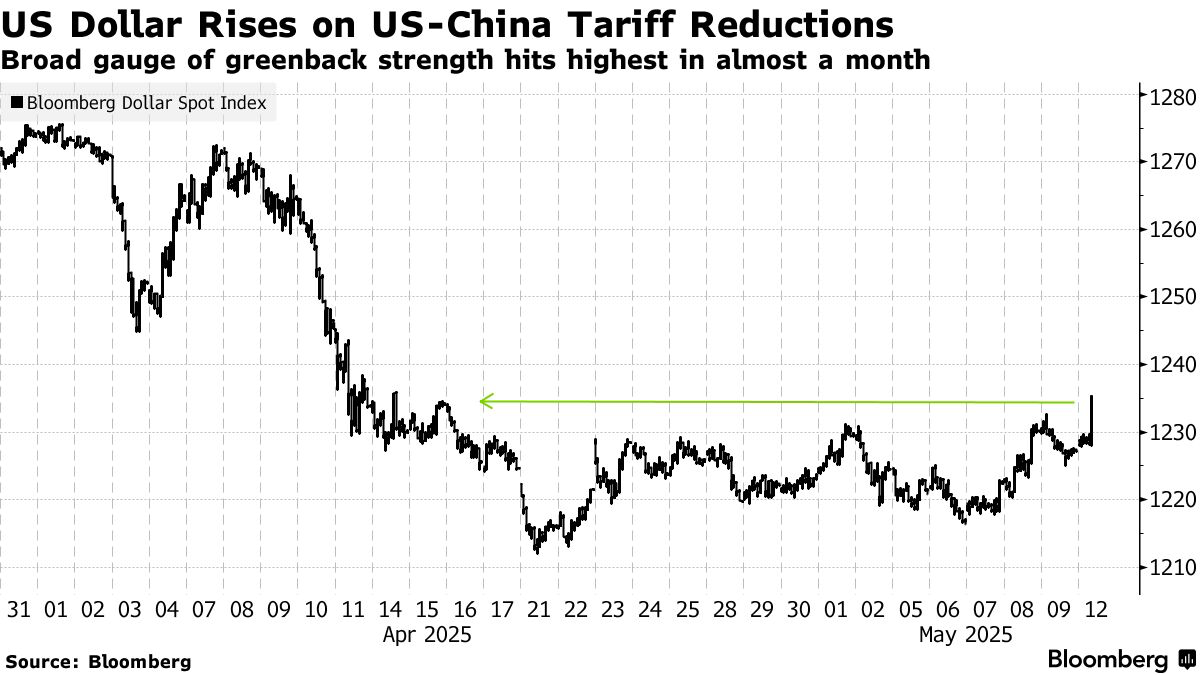

A major catalyst was the 90-day truce in tariff escalation between the U.S. and China, giving markets a needed reprieve. Yet, while this de-escalation has calmed nerves, it hasn’t solved structural issues. Investors remain aware that this is merely a pause, not a resolution, leaving markets exposed to any surprise reversal in tone or policy.

Research teams from multiple firms warn that the “trade war purgatory” could inflict lasting damage even during this window, especially if deals don’t materialize before the deadline.

Speed Shock: When Headlines Outpace Conviction

The violent rebound from April’s lows has drawn comparisons to the post-COVID market recovery in 2020. Much like that period, investors faced blurry economic data, unpredictable headlines, and a rapidly evolving narrative. The sharp move higher has occurred so quickly that even bullish strategists admit it’s been hard to participate meaningfully.

Sectors tied to global growth and Chinese demand, which had previously been battered, were among the biggest winners. Data shows some stocks previously down 60% from February peaks are now leading gains, largely thanks to speculative or “fast-money” flows.

Yet, it’s not high-quality names leading the charge. As noted by traders at a major investment bank, it’s “low-quality themes” that are dominating, suggesting a speculative rally lacking long-term investor conviction.

Algorithms Don’t Blink: Systematic Buying Takes Over

Quant-driven strategies—particularly trend-following and volatility-sensitive funds—have played a dominant role. These systematic investors rely on price momentum, not fundamentals, and have helped fuel the surge.

This trend is compounded by the unexpected behavior of retail investors, who continued to buy even during market dips. Unlike past cycles where retail typically retreats, their resilience has added further fuel to the climb.

Still, professional money remains cautious. Data from the Commodity Futures Trading Commission (CFTC) shows institutional investors are still underweight S&P 500 futures, reflecting broad skepticism.

CTAs Wait for Confirmation, Hedge Funds Cover Shorts

Trend-following strategies like Commodity Trading Advisors (CTAs) are not yet fully committed. Analysts note that due to the speed of the rebound, CTAs prefer more gradual trends and will wait for further confirmation before fully engaging. This hesitation adds to the sense that the rally, while technically strong, lacks consensus conviction.

On the hedge fund side, Goldman Sachs’ Prime Desk reported the second-largest notional net buying in five years, largely attributed to short-covering—a defensive move rather than a risk-on shift. This points to a rally driven more by forced positioning than proactive investment.

Technical Setup Favors Bulls—for Now

Despite the sentiment gap, technical indicators suggest the market has room to run:

- Market breadth remains broad, with participation across sectors.

- The 200-day moving average was cleared without resistance, often a bullish sign.

- V-shaped recoveries, as seen historically, tend to trap cautious investors, rewarding those willing to stay the course.

SentimenTrader data supports this view, noting that while short-term risks remain, longer-term probabilities now tilt in favor of continued upside. But the caveat? This is a market based on probabilities, not guarantees, and good news fatigue could reverse the narrative quickly.

Risk-Reward Reversal Looms

The stronger this rally becomes, the less attractive the risk-reward trade-off grows. Elevated prices combined with lower volatility mean that any shock—be it poor economic data, political missteps, or geopolitical tensions—could result in a disproportionately sharp correction.

Moreover, many of the recent tailwinds aren’t yet backed by hard macro data. The full economic impact of the initial tariff shock is still being assessed. If indicators start reflecting damage from even the short-lived trade escalation, investor optimism could evaporate.

There’s also concern that America’s current president, known for policy unpredictability, could shift tone again as the tariff pause nears expiration, potentially “twisting the knife” on negotiations and disrupting sentiment.

Conclusion: Between Euphoria and Exhaustion

The current equity rally is a paradox—broad but brittle, powerful but uneasy. It reflects a market that wants to believe in recovery, but hasn’t yet seen enough to commit fully. As Alex van den Berg from Horizon28 puts it, “We’re in a market being lifted by relief, not resolution. Until we move from pause to progress, every gain comes with a grain of caution.”

For now, the rally continues. But its staying power will depend on more than just hope. It will require tangible improvement in trade talks, clear economic validation, and reduced dependence on technical squeezes. Without those, investors may soon find that chasing this rally comes with more risk than reward.