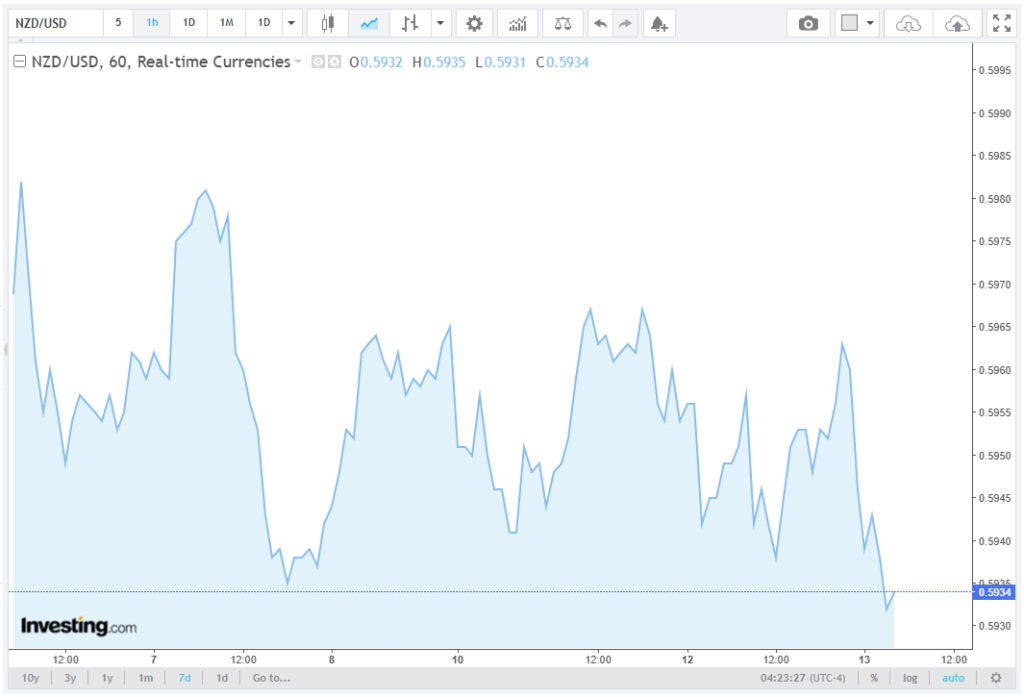

The New Zealand Dollar (NZD) extended its downtrend against the US Dollar (USD) on Wednesday, trading around 0.5940 during Asian session hours, marking the second consecutive day of losses.

The subdued price action followed the release of the Reserve Bank of New Zealand (RBNZ) Inflation Expectations report, which indicated a rise in one- and two-year inflation forecasts. In this article, the team at Byronixel offers a detailed examination of the issue.

Despite the uptick in expectations, NZD/USD has struggled to regain momentum amid a firm US Dollar Index (DXY) and ongoing geopolitical uncertainty. The pair’s recent decline of roughly 0.4% over two days underscores investor caution ahead of upcoming monetary and fiscal events.

RBNZ Inflation Expectations Highlight Rising Price Pressures

According to the RBNZ Q2 2026 report, one-year inflation expectations surged to 3.41%, up from 3.12% in Q1, while two-year expectations increased to 2.53%, compared with 2.41% previously.

The RBNZ’s preferred core inflation measure, which excludes volatile items such as energy and food, remained within the 1–3% target range, with Q1 2026 core CPI recording 2.45% year-on-year, in line with market consensus.

Rising energy costs continue to feed through to inflation, with Brent crude oil prices hovering around $86 per barrel, up from $80 per barrel in March. This is partly due to supply disruptions in the Strait of Hormuz, which has historically accounted for approximately 20% of global seaborne crude oil trade.

Analysts now expect the RBNZ to maintain a neutral-to-tight monetary stance, with market-implied probabilities showing a 75% chance of a 25-basis-point hike in July, according to overnight OIS (overnight indexed swap) data.

Core Inflation Stability Eases Short-Term Pressure

Despite rising market expectations, RBNZ Governor Anna Breman emphasized that core inflation remains contained, with Q1 core CPI unchanged at 2.45% YoY and trimmed mean CPI at 2.38%, both comfortably within the target band of 1–3%.

These readings led market participants to scale back expectations for a rate hike in May, with Fed Funds futures-style pricing reflecting a less than 20% probability of a May move, down from 35% before the report.

However, the ongoing risk of energy-driven inflation, which could contribute an estimated 0.3–0.4 percentage points to headline CPI in H2 2026, keeps the market attentive to July monetary policy decisions.

Fiscal Policy Supports Medium-Term Fundamentals

New Zealand’s Prime Minister Christopher Luxon reiterated the government’s medium-term fiscal objectives in a pre-Budget speech, highlighting plans to achieve a budget surplus by 2028–29 and to reduce gross government debt to around 40% of GDP from 51% in FY2025.

The fiscal trajectory implies a debt-to-GDP reduction of ~1.5 percentage points per year, underpinned by a combination of moderate spending restraint and tax revenue growth projected at 3–4% annually. While these measures support NZD fundamentals over the medium term, short-term currency movements remain sensitive to external shocks, particularly those impacting the US Dollar.

US Dollar Strength Amid Geopolitical Risk

The NZD/USD pair continues to face headwinds as the US Dollar Index (DXY) held firm around 104.6, bolstered by heightened geopolitical volatility in the Middle East. Following the US President’s comments, markets interpreted the heightened risk of regional conflict as supportive for safe-haven USD demand.

The US’s warning of either a new deal or total decimation for Iran was met with a firm Iranian response. Deputy Foreign Minister Kazem Gharibabadi demanded reparations, recognition of sovereignty over the Strait of Hormuz, and a complete end to US sanctions.

These tensions have contributed to increased implied volatility in the FX market, with NZD/USD 1-month options pricing a 6.2% expected move, compared with a 3-month average of 4.8%, indicating heightened risk premia.

Technical Analysis: NZD/USD Remains Subdued

From a technical perspective, NZD/USD has breached short-term support at 0.5950, now eyeing the 0.5920–0.5900 zone as the next key level. Momentum indicators show a 14-day RSI at 38, suggesting the pair is approaching oversold conditions, while the 50-day moving average at 0.5985 continues to act as resistance.

Traders are watching NZD/USD correlation with Brent crude and DXY levels closely, as energy price shocks and US Dollar strength could determine whether the pair stabilizes near 0.5900 or continues to test multi-week lows. Short-term traders may favor range-bound strategies, whereas longer-term positions hinge on inflation trajectory and RBNZ policy clarity.

Conclusion

In summary, the NZD/USD pair is navigating a complex environment where domestic inflation expectations, energy price pressures, and geopolitical risk factors intersect. While the RBNZ’s core inflation control provides some short-term relief, persistent USD strength and market-implied rate hikes suggest that NZD downside pressure may continue in the near term.