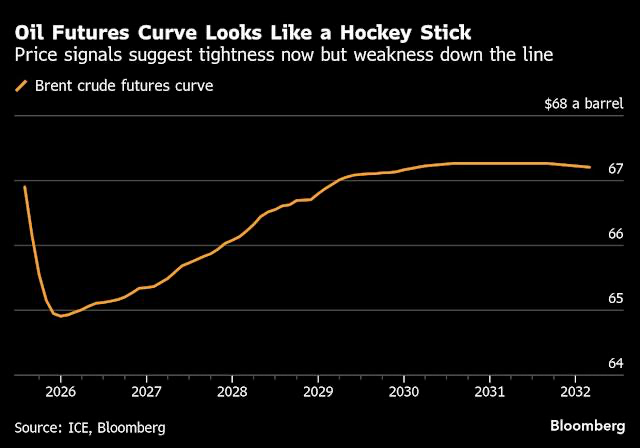

Despite ambitious efforts to increase production, oil prices remain sluggish.

The oil market has been abuzz in recent months as the OPEC+ alliance sets its sights on expanding oil output. The group, led by heavyweights like Saudi Arabia and Russia, has boosted production quotas in hopes of recovering idle capacity and driving global supply.

Yet, according to financial analysts at Rineplex, these quota increases are not yielding the expected surge in actual oil production.

While the OPEC+ plan promised an increase of approximately 1 million barrels per day between March and June, the expected growth in output has remained elusive. The oil market’s reaction has been tepid, with Brent crude hovering around $66.29 per barrel, down more than 11% this year.

The Numbers Tell a Different Story

Despite the headline-grabbing quotas, the reality on the ground is less than convincing. Morgan Stanley’s team, led by Martijn Rats, pointed out that the output increase from the OPEC+ alliance has yet to significantly impact global production.

Their research draws on data from refinery throughput, cargo exports, and pipeline flows, all of which show little evidence of a substantial rise in output.

The Saudi oil production, in particular, appears to have stalled, failing to meet the expectations set by the coalition’s new targets. This sluggish performance raises questions about the effectiveness of the OPEC+ strategy to reclaim market share from non-member producers and counteract trade tensions that have affected global demand.

OPEC+ Still Pushing Forward

That said, the analysts at Morgan Stanley remain cautiously optimistic. They forecast that OPEC+ will increase production by around 420,000 barrels per day between June and September, with about half of that increase coming from Saudi Arabia. While this suggests some future growth, it’s a far cry from the aggressive production increases initially envisioned.

The financial experts are also banking on external factors to balance out the supply-and-demand equation. The non-OPEC supply is expected to grow by about 1.1 million barrels per day in 2025, which could contribute to a global oil surplus despite slower-than-expected output from the cartel.

Market Outlook: What’s in Store for Oil Prices?

The immediate outlook for oil prices remains soft. Even if OPEC+ successfully increases production as planned, it might not be enough to shift market dynamics significantly.

With global demand growth projected to be around 800,000 barrels per day, supply from both OPEC+ and non-OPEC producers could overwhelm demand, keeping prices subdued in the coming months.

Morgan Stanley has revised its forecast for Brent crude to $57.50 per barrel for the second half of the year, a drop from current levels. The analysts are particularly concerned about the end of the summer driving season, when seasonal demand tends to soften.

The Bigger Picture: Beyond Quotas

So, where does this leave investors? While the OPEC+ quota hikes are significant, the market’s reaction suggests that the group’s efforts are unlikely to make a major dent in oil prices in the short term. The growing global supply glut, combined with muted demand growth, points to a softer market outlook for the rest of 2025.

The key takeaway for investors? Pay attention to external factors like global demand trends and non-OPEC production growth. These will be just as important, if not more so, in determining the direction of oil prices as the moves made by OPEC+.

The Road Ahead: Oil’s Long-Term Potential

The broader implications for the oil market are complex. Even with the OPEC+ cartel’s best efforts, they face a highly competitive global market. Shifts in production dynamics, such as those from U.S. shale producers and other non-member nations, could further dilute OPEC’s market influence.

For now, though, OPEC+ is betting that gradual increases in supply will eventually catch up with demand, allowing them to regain some lost ground in the oil market.

As investors watch the oil market unfold, attention must turn to the balance of supply and demand as well as the geopolitical landscape. With OPEC+ quotas in flux and external forces pulling in opposite directions, the outlook for oil remains uncertain.

Final Thoughts: Patience Is Key

While it’s clear that OPEC+ quota hikes have not triggered the expected surge in the oil market, the story is far from over. The market has yet to fully react to these increases, and the next few months will be pivotal in determining whether OPEC+ can meet its ambitious targets.

The oil market’s trajectory remains uncertain, and much hinges on how quickly Saudi Arabia and other key members ramp up production. If the cartel succeeds in boosting supply as planned, it could eventually fuel a price recovery. However, with external factors like global demand trends and the actions of non-OPEC producers playing a crucial role, there’s still significant volatility ahead.

For investors, the message is clear: stay vigilant and keep track of key indicators. Watch for signs of increased production, especially in Saudi Arabia, and monitor global demand closely.

These signals will provide insight into whether OPEC+’s efforts can turn the tide in oil prices or if the market will continue its downward trajectory. Only time will tell if these incremental increases will bring the change that OPEC+ is hoping for.