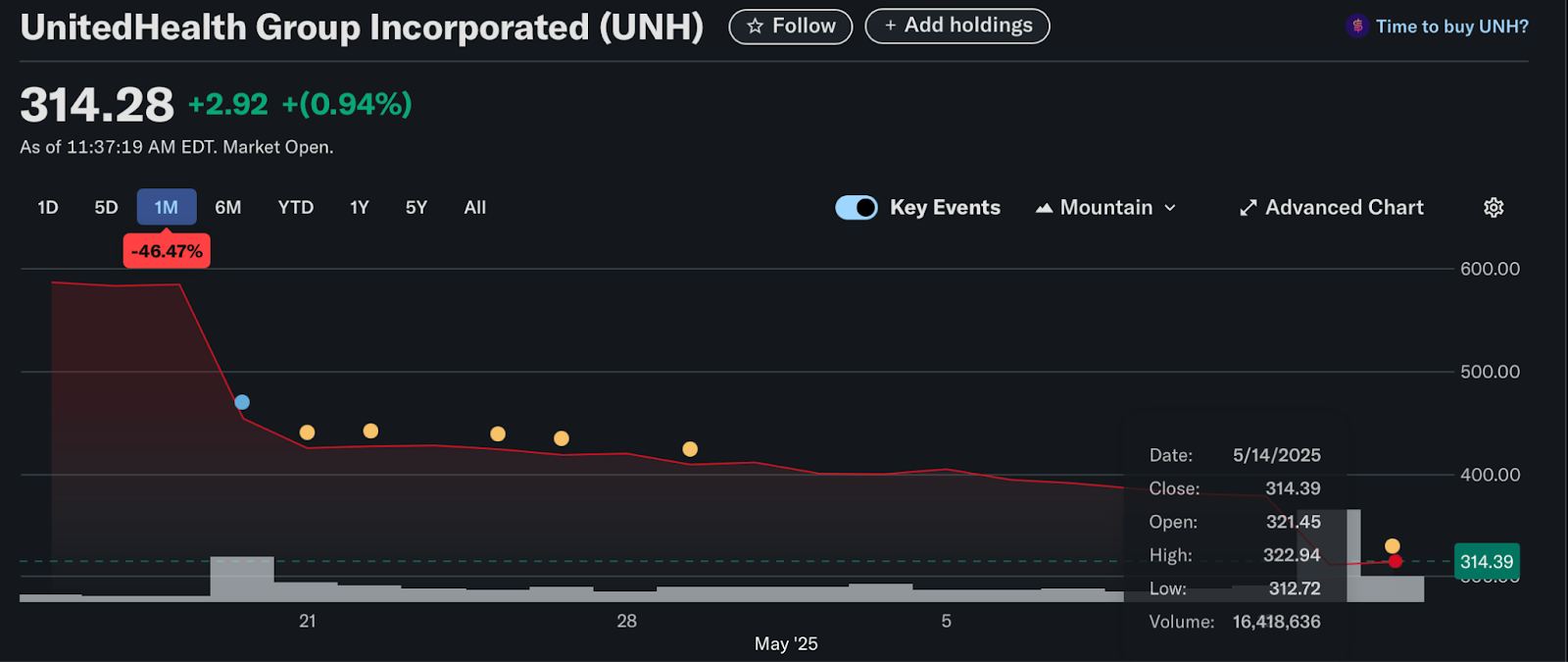

Wall Street was caught off guard this week by a series of abrupt moves from UnitedHealth Group, including a leadership reshuffle and the withdrawal of its 2025 financial guidance, just weeks after the company signaled efforts to recalibrate elevated costs. The immediate reaction was sharp—shares plunged 18% on Tuesday, prompting downgrades and widespread uncertainty about the company’s near-term trajectory.

The move has reignited concerns about structural pressures within Medicare Advantage and the broader healthcare insurance sector. A financial strategist from Horizon28, Emma Rives, explores the deeper implications of UnitedHealth’s recent decisions, the market’s anxious response, and what the road ahead could look like for the industry giant.

A Sudden Change at the Helm—and a Strategic Reset

UnitedHealth replaced CEO Andrew Witty, age 60, with his predecessor, 72-year-old Stephen Hemsley, in a move that shocked analysts and investors alike. Hemsley, credited with transforming UnitedHealth into a vertically integrated powerhouse during his tenure from 2006 to 2017, has returned amid growing financial uncertainty.

The leadership shift came alongside another jolt: UnitedHealth pulled its 2025 earnings guidance, signaling management’s discomfort with forecasting performance while cost trends remain unclear. While leadership cited a need to give the incoming CEO time to reassess projections, analysts believe the guidance withdrawal reflects ongoing challenges in managing Medicare Advantage utilization and cost volatility in the company’s Optum division.

The Fallout: Stock Plunge and Analyst Downgrades

The market reacted swiftly. On Tuesday, UnitedHealth’s stock fell 18%, its steepest drop in recent history. Although shares recovered slightly the following day with a 1% uptick, the overall sentiment remains deeply cautious.

Bank of America downgraded the stock to Neutral, stating that the decision to pull guidance reflects both strategic uncertainty and elevated care utilization. Meanwhile, UBS and Barclays analysts warned of continued headwinds throughout 2025, emphasizing that investor confidence would remain low until a reliable earnings floor is re-established.

Medicare Advantage Pressures Take Center Stage

At the core of UnitedHealth’s current trouble is higher-than-expected utilization in its Medicare Advantage segment. According to the company, care activity has not only increased but also expanded into new types of treatments, putting additional strain on margins. These cost escalations are now expected to impact other parts of the insurance business, further dampening 2025 prospects.

Mizuho Securities analysts noted that the upward trend in utilization doesn’t appear to be abating, while UBS stated explicitly that they are not assuming any normalization this year, adding to concerns that 2026 may be the earliest point for earnings stabilization.

A Pattern of Mounting Challenges

This episode adds to a growing list of challenges for UnitedHealth. Earlier this year, the company dealt with the aftermath of a cyberattack that proved more damaging than initially disclosed.

On top of that, leadership had to contend with public scrutiny and reputational fallout linked to a high-profile tragedy involving the company’s late CEO, which raised broader ethical and regulatory questions about the industry. Combined, these setbacks have strained investor patience and contributed to a 38% decline in UnitedHealth’s stock over the past year.

Sector-Wide Implications—or an Isolated Misstep?

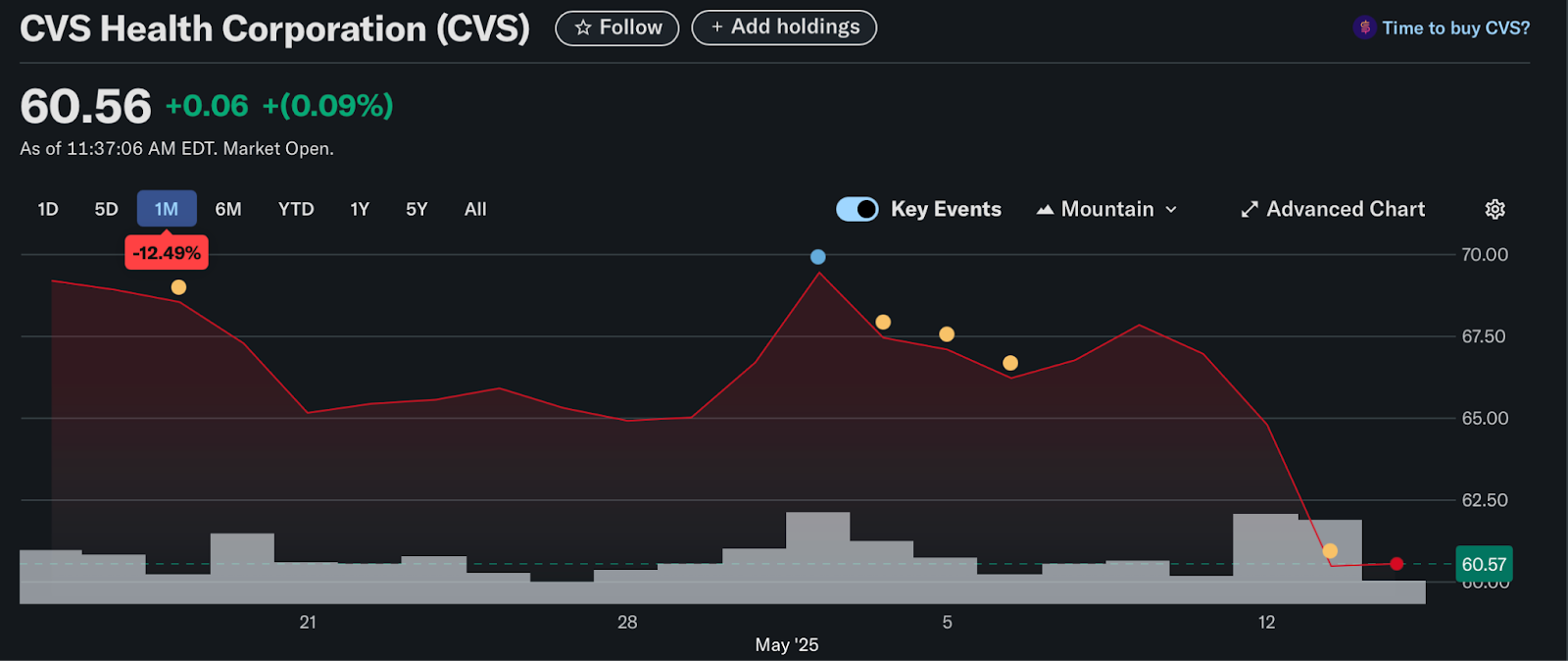

Initially, the spike in Medicare Advantage costs raised fears that other major players like CVS Health might face similar pressures. But those concerns have since eased, with analysts now attributing UnitedHealth’s woes to internal mispricing and planning errors rather than systemic industry flaws.

This has tempered broader sector contagion but has also underscored how even the most well-established insurers are not immune to operational missteps in a high-cost, post-pandemic care environment.

Strategic Outlook: 2026 as the Recovery Timeline

During Tuesday’s investor call, new CEO Hemsley and CFO John Rex acknowledged the scale of the problem, forecasting a return to profitability not before 2026. This admission has recalibrated Wall Street’s expectations, shifting focus from recovery in 2025 to stability two years out.

While this long horizon could appeal to long-term institutional investors, the short- and medium-term outlook remains unclear. Analysts from Barclays summed it up best, stating that unless a clear earnings baseline is set, few investors are likely to offer UnitedHealth the benefit of the doubt.

Conclusion: Confidence Fractured, Patience Tested

UnitedHealth’s leadership reshuffle and decision to withdraw forward guidance have magnified concerns around transparency, planning, and cost control—areas once considered core strengths of the insurer. The 18% stock plunge, driven by fears of deeper financial strain, shows just how fragile investor trust has become in the face of uncertainty.

The path to recovery likely runs through 2026, but without concrete improvements in utilization trends and margin stability, the market may remain skeptical. For now, UnitedHealth’s reputation as a reliable bellwether for the sector has been tested, and the company will need more than a leadership reshuffle to rebuild market confidence.