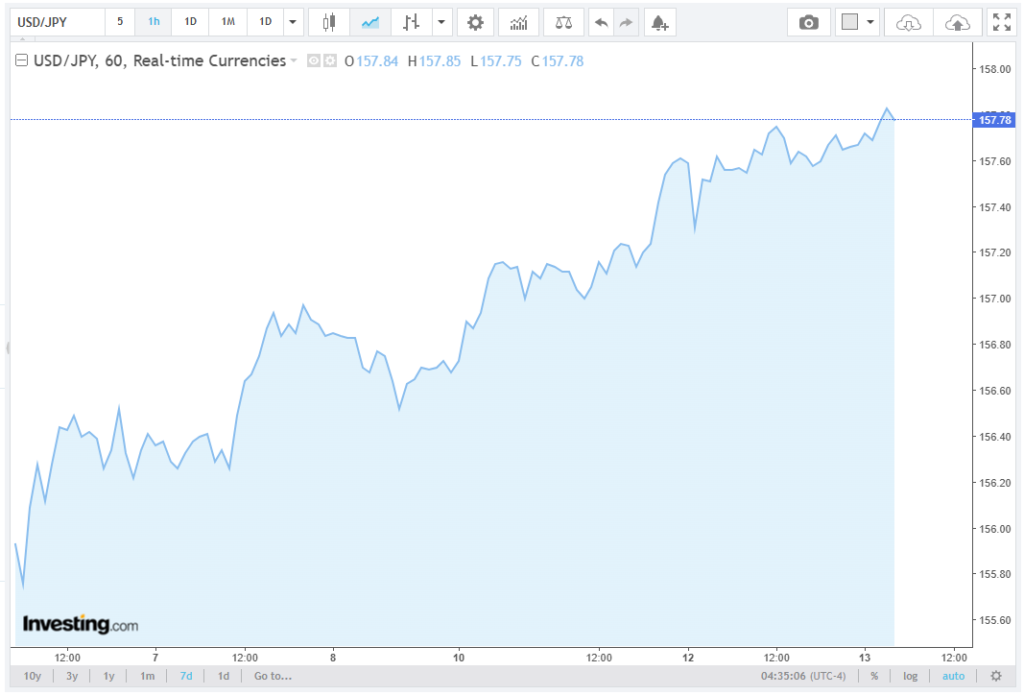

The Japanese Yen (JPY) remains weak versus the US Dollar (USD), as USD/JPY climbs for a third straight session, hovering around 157.70 during Wednesday’s Asian trading.

The pair’s strength reflects a combination of monetary divergence, geopolitical risk premiums, and evolving expectations for both the Bank of Japan (BoJ) and the Federal Reserve (Fed) policy trajectories. Byronixel experts delve into this matter comprehensively in their article.

USD/JPY Gains on Strong Current Account Surplus

The Yen’s softness follows the release of Japan’s March current account surplus, which surged to JPY 4,681.5 billion, up 29% year-on-year (YoY) from JPY 3,625.3 billion in March 2025 and surpassing the consensus forecast of JPY 3,879 billion.

The trade balance component contributed JPY 1,532.4 billion, while primary income accounted for JPY 3,149.1 billion, highlighting the continued robustness of Japan’s overseas investment income.

Despite the record surplus, the JPY weakened, underscoring market sensitivity to interest rate differentials and risk sentiment. Historically, the Yen has tended to appreciate on large surpluses, but persistent divergence between Japanese and US short-term rates has suppressed its safe-haven demand.

BoJ Signals Incremental Policy Tightening

The Bank of Japan’s April Summary of Opinions indicated that policymakers are considering incremental hikes in the policy rate as early as the June 2026 meeting. The BoJ cited inflationary pressures from rising crude oil prices, noting that Tokyo CPI climbed 2.1% YoY in April, while core-core CPI (excluding food and energy) remained at 1.2% YoY, indicating underlying price pressures remain contained but are gradually firming.

According to OECD projections, Japan’s short-term policy rate could reach 2% by the end of 2027, suggesting a gradual tightening cycle. However, the BoJ is expected to maintain flexibility in Yield Curve Control (YCC) operations, particularly in the 10-year JGB market, where yields recently rose to 0.48%, approaching the upper bound of the 0.5% target.

Fiscal policy recommendations from the OECD include raising the consumption tax to support revenue and limiting supplementary budgets to exogenous shocks, ensuring sustainable fiscal consolidation amid a projected gross debt-to-GDP ratio of 266% in 2026.

US Dollar Strength Supported by Geopolitics and Inflation

The USD continues to benefit from elevated geopolitical risk premiums and hawkish US macroeconomic data. USD/JPY gains have been reinforced by heightened Middle East tensions, following statements from the US President and Iranian Deputy Foreign Minister. Markets are pricing increased risk premia, as measured by the JPY/USD volatility index, which spiked to 9.7%, the highest since January 2026.

Inflationary data in the US further support the Greenback. The Bureau of Labor Statistics (BLS) reported that April CPI increased 0.6% month-over-month (MoM) and 3.8% year-over-year (YoY), surpassing the 3.5% consensus.

Core CPI, excluding food and energy, rose 0.4% MoM, or 2.8% YoY, signaling persistent price pressures. This data reinforces expectations that the Fed will maintain the target funds rate at 5.25–5.50% through at least Q4 2026.

Technical Analysis of USD/JPY

From a technical perspective, USD/JPY maintains bullish momentum above the 157.00 support level. Resistance near 158.50 represents a key short-term target, with traders monitoring the 50-day moving average at 157.90 for breakout confirmation.

Volume-weighted average price (VWAP) analysis indicates that intraday support is likely between 157.40 and 157.50, with potential retracement levels at 156.80 if geopolitical tensions ease or BoJ signals faster-than-expected tightening.

Short-term positioning shows a net long USD speculative exposure of +92,000 contracts, according to the CFTC Commitments of Traders report, highlighting investor conviction in continued USD strength relative to JPY.

Implications for Monetary and Fiscal Policy

Despite a record current account surplus, the Yen remains subdued, reflecting a combination of monetary policy divergence, persistent US inflation, and geopolitical uncertainty. The BoJ faces a delicate balancing act: raising short-term rates while maintaining market liquidity in the JGB market. Should US Treasury yields continue to rise, the USD/JPY pair could test 160.00 in a scenario of continued USD demand for yield.

Fiscal and monetary alignment is also critical. The OECD emphasizes stricter budgetary discipline and efficient consumption tax measures to manage Japan’s fiscal deficit, projected at 3.4% of GDP in FY2026, while sustaining moderate economic growth of 1.5% YoY GDP expansion.

Conclusion

The Japanese Yen remains subdued, pressured by monetary divergence, geopolitical risk, and strong US inflation data. While Japan’s current account surplus reflects robust external balances, market focus remains on BoJ policy adjustments, US Fed guidance, and risk sentiment dynamics.

Near-term USD/JPY trading will likely be dominated by interest rate spreads, geopolitical developments, and BoJ policy signaling, with a cautious eye on 10-year JGB yields and global equity volatility.