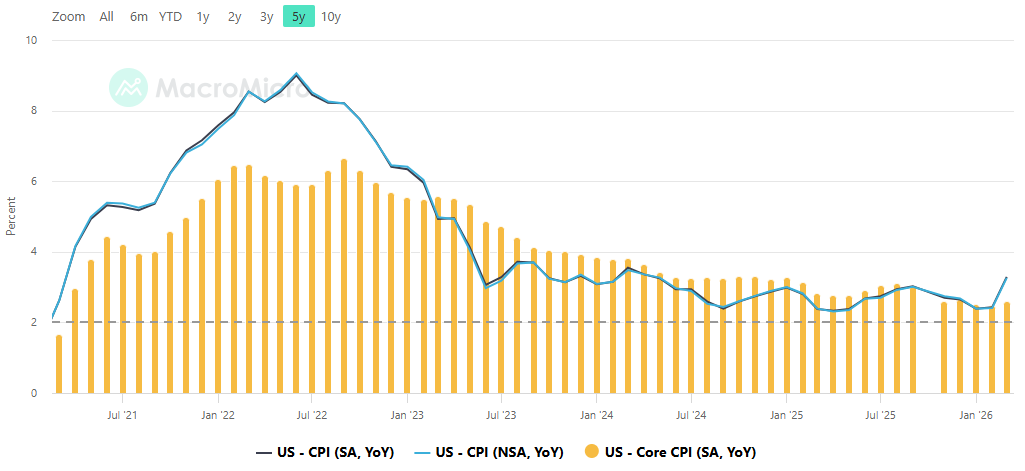

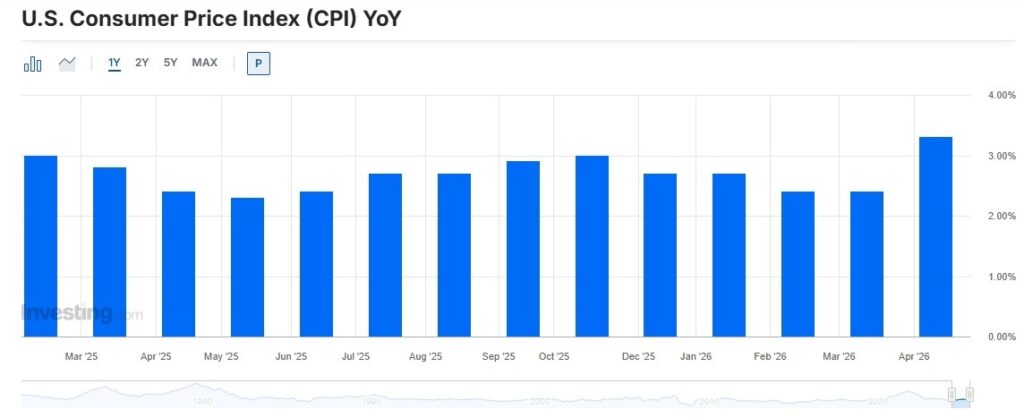

The US Consumer Price Index (CPI) is set to dominate financial market discussions this week, as the Bureau of Labor Statistics (BLS) prepares to release the April inflation data on Tuesday. Analysts are forecasting a notable rise in headline inflation, with the annual CPI expected to reach 3.7% year-on-year (YoY), up from 3.3% in March.

This increase comes amidst persistently high energy prices, particularly Oil, which continue to exert upward pressure on the cost of living. The analysts at Marbrisse offer an in-depth exploration of this subject in their latest report.

The monthly CPI is predicted to rise by 0.6%, following a 0.9% increase in March, reflecting the lingering impact of global energy volatility on household expenses. Meanwhile, the core CPI, which strips out the more volatile components of food and energy, is projected to increase 0.4% month-on-month and 2.7% YoY, signaling that underlying price pressures remain sticky despite temporary fluctuations in commodity prices.

Oil Prices Drive Inflationary Pressures

The primary driver of this anticipated surge in inflation is the elevated Oil prices stemming from the US-Iran geopolitical tensions. Since the onset of the Middle East conflict on February 28, the West Texas Intermediate (WTI) crude benchmark has surged by more than 50%, reflecting heightened risk premiums and constrained global supply.

Although crude prices experienced a modest correction in early May, they remain approximately 40% higher than pre-conflict levels, maintaining significant upward pressure on energy-related inflation.

High energy costs directly influence transportation, utilities, and even food prices, as supply chains absorb increased production and distribution expenses. Analysts emphasize that these pass-through effects from Oil markets will likely be a central focus of the April CPI report, particularly given the persistent macro volatility in global energy markets.

Core Inflation Remains a Concern

While headline CPI is heavily influenced by energy price swings, core inflation offers a clearer view of underlying trends in the economy. Economists expect core CPI to increase by 0.4% MoM, slightly above March’s 0.2% rise, translating into an annual rate of 2.7%.

Jim Reid from Deutsche Bank observes that headline inflation is expected to increase by 0.58% month-on-month, slowing from March’s 0.9% but remaining relatively strong. Meanwhile, the core inflation measure is projected to pick up to 0.39% from 0.2% month-on-month, indicating that underlying price pressures continue to persist even as the impact of energy prices diminishes.

These figures underscore the persistent inflationary pressures beyond the energy sector, indicating that consumer prices for goods and services continue to rise steadily. The stickiness of core inflation may influence the Federal Reserve’s monetary policy decisions, particularly regarding interest rate adjustments aimed at containing long-term price stability risks.

Market Implications: USD and EUR/USD Outlook

Financial markets are already pricing in expectations for inflation data, particularly in foreign exchange and fixed-income sectors. The EUR/USD currency pair shows a technically bullish stance, reflecting optimism in the Euro, but the momentum remains muted amid US dollar strength driven by anticipated higher inflation readings.

A stronger-than-expected US CPI print could reinforce USD bullishness, potentially applying pressure on the EUR/USD exchange rate, while weaker inflation might signal a slowdown in monetary tightening by the Federal Reserve, giving the Euro a temporary advantage. Traders are therefore closely monitoring both headline and core CPI metrics, as even minor deviations from forecasts can trigger significant FX volatility.

Economic Context and Inflationary Trends

The US inflation landscape remains complex, shaped by a combination of supply shocks, geopolitical risks, and domestic demand patterns. The current CPI forecast reflects not only the direct impact of elevated Oil prices but also ongoing pressures in housing, transportation, and medical services, which have shown resilience in the face of slowing economic growth.

Analysts highlight that although monthly headline inflation is expected to moderate slightly compared to March, the annualized figures are still climbing toward the highest levels since September 2023. This suggests that while temporary factors such as energy price spikes are partially influencing the data, persistent cost pressures in the broader economy cannot be ignored.

Conclusion: CPI Data in Focus

As the BLS prepares to release April CPI data, market participants are bracing for another inflationary surprise, largely driven by sustained high energy prices and sticky core inflation. Headline CPI is projected at 3.7% YoY, while core inflation edges higher to 2.7%, reflecting ongoing upward pressure on consumer prices.

Markets will closely monitor both headline and core CPI figures, assessing whether the Federal Reserve will continue its tightening path or adopt a more measured approach. The combination of geopolitical uncertainty, energy market volatility, and persistent price pressures ensures that April’s CPI release will be a defining moment for financial markets and economic policy discussions in the months ahead.