Software companies faced intense selling pressure despite the Nasdaq Composite advancing and the technology sector broadly participating in a rally. The divergence highlighted investor concerns about AI disruption, competition intensity, and valuation sustainability across the subsector. Subsector weakness created opportunities for stock pickers willing to differentiate quality from challenged business models.

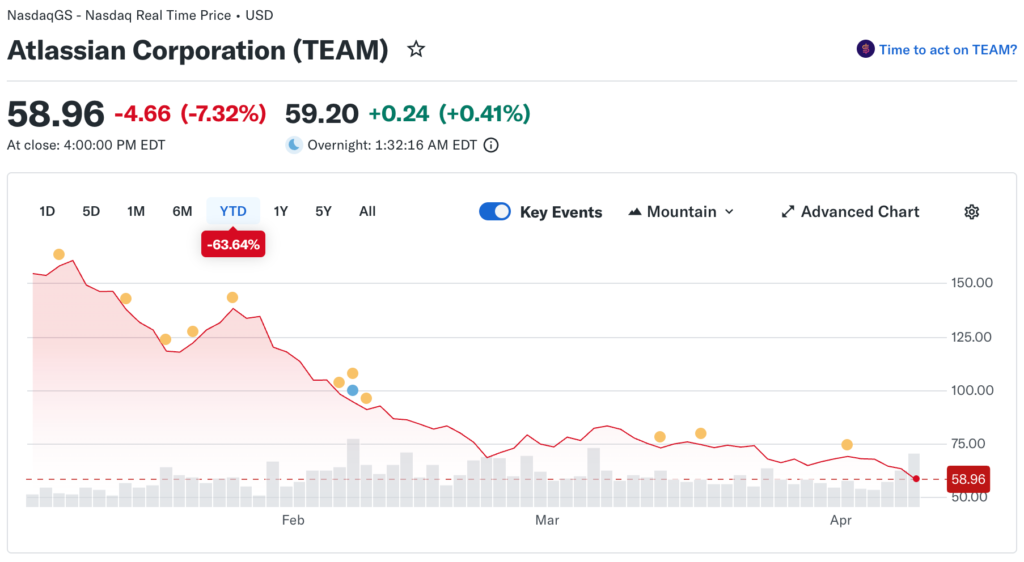

Junior finance analysts at Byronixel break down how Atlassian’s price targets were slashed by nearly 40% to $115, citing artificial intelligence as a potential near-term headwind. The dramatic reduction spooked investors despite analysts maintaining a buy rating and noting the company’s competitive moat. Shares trading below $60 implied substantial upside remained even after the target cut.

The Atlassian Challenge

Jira and Confluence products enjoyed strong market positions in project management and collaboration categories. But AI-powered alternatives from both startups and tech giants threatened to erode customer lock-in. Enterprises experimenting with generative AI tools for workflows might delay Atlassian adoption significantly.

Wall Street still expected roughly 20% annual earnings growth from the company over the coming years. This growth rate at the current valuation multiple suggested the stock wasn’t expensive if execution delivered. The question centered on whether AI enablement or displacement dominated near-term competitive dynamics.

The Zscaler Competition

Analysts downgraded Zscaler to hold, warning about increasing competition from multiple sources pressuring the cloud provider. The cybersecurity market fragmentation intensified as larger platform players added security capabilities. This encroachment threatened specialist vendors’ pricing power and market share significantly.

Palo Alto Networks and other established vendors expanded cloud-native security offerings, competing directly with core products. Enterprises preferred consolidating security tools with fewer vendors to reduce complexity. This purchasing preference disadvantaged point solution providers regardless of technical superiority.

The AI Disruption Thesis

Generative AI tools threatened to automate workflows currently requiring specialized software applications across industries. Code generation capabilities potentially reduced demand for development platforms that dominated recent years. Document creation and analysis features might displace collaboration and content management systems entirely.

Enterprise software vendors responded by embedding AI capabilities into existing products defensively. But this defensive strategy faced challenges from hyperscalers offering AI-powered alternatives at lower prices. The commoditization threat is particularly acute for applications with thin differentiation beyond the user interface.

The Valuation Reset

Software multiples expanded dramatically during the pandemic as digital transformation accelerated and interest rates fell. Cloud companies traded at 15x to 20x sales despite limited profitability. The valuation euphoria created vulnerability to any growth disappointments or macro headwinds.

Interest rate increases in 2022-2023 compressed multiples across growth stocks significantly. The software sector bore a disproportionate impact given long-duration cash flows sensitive to discount rates. Current valuations still implied strong growth assumptions despite rising competitive threats.

The Spending Scrutiny

Chief Financial Officers implemented a rigorous review of technology budgets, seeking cost reduction opportunities. Cloud infrastructure spending faced particular scrutiny given the substantial monthly bills accumulating. Vendors lacking clear ROI quantification struggled to maintain pricing power during renewals.

Software seat count reductions emerged as a popular cost-cutting lever across corporate America. Companies discovered that many purchased licenses went unused or underutilized significantly. Right-sizing deployments reduced vendor revenues without impacting business operations.

The Consolidation Pressure

Platform vendors offering broad suites enjoyed an advantage over point solutions during budget pressures. Customers preferred integrated offerings from a single vendor over best-of-breed multi-vendor architectures. This dynamic favored large incumbents with comprehensive portfolios.

Microsoft leveraged bundling strategies to gain share across multiple software categories. Office 365 integration created stickiness extending into collaboration, security, and analytics. Competitors struggled to match this distribution advantage.

The Small-Cap Carnage

Smaller software vendors lacked scale advantages, protecting large-cap peers from competitive pressures. Customer concentration risks meant that losing a single major account could materially impact financials. The precarious position made these stocks particularly volatile during sector rotations.

Growth rates for small-caps needed to exceed large-caps significantly to justify premium valuations. But competition from well-funded giants made sustaining differentiation difficult. Many niche vendors faced existential threats from larger competitors entering their markets.

The SaaS Model Questions

Subscription economics that previously attracted premium valuations faced scrutiny around customer lifetime value assumptions. Churn rates climbing during economic uncertainty undermined cohort economics. The revenue predictability advantage diminished as renewal rates deteriorated.

Net revenue retention metrics deteriorated from pandemic peaks as expansion rates normalized and churn increased. Companies previously posting 120%+ retention saw declines to 110% range. This deceleration disproportionately impacted growth projections.

The Recovery Scenarios

Best case involved AI fears proving overblown as software vendors successfully integrated new capabilities, strengthening positions. Revenue growth reaccelerated, and multiples expanded from current compressed levels. Patient investors buying weakness earned strong returns.

Base case saw extended multiple compression as growth decelerated but remained positive. Software stocks underperformed the broader market until valuations reset to more sustainable levels. Selective opportunities emerged, but sector leadership shifted elsewhere.