Wall Street entered April 10 riding momentum from the longest winning streak since October 2025, with equity indices advancing steadily despite conflicting signals from energy markets. The remarkable turnaround demonstrated resilience amid ongoing geopolitical uncertainty as traders positioned for weekend diplomatic talks.

Byronixel examines how the Dow Jones Industrial Average turned positive for the year, climbing 0.25% since January as investor confidence returned following the ceasefire announcement. The S&P 500 extended gains for a seventh straight session, adding 0.62% to close at 6,824.66 points. This winning streak represented the most sustained advance in six months.

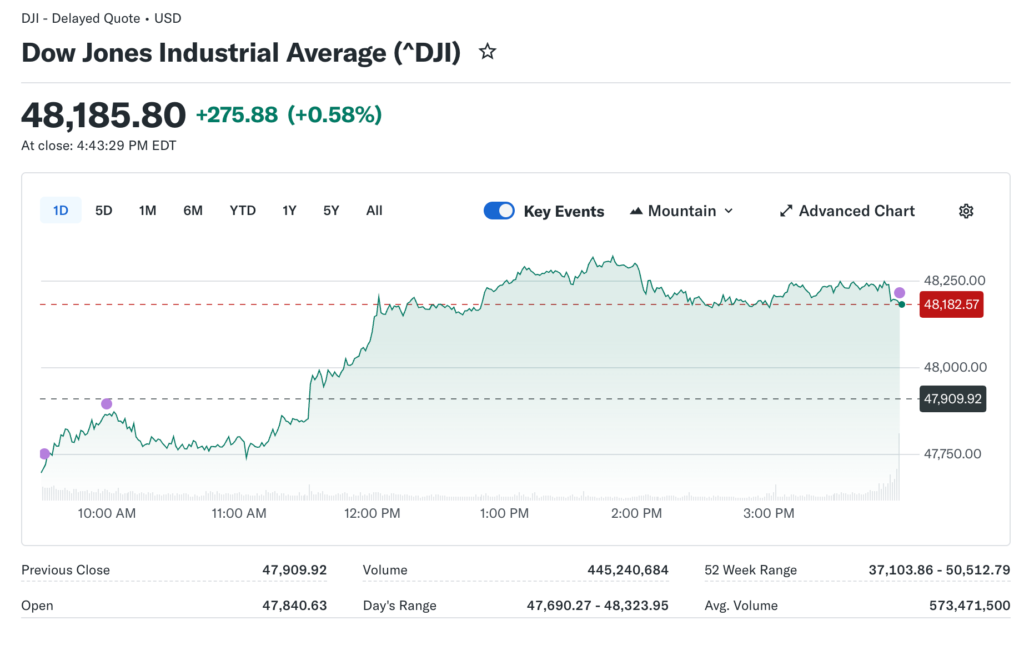

The Momentum Builds

The Nasdaq Composite climbed 0.83% to finish at 22,822.42, outpacing broader market performance as technology stocks regained leadership. The Dow posted a 275.88-point gain to settle at 48,185.80 points, pushing the blue-chip index into positive territory. Market breadth improved steadily throughout the rally as defensive positioning unwound completely.

More sectors participated in gains as capital rotated into cyclical names that had suffered during the crisis. This broadening participation suggested genuine conviction rather than narrow leadership from a handful of stocks. The psychological importance of the Dow returning to positive annual returns cannot be overstated for retail investor sentiment.

The Oil Contradiction

West Texas Intermediate crude rose more than three percent to settle at $97.87 per barrel after earlier touching $100 intraday levels. Brent crude futures added over one percent to close at $95.92, maintaining its typical premium to WTI. The persistent oil strength seemed at odds with equity market optimism about crisis resolution moving forward.

Weekend ceasefire talks scheduled in Pakistan created a binary outcome scenario for traders positioning ahead of key developments. Success could send crude tumbling back toward $90 levels, while a breakdown might spike prices above $105 quickly. Markets positioned cautiously ahead of this critical diplomatic moment that would determine near-term direction.

The Technology Performance

Software companies faced particular pressure as investors questioned valuations following the recent crisis rally and competitive dynamics. Atlassian shares fell after analysts slashed price targets, citing artificial intelligence as a near-term headwind. The stock trades below $60 while reduced targets sit at $115, implying substantial upside remains available.

Zscaler faced a downgrade due to increasing competition from multiple sources, pressuring the cloud security provider significantly. This reflected broader concern that cybersecurity market fragmentation would pressure margins and growth rates going forward. Competitive dynamics shifted as larger platform players encroached on specialist territories across the technology sector.

The Meta Catalyst

Meta Platforms surged 2.6% following the announcement of a new artificial intelligence model, providing a significant boost to index performance. The social media giant’s AI developments suggested continued investment in next-generation technologies despite economic uncertainty persisting. Investors rewarded companies maintaining innovation spending through volatility rather than cutting budgets to preserve margins.

The $21 billion expanded agreement between Meta and CoreWeave for AI computing capacity signaled that massive infrastructure buildout is continuing. This partnership demonstrated confidence in AI monetization despite questions about near-term returns on massive investments. The scale of commitment suggested Meta sees a clear path to revenue generation from these capabilities.

The Defensive Rotation

Utilities and consumer staples joined the rally as investors gained confidence about economic stability after weeks of uncertainty. American Electric Power advanced alongside Walmart, demonstrating rotation into defensive names traditionally shunned during growth phases. This suggested balanced positioning rather than aggressive risk-taking by professional money managers seeking portfolio protection.

Walmart benefited from strong consumer spending data showing resilience despite elevated gasoline prices pressuring household budgets. Lower-income households maintained purchase patterns even as energy costs pressured budgets, according to payment data. The retail giant’s value positioning attracted shoppers across the economic spectrum during inflationary periods.

The Sector Breakdown

Industrials led gains with sector funds jumping 3.8%, reflecting optimism about manufacturing activity and infrastructure spending ahead. Materials followed closely with gains of 3.3% as commodity demand expectations improved with reduced recession probability. These cyclical sectors benefited most from lower recession probability as economic data remained resilient overall.

Information Technology added 3.1%, demonstrating continued investor appetite for growth despite software sector weakness in certain areas. The broad technology gains offset headwinds facing specific subsectors like enterprise software and cybersecurity point solutions. Semiconductor stocks are particularly strong as the AI infrastructure spending thesis remained intact despite some investor skepticism.

The Weekend Catalyst

Pakistan-hosted ceasefire talks created a clear binary event for Monday, opening with significant implications for multiple asset classes. Successful negotiations could spark another leg higher in equities while sending oil prices crashing toward pre-crisis levels. Breakdown would reverse recent gains as markets reprice geopolitical risk premium back into all assets.

Positioning ahead of such uncertain outcomes typically drives reduced trading volumes and tighter ranges during Friday sessions. The session likely sees consolidation as traders avoid major commitments before weekend developments that could reshape markets. This cautious approach makes sense given the high stakes involved in the diplomatic discussions ahead.